JGBs JPYing BOJ

EDU DDA Jan. 21, 2026

Summary: The JGB selloff has reached extreme proportions and thereby stoking all kinds of confusion about why it has happened. Since many assume it is about the Japanese government’s absurdly awful fiscal position, it has been further asserted this vigilantism will end up sweeping the world’s bond markets very quickly. A nice story and actually a far more preferable outcome, however what’s happening in JGBs is the other side of JPY as translated via BoJ. You don’t have to take my word for this.

THE GREATEST SOURCE OF FINANCIAL UNCERTAINTY

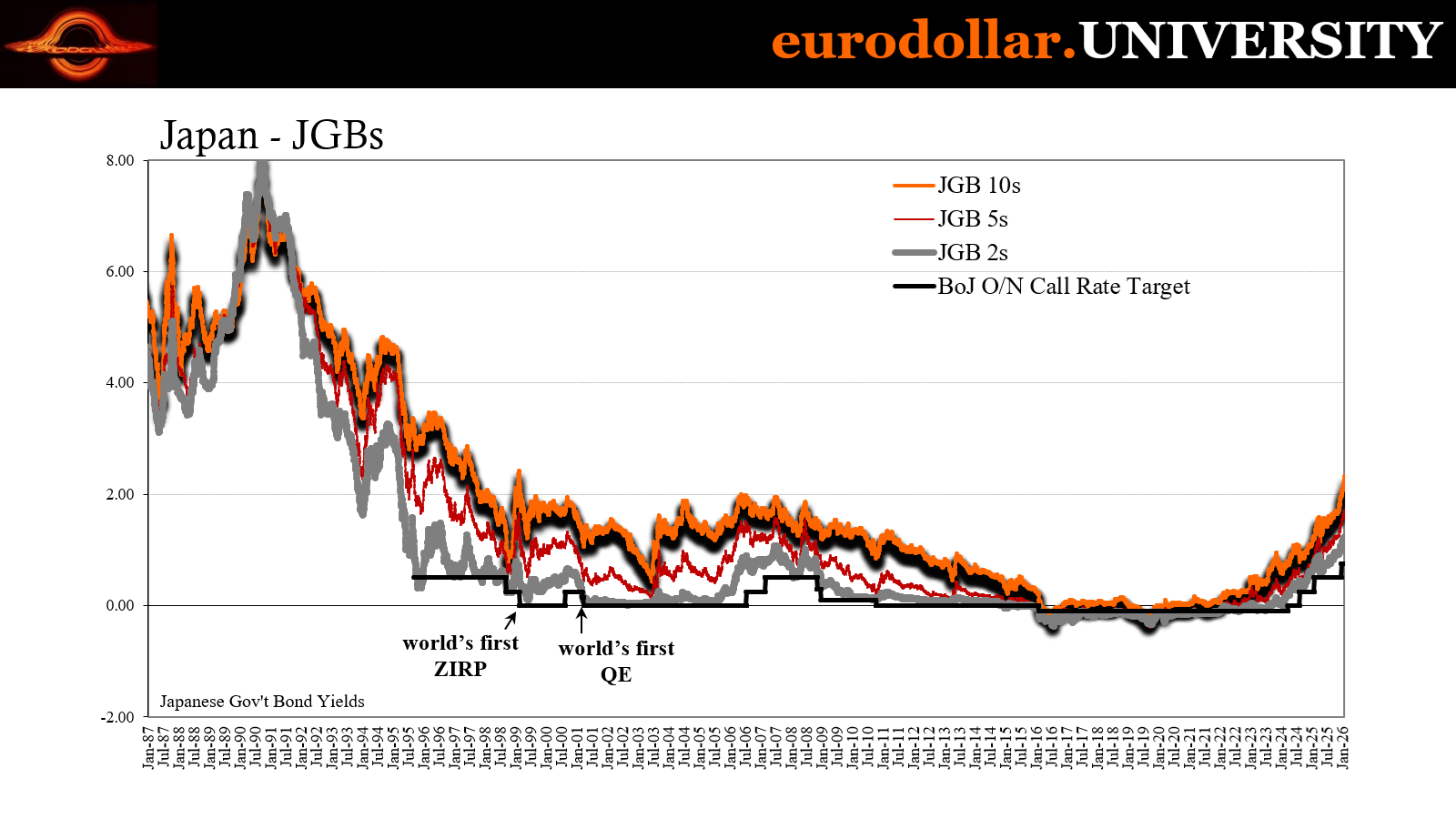

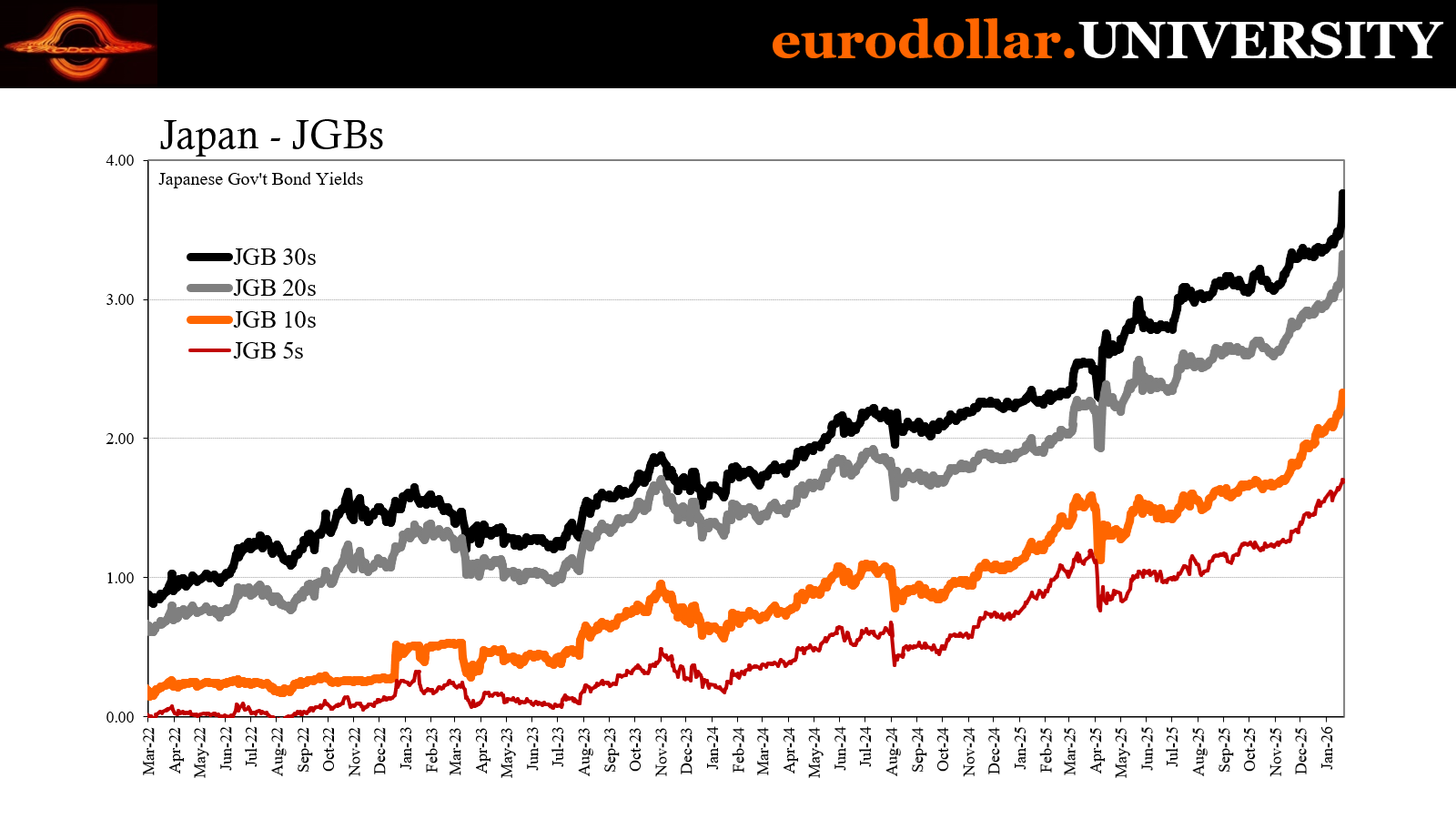

Japanese bond yields continue to behave erratically, seeming to some as a signal bond vigilantism has returned perhaps with a vengeance. Yields over there have soared, particularly more recently, but by all honest accounts (agenda-free) not for fundamental reasons. Instead, the problem is a mix of policy missteps combined with the natural inclination among (formerly) big JGB buyers to protect themselves from the fallout of those mistakes.

It’s a buyers’ strike, not rejecting government deficits.

SOME BADLY NEEDED CONTEXT

At root is the eurodollar’s impact on the yen and why it isn’t performing like the textbooks all say. But since the Bank of Japan will only follow the textbook rather than the evidence, this thing with JGBs has spiraled unnecessarily for largely political purposes.

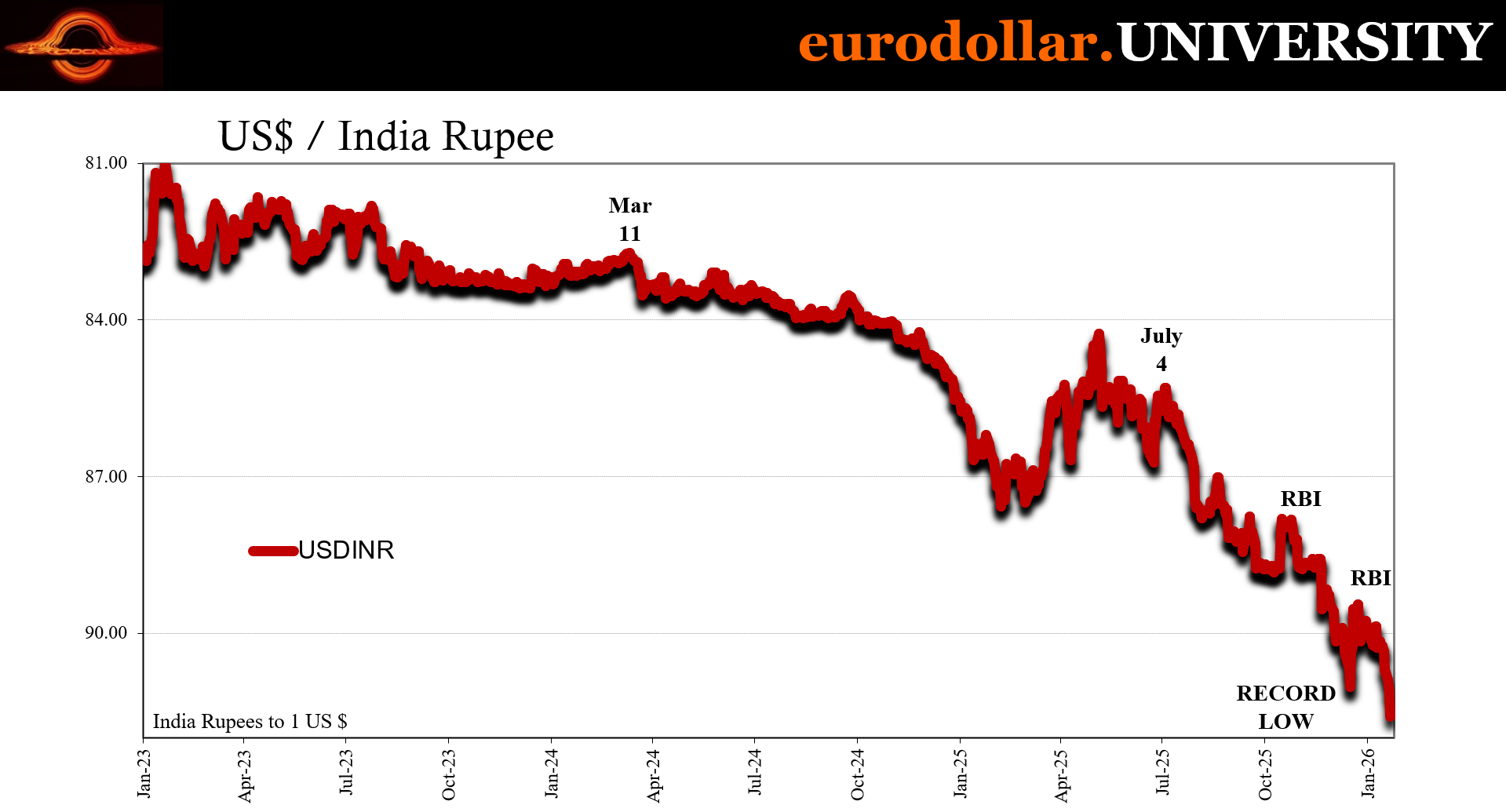

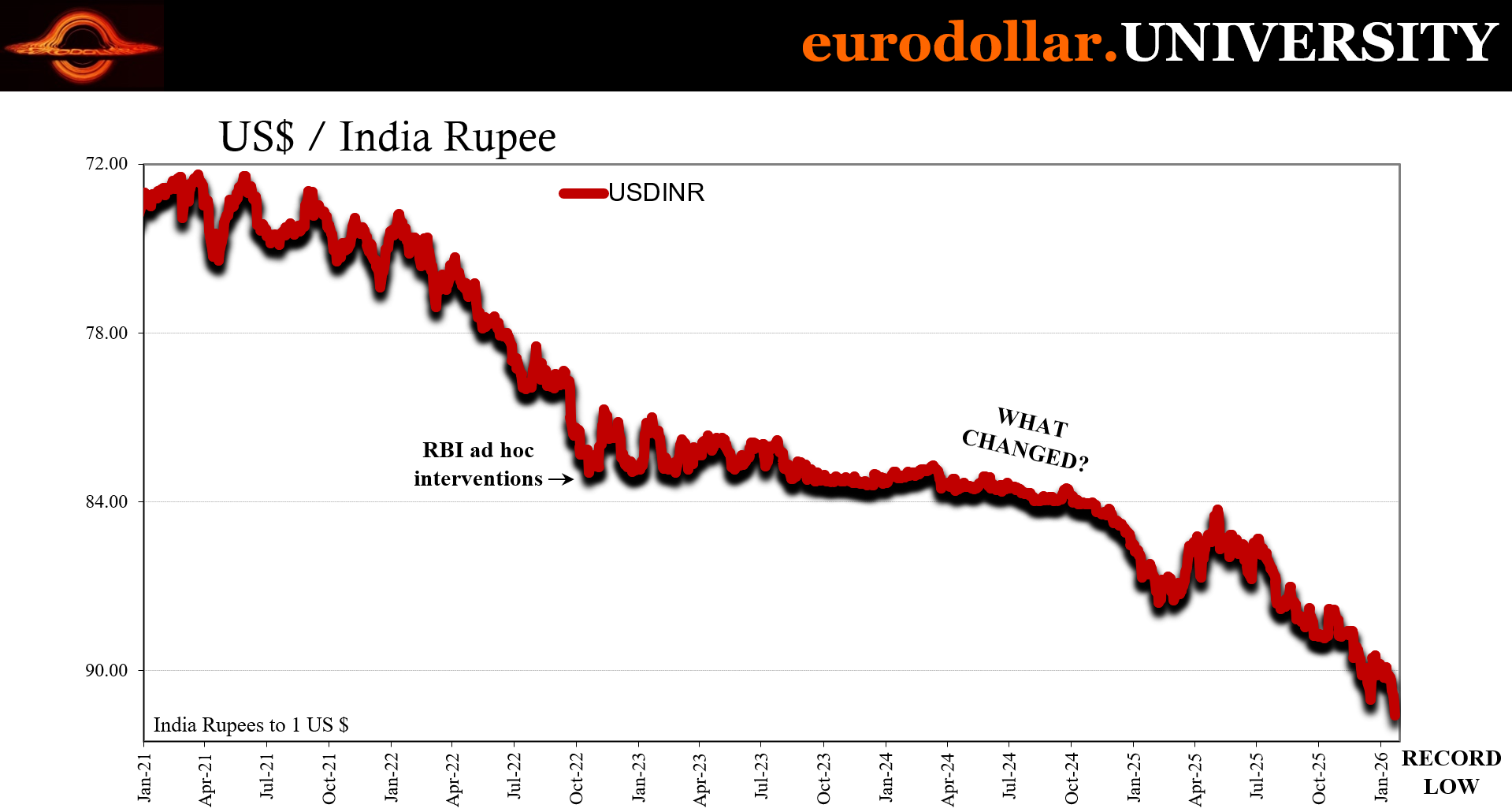

That is the “thing” where it comes to government interference. Not intervention, they can call it that all they want when at most it creates volatility, potentially harmful, and maybe some short run results which quickly fade once the system gets back to going where it was going to go anyway. We have any number of examples recently, including India and South Korea.

Both of them have performed attempted currency rescues and neither of them have produced tangible results beyond the very short run. RBI, for example, has expended a reported $45 billion in its latest rupee “rescue” while also incurring the local costs of that effort in the form of interbank illiquidity (rupees necessarily bought through “selling” dollars end up being locked away from the banking system).

INR just plunged to a new record low today anyway. Korea’s won has very nearly unwound its recent government-inspired rise. And all of it confusing the hell out of everyone who thinks governments control currencies via interest rate mechanisms when that hasn’t been the case in at least a half century, assuming it ever happened or ever happened so simple as that.

The implications are certainly profound enough. The JGB issue alone is creating expectations for bond vigilantes the world over – if Japan has finally reached a limit, what does that mean for all the other reckless capitals around the globe?

Even if that was true, not what everyone seems to think or want.

When buyers go on strike

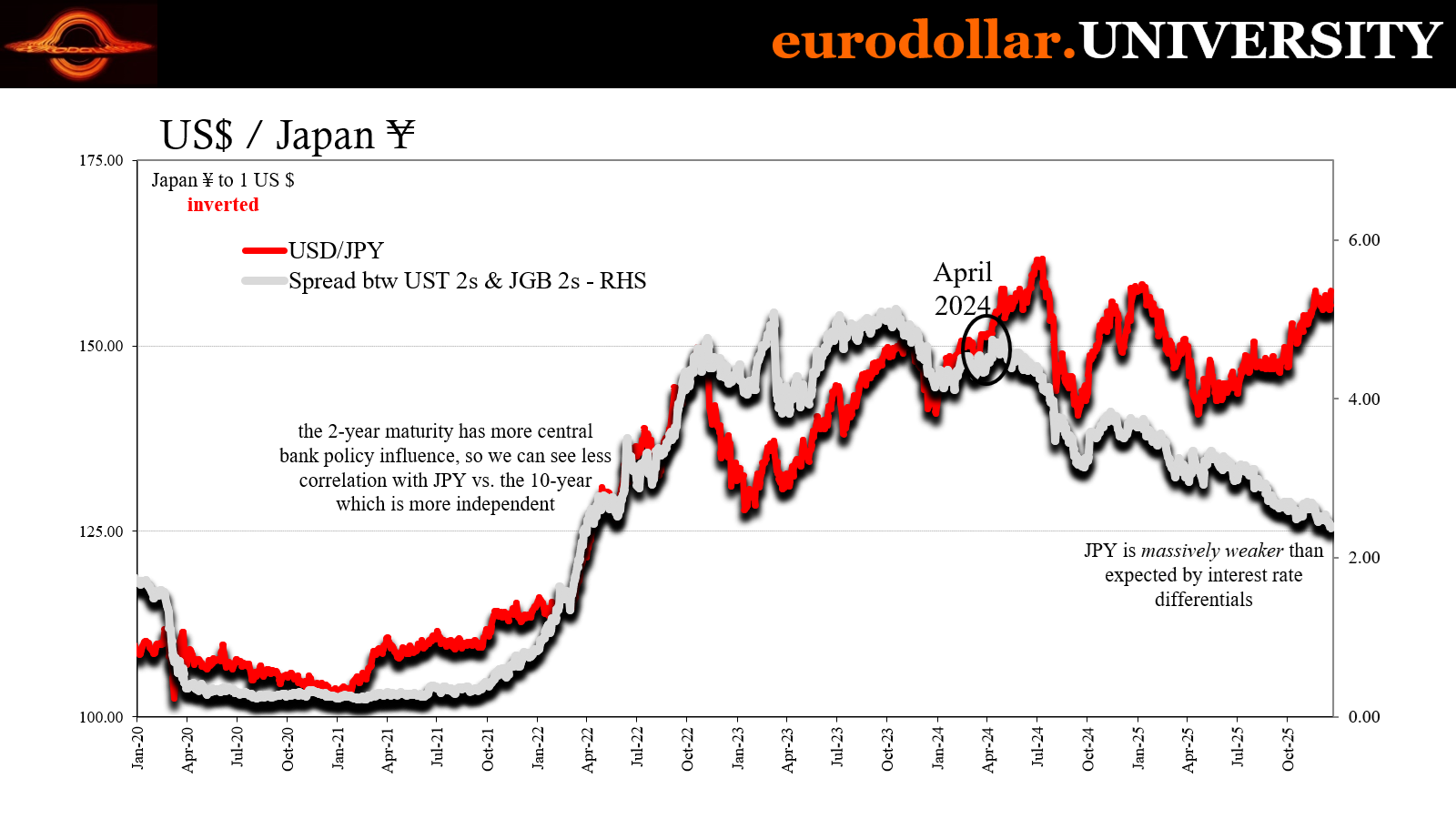

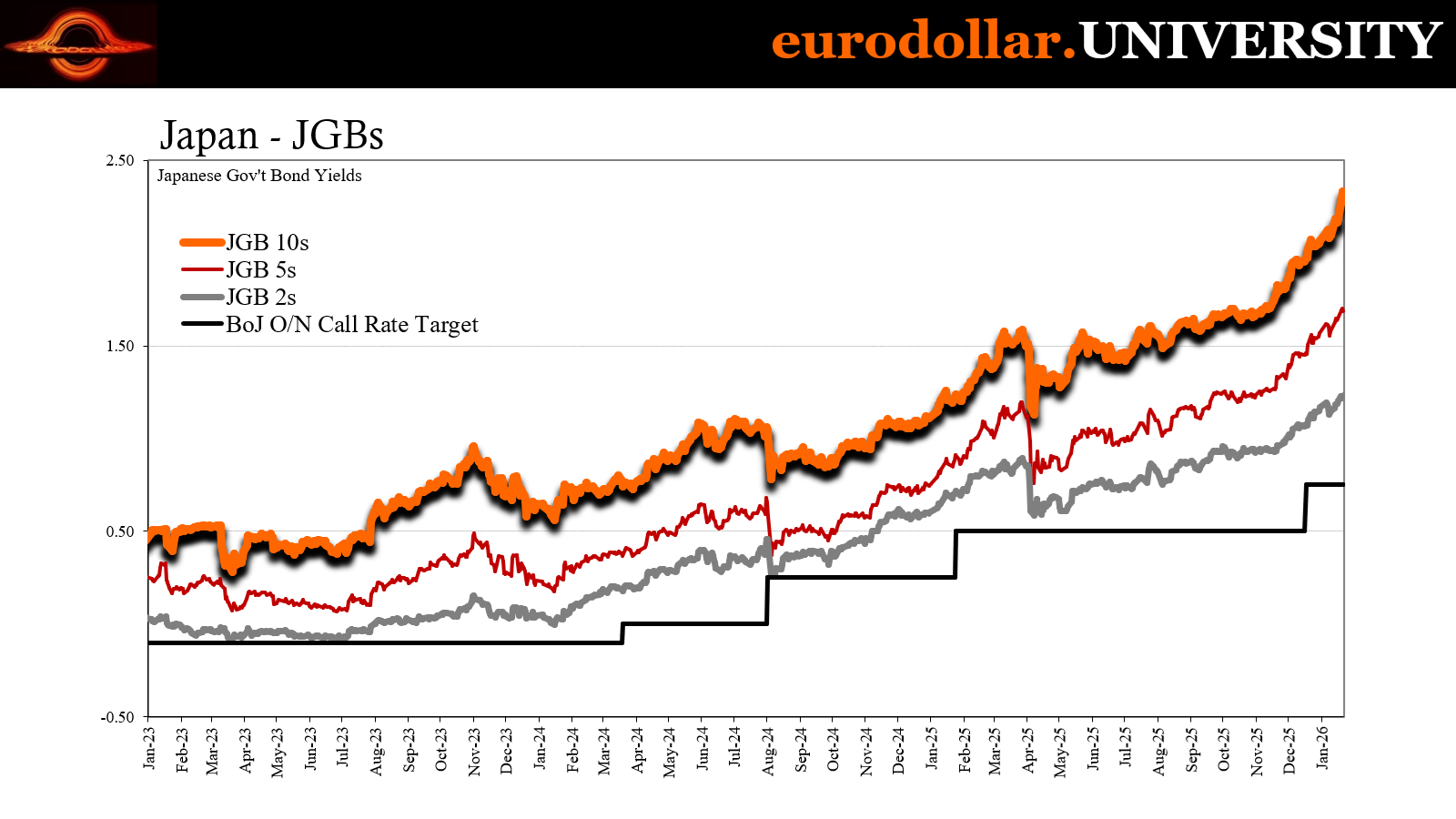

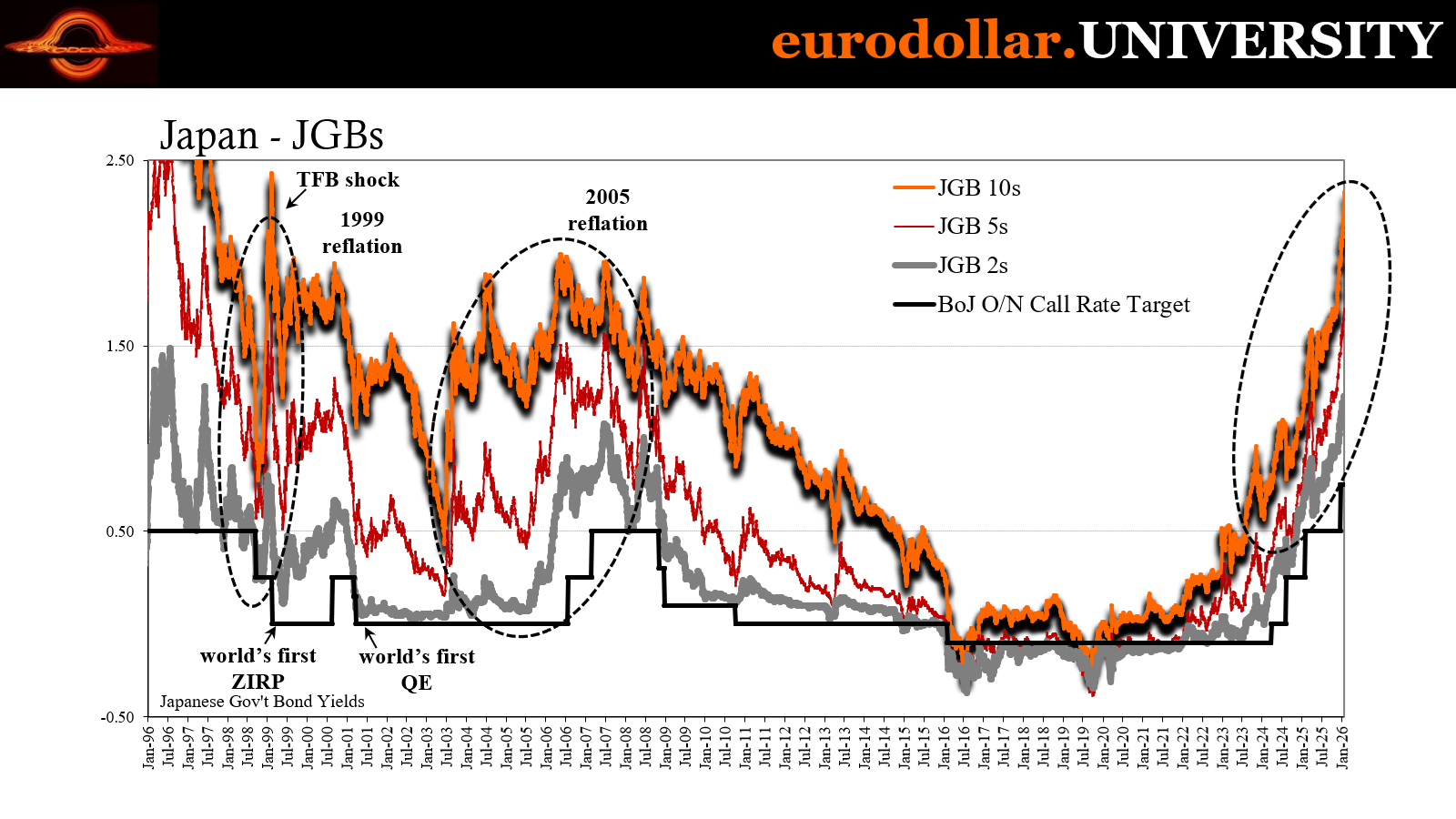

The Bank of Japan is pretending it is attempting to fight against inflation with its rate hikes when in reality officials in Tokyo are really after the yen. JPY’s weakness does feed into domestic consumer prices, sure, but that’s not really the main issue. Policymakers are following the textbook version of currency exchange which declares central bank interest rates as the primary factor for fundamental currency values.

This is another one of those you don’t have to take more word for it. Government officials as well as central bankers have repeatedly stated they believe the yen is far weaker than its “fundamental” value would have it, a value they base on the difference between US$ interest rates and those drawn from the Japanese market (presumed to be determined by central bank policy).

More recently, officials have grown more explicit in admitting Japanese rate hikes are less about domestic consumer prices and truly aimed squarely at JPY.

But that simply begs the question why the yen is weak in the first place to the point it would radically deviate from those government fundamentals. Authorities don’t have any good answers for that conundrum, instead meekly pointing to “one way” trades as if speculators could ever control such major FX for any longer than a few minutes, perhaps a few microseconds.

What Tokyo is really saying is they don’t know why JPY is down and have no good idea what to do about it apart from the standard approach.

Thus, the rate hikes will have to continue.

But, as the BoJ threatens to chase the yen with its policy, that has made it increasingly difficult for JGB market participants to hang on to JGBs or buy more of them; buy any of them. The more it appears as though Kazuo Ueda will prioritize the weak yen, the more relatively higher policy rates can create potential losses in JGBs.

It is basically the same proposition as what led to the spark of the US banking crisis in 2023, if on a much slower timescale (the 2023 event was not really about UST values, but how those played into an increasingly difficult funding environment which forced the system to start culling its weaker members including that one bank in Switzerland which had nothing to do with US regional banks). Put yourself in the shoes of one of the big Japanese insurance companies, traditionally the biggest buyers of JGBs.

Ueda has essentially laid out a policy course which threatens the value of massive amounts of your holdings. Even if the market doesn’t agree with the reasons why BoJ might raise rates, the truth is under these circumstances irrationality on the part of policymakers can lead to a self-reinforcing, self-feeding selloff.

Especially when there isn’t as much depth to the overall market, as in Japan’s case. That means smaller pullbacks produce greater price movements, higher volatility therefore even more reason to stay out of it.

It starts slowly at first, as insurers and pension funds sell some of their JGBs at the margins understanding a few rate hikes would have outsized negative price impacts (convexity). Any JGBs that are intended to be held to maturity would be unaffected. Those not considered reserve assets, however, would be, especially if pledged as collateral that gets increasingly less usable as their price goes lower.

The selling starts slowly as does the reduced buying. And the more the BoJ shows it will stick to its current policy trend, the more pressure on the market – again, not for fundamental reasons, not for growth and inflation expectations, but the uncertainty created on JGB prices over what is ostensibly a currency matter beyond all official control.

As you might expect, the longer this goes, the more selling feeds on itself and creates price volatility which means higher potential exposure to falling bond prices and perceptions that are driven even farther by official irrationality. After some point, buyers would essentially refuse to participate – the buyers’ strike.

That is where long end of the JGB market is right now and, as with so many of these, this is not something you need to take my word for. Here it is once more from the horse’s mouth:

Japan’s second-biggest bank plans to aggressively rebuild its local sovereign debt holdings once a wild surge in yields runs its course.

Sumitomo Mitsui Financial Group Inc. is prepared to increase its Japanese government bond portfolio to as much as double the current ¥10.6 trillion ($67 billion) after it makes a full-scale return to the debt, global markets head Arihiro Nagata said in an interview.

Obviously, Sumitomo is massive and a huge player in the market and it wouldn’t be even contemplating a return to JGBs if government deficits were the primary reason it has been sitting out so far. If fear over some debt limit were motivating the selling, the selling would continue until default or fiscal sanity (so, default).

What Sumitomo is doing is simply waiting for that moment when Ueda wakes up and realizes he can’t rate-hike his way to a stronger yen. Once the possibilities of further bond price declines decline, Sumitomo and everyone else comes back into the JGB market once again and probably very happy to do so picking up cheaper bonds paying higher rates and featuring enormous snapback appreciation potential.

Eurodollar controls Japanese rates

S Mitsui is hardly the only one which has come right out and said blame BoJ. Here’s an earlier example I’ve pointed to before, this one from another titan Mizuho:

Mizuho Financial Group Inc. is managing its securities portfolio “very conservatively” as Japan’s third-largest lender prepares for the next investing opportunity after shrinking its bond holdings.

The bank wouldn’t build up big positions until it is confident the Bank of Japan isn’t likely to raise rates any more, Chief Executive Officer Masahiro Kihara said during a question-and-answer session with the media on Tuesday.

Mizuho has cut its positions in foreign and Japanese government bonds, Kihara said. It slashed its JGB holdings to ¥8.3 trillion ($57 billion) as of March, from ¥25.1 trillion three years earlier, according to an investor presentation. While its foreign bond holdings rose from ¥8.9 trillion to ¥11.8 trillion over the same period, they dropped from a year earlier as the firm realized losses.

The more the BoJ sticks to its ridiculous plan, the more buyers will sit out the JGB market until some point when the prices get to be so low the enormous potential returns will convince enough of them to take the risk of any further policy rate hikes. But no one knows what price level that might be or when that could happen.

What does happen is buyers remain on strike until the price goes too far or BoJ begins to demonstrate some rational thinking. I’m thinking everyone is betting on the former rather than any chance of the latter, therefore JGB ultra-long yields keep going until that unknowable price level triggers.

Whenever that is, back to Sumitomo:

Sumitomo Mitsui’s JGB holdings most recently peaked at ¥15.8 trillion in March 2022, but Nagata said that was mainly short-term notes bought for collateral transaction purposes. “We will rebuild the amount far bigger than that,” [Nagata] said.

Central banks are the greatest source of financial uncertainty there is when their mandate is the exact opposite. And the reason why is the standard practice of Economics which gets basically everything in economics wrong and backward.

Japan and its JGBs another case in point.

Awash in official noise

India and South Korea are two recent examples of the foolishness of trying to tackle the FX problem. That problem begins with a fundamental misunderstanding of all these currency dynamics, including the nature of ledger money itself.

People wrongly equate exchange rates to a currency’s value in the same way they think of a stock price. This is incorrect. A currency doesn’t have a “value”, its price reflects ledger money flows and therefore the exchange “value” is merely a relative gauge of those flows (broadly speaking).

One of the key features of the eurodollar system was its fundamental focus on being an exclusive medium of exchange. How could it really have been much otherwise? A virtual, fictive ledger money system - by definition - doesn’t produce physical tokens that can be removed as stores of value. What’s left is really returns on the same book entries as what counts for this “currency.”

For those, competing rates and yields from financial markets quickly absorbed that sometimes-competing monetary function. As was said from the eurodollar’s earliest days, the Eurobonds of lore, it became a full-fledged, soup-to-nuts monetary regime. No physical cash was necessary, in fact none was really ever desired.

What governed use was nothing more than accounting conventions, many of which were defined for and from a bygone era to placate always-way-behind regulators. Return-hungry participants sought out different definitions rather than pieces of paper.

For instance, if you wanted to transact, to employ the eurodollar’s medium of exchange, you’d have to transfer – by book entry – whatever existing book entry balance into an account specified to be that exchange medium; checking or however necessarily described.

When not in need of readily available funds, the numbers shifted, book entries made so that you’re available to “invest” across a wide variety of financial markets. And when making that investment, your funds transfer from one book entry to the next. The borrower gets credited with a transaction balance while you shift into an investment account of some kind (including brokerage).

Back and forth this virtual money shifts between usable and investable; from mediums of exchange to stores of value then back again, easily keeping separate those basic monetary functions because there is no real money or currency; just accounting.

This methodology crossed nominal denominations, too, as you’d expect given that the eurodollar is basically the other side of nearly every global transaction. As Dufey and Giddy had more than adequately described way back in 1981 (if only officials and Economists were paying attention):

The remarkable feature of this use of forward contracts in the Eurocurrency market, for example, is that it enables banks to offer deposits or loans in any currency for which there is a forward exchange market, even if no external money market exists in that currency. The result is that the Eurodollar is the only full-fledged external money in existence; other Eurocurrencies are often simply Eurodollars linked to forward exchange contracts.

This is because “Eurocurrencies” such as represented in forex “are often simply Eurodollars linked to” in this case mostly currency swaps. Basically, all the other forex swaps swap into dollars as the preeminent global medium of exchange.

Hardly anyone goes directly from, say, sterling to Canadian dollars, rather they mediate through US dollars (meaning eurodollars).

In other words, the needs of the system and conditions within it are what dictate currency translations, what are misleadingly called exchange values. Governments are effectively powerless in the face of some of the more intractable circumstances from within this blackhole arrangement. Sure, “interventions” can produce short run effects, even sizable ones, yet there is little staying power to them since those effects are largely limited to the margins, oftentimes speculators playing those margins.

A massive dollar selling campaign by RBI, for example, can move the FX price on a given day which could and does prove costly to those who are purposefully short the rupee (as in, making directional bets on the currency most of the time using leverage). The price of INR goes up when the central bank shows up, forcing short covering and the like from the speculative end of the market.

Even that, however, is about the flow of currency – in that case, RBI is providing a short run flood of dollars (“selling” dollars).

That does nothing to alter the needs of everyone else who are taking actions for reasons that have nothing to do with the exchange rate (especially since most transactions take care of exchange risk in some ways, either hedged or, in the case of something like swaps, it’s written right into the contract terms). What determines a currency’s more-than-short-run direction are the flows within all those unseen book entries.

INDIA NEEDS TO BORROW MORE TRADE DOLLARS BUT THE EURODOLLAR HAS ONLY GOTTEN TIGHTER SINCE 2007, THUS RUPEE

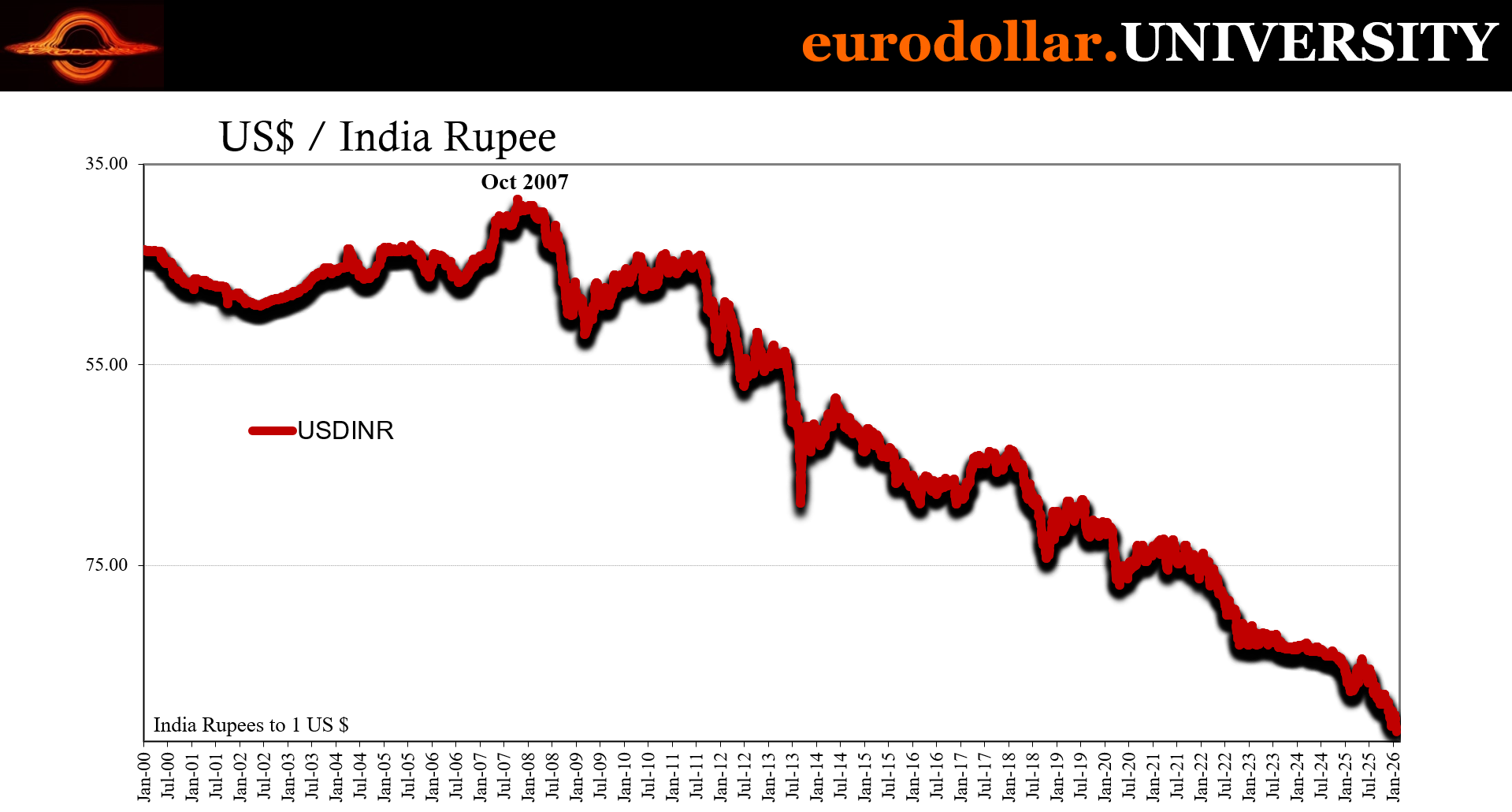

For India, the rupee’s long run weakness (going all the way back to 2007) is really easy to appreciate (pun intended). The country buys more overseas than it sells. That means it will need constant new sources of ledger eurodollars which have to be borrowed from the eurodollar system. The greater the trade deficit, the greater the need to borrow and the more pressure on the rupee.

And should the eurodollar lenders become fickler about lending, the more the rupee will have to “pay” the premium regardless of interest rates or RBI pretenses.

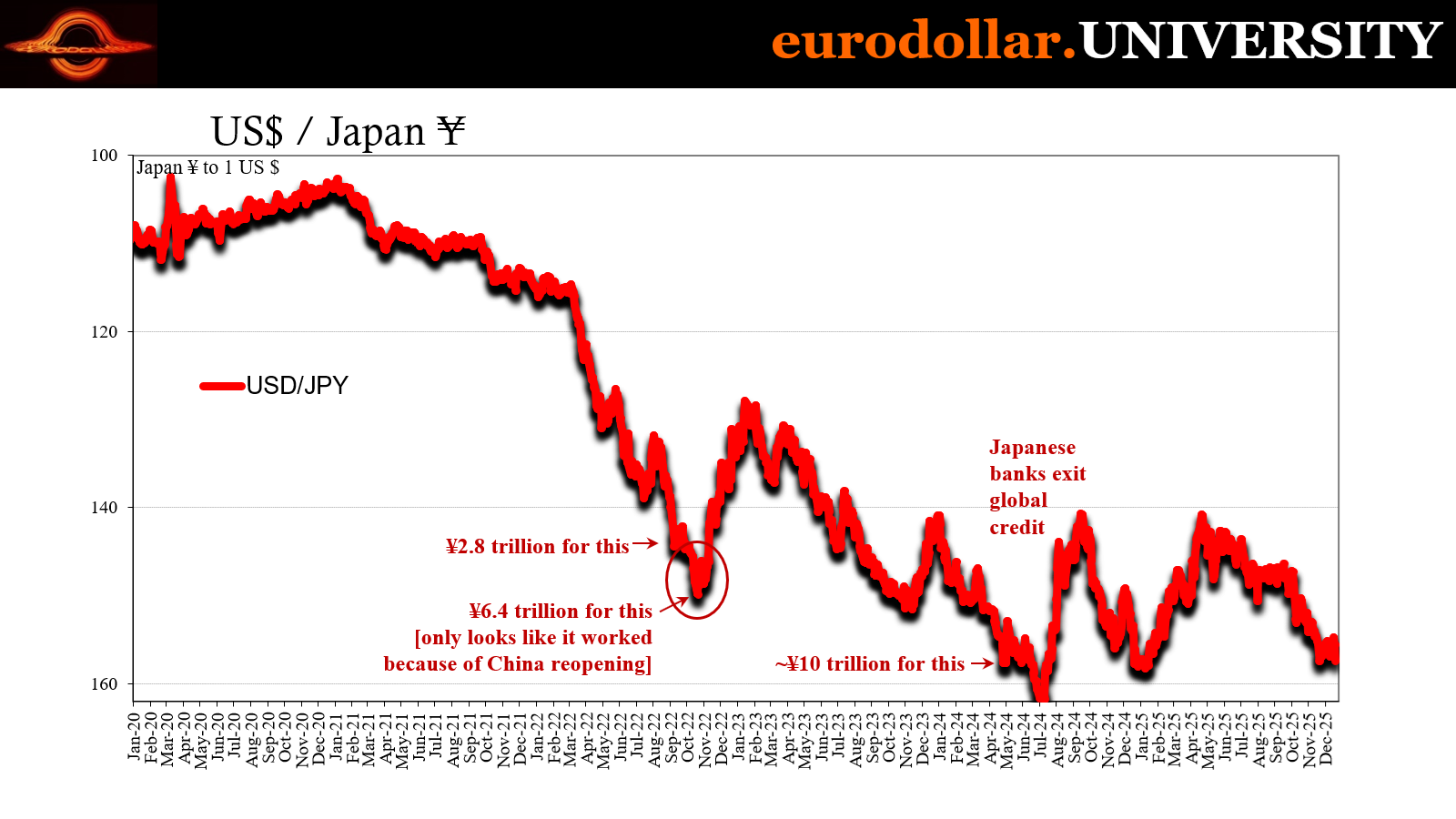

Or Bank of Japan, as in the case of the yen.

Eurodollar mechanics are fundamental.

For Japan, those have created this weird vortex which now extends deep within the JGB market. The tighter eurodollar flows aimed at Japan, the lower the yen will go. As JPY falls, the more the Bank of Japan threatens to raise its short-term policy rate which provides even more justification to the JGB buyers’ strike.

A tighter eurodollar system gets translated into higher Japanese bond rates!

Why? Because central banks are the greatest source of financial uncertainty there is. Take them out of this equation, the yen is still in trouble, that doesn’t change, but you wouldn’t have the rate hikes and threats for more which would mean Japanese insurers and banks would be buying JGBs on the regular instead of sitting them out.

You could argue, as anyone following the Economics textbook might, the central bank is simply exercising “control”, even if indirect, over market yields in order to affect its policy. However, it is still ineffective because the yen is falling anyway no matter how high Japanese interest rates have gone, policy or market. BoJ is creating volatility in the bond market for absolutely nothing gained.

They can’t even say it is restraining “inflation” because supply factors in Japan are creating those price pressures and so don’t react to interest rates one way or the other.

Instead, this whole thing is really designed for headlines and perceptions, knowing that most of the general public – the voting public – doesn’t pay much attention to details. The average Japanese isn’t going to be connecting dots on JGB yields to eurodollar flows and how little the central bank is impacting either. BoJ is raising rates so that officials can say they’re doing something.

Doesn’t matter that something makes no sense, produces no tangible results, and is in too many ways counterproductive. Or exactly what QE has been, too. It’s all performative, entirely theater.

If only it was vigilantism, that would be terrific. Fiscal restraint is long overdue. But even if that was the case, Japan is so far down the deficit rabbit hole, so far ahead in terms of its outstanding debts, it wouldn’t apply to anywhere else. DC, for example, still has a long way to go just to get into the same ballpark as Tokyo. A frightening thought all its own.

And that’s why as a far distant tomorrow problem bond investors overlook governments’ credit profiles in favor of what can impact them today. Depression economics.