CLOSE THE DOOR ON TARIFF INFLATION

EDU DDA Jan. 13, 2026

Summary: December’s CPI won’t finally kill off tariff inflation, though it should. The idea remains on life support solely because Economics isn’t a science, and those who follow it aren’t interested in facts or truth. How did it get to be this way? Why did expectations theory become so irredeemably embedded in this mainstream? As is usual, in the absence of credible information and factual assertions, Economists were left to just make up ideas to explain the world using their version of entrails and tea leaves. Tariff inflation is merely the latest to expose the sham.

LET’S BE HONEST, IT ISN’T ‘LIMITED’ IT DOESN’T EXIST

This was supposed to be revenge of the shutdown. After November’s CPI was criticized for being something, it was too low, they said, December was scheduled to produce a spike and get the tariff inflation idea back on track. But superstitions are nothing to go by.

I often reference the study by Jeremy Rudd, formerly of the Federal Reserve Board, simply because on his way out the door he finally said what should be common knowledge. Rudd was and probably still is a well-respected researcher, therefore straying so noticeably far from the ideological box Economics has put everyone in stood out and continues to stand out. He heavily criticizes these theories in those most damning economic terms.

The theory itself sounds plausible enough, like a lot where it comes to astrology. It says if you believe inflation is going to be a persistent problem then you might begin to act on those instincts to then become the inflation. This all stems from the missing money of the seventies and before; without being able to locate the monetary reason for “great” inflation, Economists had to come up with something else and expectations seems just reasonable enough.

Though, as Rudd also pointed out, there was the overwhelming desire to fix econometric models, too.

After a year of hearing about tariff inflation, there remains no evidence for it. On the other side, flat Beveridge isn’t an idea it has become established fact, including by the Establishment Survey to the point none other than Jay Powell has had to concede as much. Somehow the tariff inflation noise remains a fixture of Fed discussion, both internally as well as externally as interested observers try their hardest to ascertain when the irrational might begin acting slightly less superstitiously.

Welcome to 2025 and 2026’s version of yield curve steepening for an economy that once again isn’t doing what it is supposed to.

Blame Iraq?

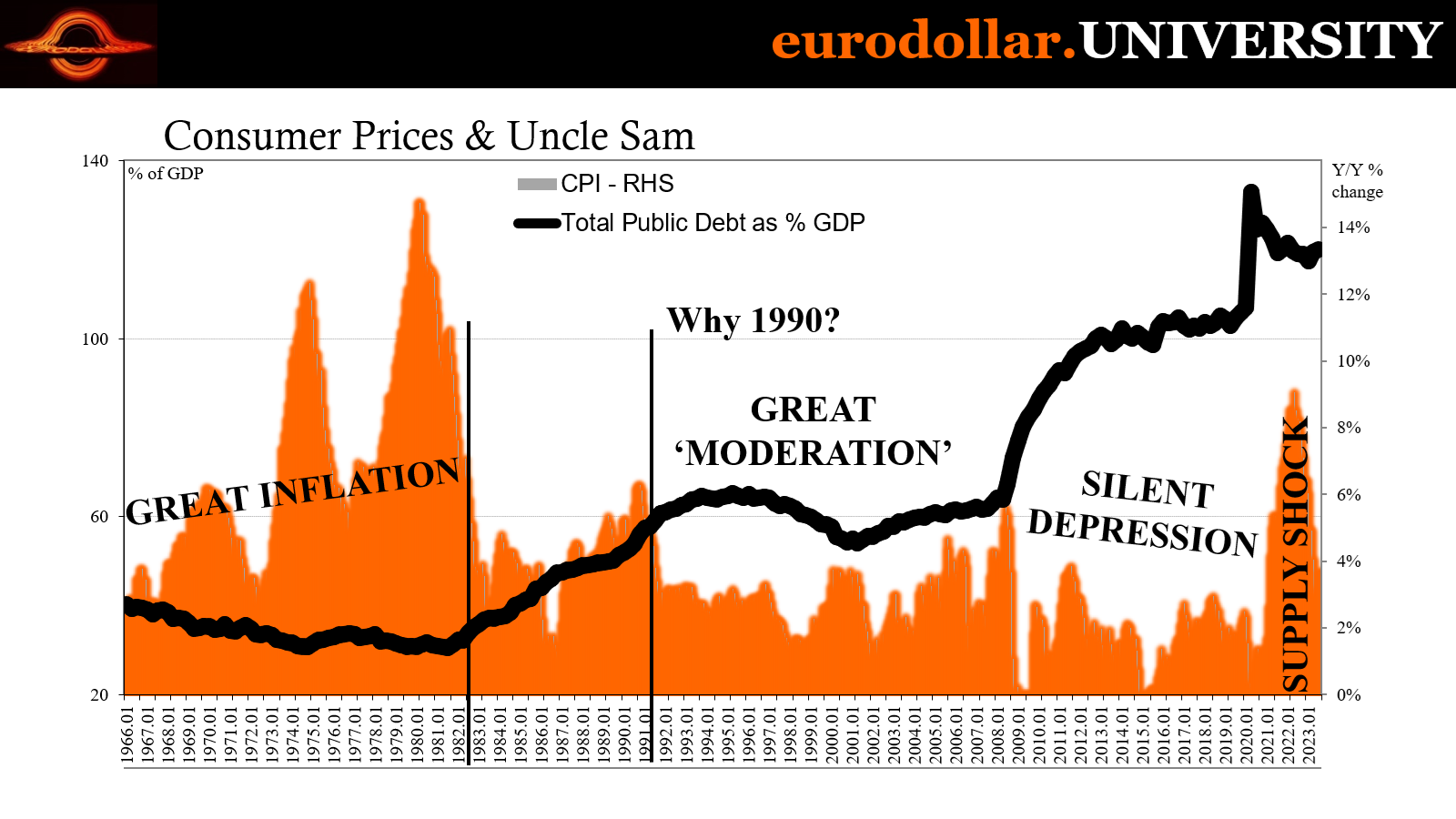

Compared to the utterly turbulent world of today, 1990 wouldn’t really rate all that high on any reasonable scale of years to remember. Saddam Hussein’s Iraq would invade Kuwait kicking off the Gulf War, sure, but thirty-six years later the costs of its legacy absolutely drown the original episode rendering it an almost forgotten footnote; a quaint association, at most.

There was also a recession which began almost concurrently with the foreign military operation. No more than correlation in time, the contraction was an especially mild as well as brief one following what had been nearly a decade of unqualified and unbroken prosperity. In the landscape of historical business cycles, the 1990-91 recession sits at the bottom of any list of those to remember.

Given this, there doesn’t seem to be any good explanation for why 1990 serves as an absolutely crystal-clear demarcation between the last remnants of the Great Inflation and the middle meat of the so-called Great “Moderation” which followed. To put it bluntly, something substantial had changed after the eighties were over.

Naturally, suspicions might be drawn to the downturn itself. Economic theory posits that, Phillips Curve and all, rising slack means lower inflation. Short run, yes; long run, how?

It is a vexing riddle which has plagued Economic (Capital “E”) theory for these three and a half decades since. The “science” behind inflation seemed to have been settled during its “greatness” eruption of the seventies. In that decade, Milton Friedman, Robert Lucas, and so many other mainstream luminaries had developed passable theories about how inflation must have worked – and how for too long it had been left to go so wrong.

Expectations theory came to dominate mainstream thought, only bolstered with the arrival of Paul Volcker at the Federal Reserve in place of the near-universally vilified (with good reason) Arthur Burns (the forgettably short stint of unqualified Bill Miller in between them). For many Economists and especially those working at central banks, a mere mention of the name of Volcker is all that’s necessary to explain the Great Inflation’s modest end.

In other words, a dedicated inflation-fighting central bank can not only impact the short run, it can hold major sway over the longer run but only through expectations. By “provoking” not one but two consecutive deep recessions (the double-dip of 1980 then 1981-82), however he did it (no one really seems to know the exact details, just the correlation timing downturns to outward associations of Volcker’s monetary policy), this allegedly established the immutable supremacy of skilled technocratic management.

Don’t Fight The Fed!

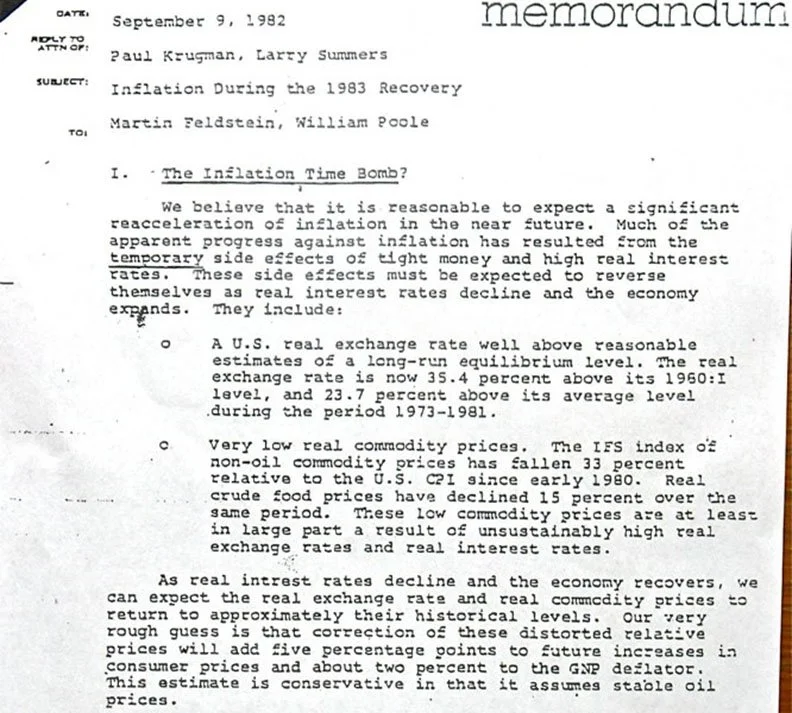

What followed the rest of the eighties, however, wasn’t exactly un-inflationary; on the contrary, at several points during the decade it appeared as if the inflation phenomenon was set to return. Perhaps most famous (and the lowest hanging fruit), Paul Krugman, working for President Reagan’s (yep, Krugman labored in the Reagan Administration) Council of Economic Advisors, he co-authored a memo with Larry Summers (yep, that guy) called the Inflation Time Bomb advising Martin Feldstein of serious caution.

Its key part:

We believe that it is reasonable to expect a significant reacceleration of inflation in the near future. Much of the apparent progress against inflation has resulted from the temporary side effects of tight money….

Reagan’s economic plan, the pair argued, “will add five percentage points to future increases in consumer prices.” Fighting “the man” from the inside, as it were.

Instead, the Great Inflation failed to return, but that didn’t mean inflation was absent. On the contrary, it would average a nearly steady 4%, not great, either, until something changed in and after the events of 1990.

A second missing money mystery

But if Krugman, Summers, and most of the rest of their orthodox clique of Economists were wrong about the eighties, they were doubly stumped by the nineties. Lower inflation still, a true moderation in global consumer prices with no obvious reason (or combination of reasons) why the turn of the calendar from eighty-nine to ninety could be so crucial.

Volcker, then Greenspan?

Many came to wonder and more so wanted it to be effective monetary policy aimed at controlling people’s expectations. In short, Volcker “establishing” an inflation-fighting central bank while demonstrating its purpose could credibly limit the reach of consumer prices (even though it didn’t happen straight away; again, there was some serious inflation in the eighties, a fact obscured by the immediate comparison with ungodly inflation during the preceding seventies).

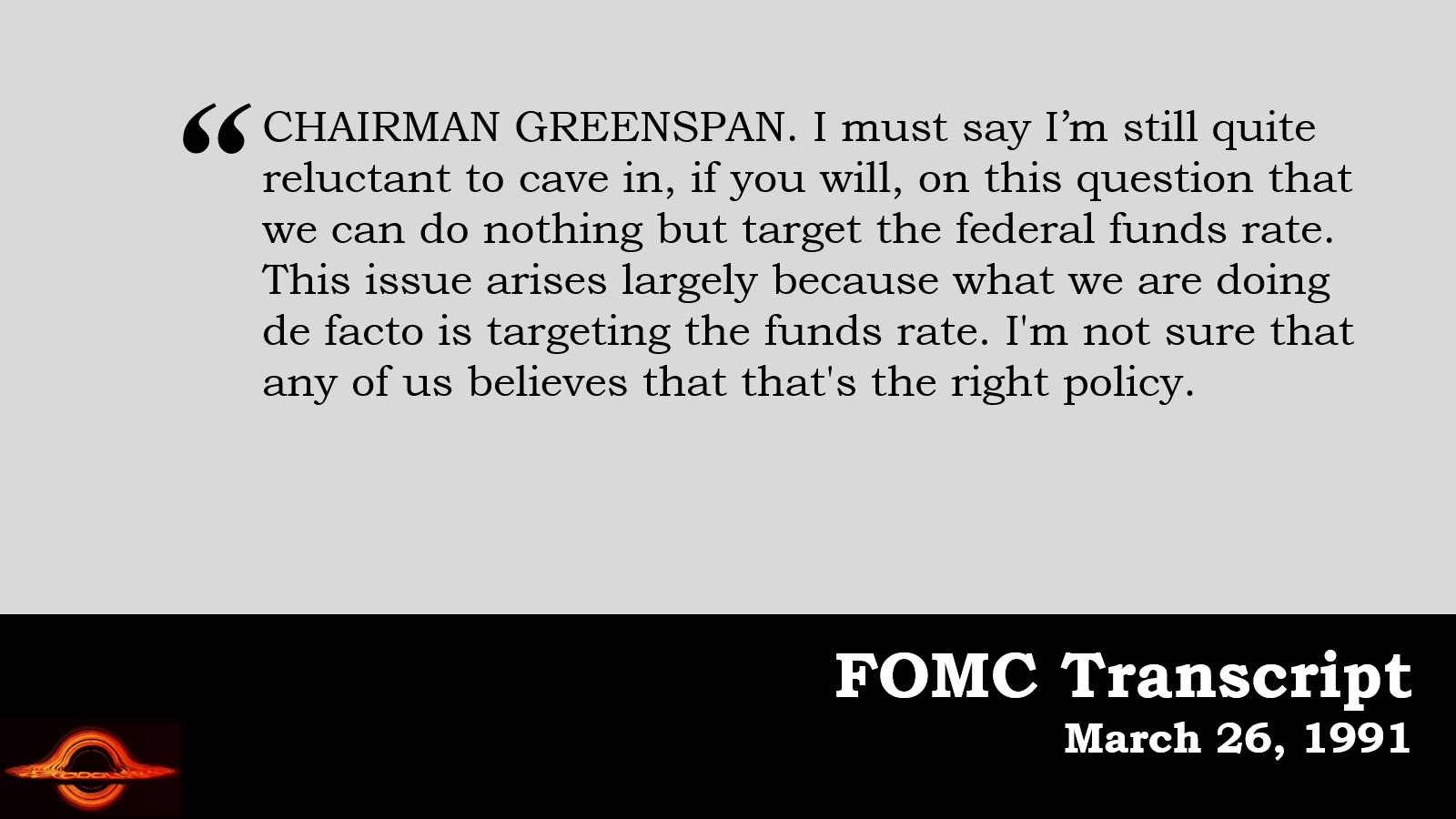

Perhaps, then, Volcker had created the expectations template which appeared to work moderately well before it was then passed to Alan Greenspan, his immediate successor, for him to perfect. Conventional history even now assigns great skill and aplomb to Mr. Greenspan first during the Crash of ’87, then the S&L Crisis, finally crediting him the original “successful” demonstration of interest rate targeting for the mild and temporary 1990-91 recession itself.

Already your first clue this is all just wishful thinking (Greenspan lowered the fed funds rate, got the recession anyway, then cost Bush Sr. his office when there was no recovery immediately afterward despite all the rate “stimulus.”)

Was 1990 the year when this new monetary policy doctrine shown the brightest, showed the world how it was done, and thereby rammed down the ceiling on consumer prices for decades to come?

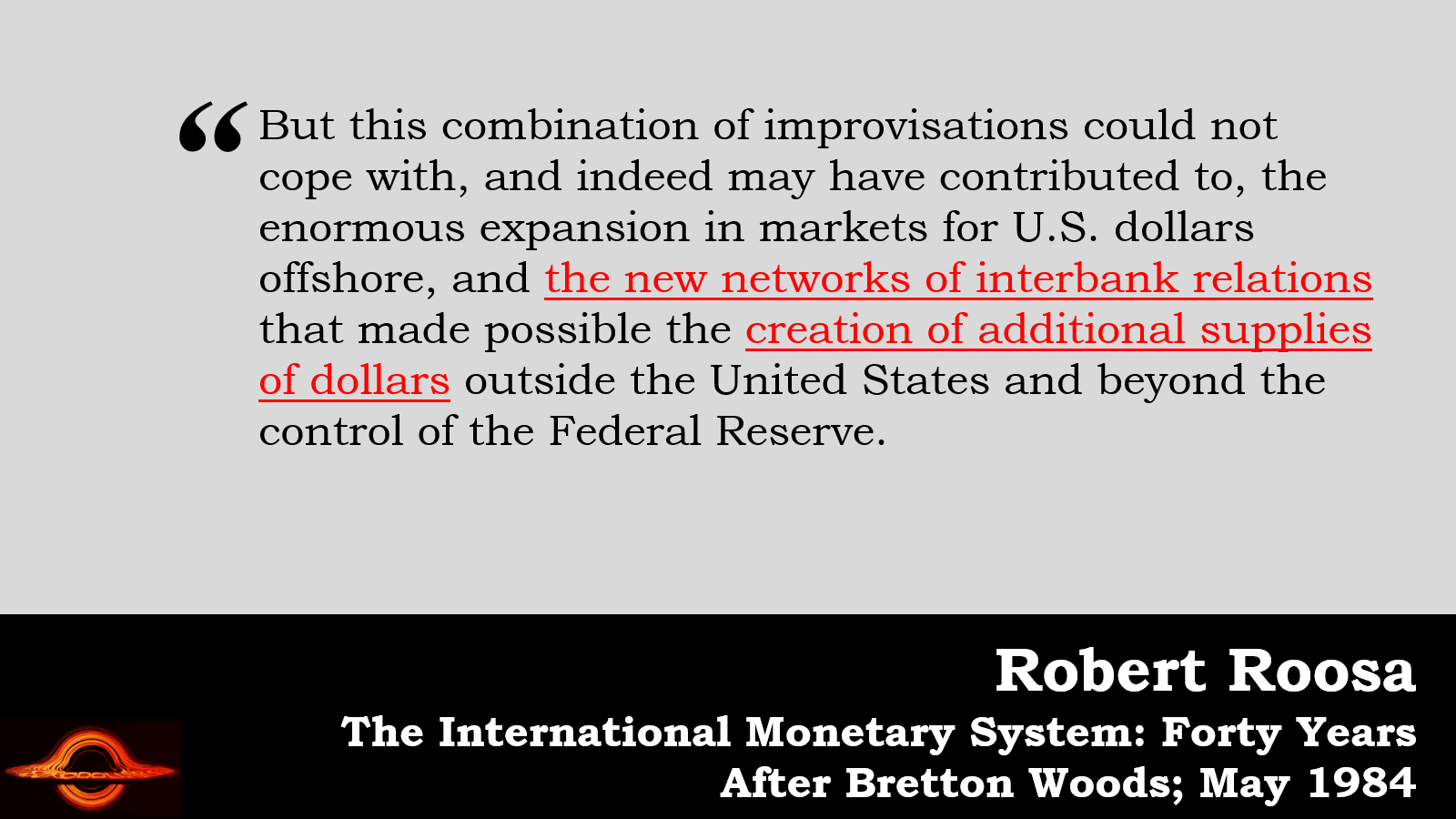

What convention gets wrong – to this day - is the “tight money” presumed of Volcker’s age. Money got tight as a matter of mistakes not policy and then it went elsewhere (this is where I remind you of Robert Roosa’s ‘84 quote about “new networks of interbank relations” “beyond the control of the Federal Reserve.”)

As I covered extensively in yesterday’s DDA, massive monetary evolution from the fifties forward never stopped even if the consumer price inflation would. Transitioning toward a mature state in the eighties, monetary growth began to more seriously explore other untapped regions beyond simply the US border. Too much money tended to chase too few goods in the seventies, then just loose enough money would chase non-American (and more financial) opportunities in the eighties.

The eurodollar system had spent the decade before pulling open and widening the doors of true globalization, which right around 1990 had unlocked an ocean of previously untouchable labor. Deng in China, Eastern Europe, they all welcomed the flood of eurodollars. Everyone rode the resulting wave of prosperity, save the unfortunate souls in places like the Rust Belt who were muscled out of the next industrial wave.

Yet, Greenspan was quickly anointed the “maestro” having stitched together his own snappy suit from Volcker’s coattails. The myth of the inflation-fighter Fed (and other central banks like it) has been omnipresent in mainstream discourse because of what’s always left out of its models – and what has been inserted, by necessity, in its place.

Economists, quite simply, cannot explain this economic history without this myth. There is no way to reconcile reality with their equilibrium models absent expectations being central to inflation conditions; and effective expectations interest rate policy being the supposed engine of that benevolence.

The 2008 shock shook everything including bad theory

While this may have sounded plausible during that Great “Moderation”, first it was only this way because of the assumption national economies operate as distinct islands; that there is no true global economy, merely a loose confederation of patchwork nationalities with little influence between or even one from another. If inflation is low in the US, it gets presumed something US must be responsible.

But then the Global (not)Financial Crisis of 2007-09 “somehow” showed up, bringing with it global deflation and economic destruction unparalleled since the thirties. This despite the alleged performance capabilities of a technocratic apex central bank set deep into the public’s long-term expectations. We all believed in Greenspan’s guy, that fella Bernanke.

Not only did this show the world very strong evidence there was a globally-connected system after all, it further and rather neatly exposed these prevailing myths about central banks as, well, myths. Expectations? Who cared! Money, please.

Ever since, QE after QE after QE to play up inflation expectations to suddenly no avail. Given enough time and mountains of contrary evidence, this constant failure has aroused if only modest mainstream suspicions that something has to be off with Economic theory, specifically inflation and expectations.

Thus, the Federal Reserve Board’s Jeremy Rudd caused a minor stir when his paper Why Do We Think That Inflation Expectations Matter for Inflation? (And Should We?) excoriated just what its title says.

I don’t want to simplify too much, but essentially Economists believe in this expectations stuff because they want their econometrics to seem to work, but they won’t unless they can at least muster some kind of answer for especially inflation history surrounding 1990 (let alone the quarter century before). The DSGE’s need this other equation:

What I believe such a response misses [that all models are inherently flawed] is that the presence of expected inflation in these models provides essentially the only justification for the widespread view that expectations actually do influence inflation. [emphasis added]

Economists believe in it because they put this function in their models, not because there is any real-world proof it should be there. With it, their models (up to 2007) could fit the data - which is not how it’s supposed to work. Science isn’t made by back testing and retrofitting. As Mr. Rudd meticulously documented, empirical evidence for inflation expectations is seriously lacking – and it always has been!

And this goes straight to the heart of the main question, both inflation (specifically)/economy (broadly) as well as what it is central banks actually do. Is the Volcker Myth…a myth?

Second, the fact that inflation’s stochastic trend manifests its last persistent level shift after the 1990–1991 recession also seems relevant, in that it suggests that ‘whatever happened’ to inflation might be more related to its actual level’s having been kept low rather than to any ‘credibility’ that the Fed gained as an inflation fighter following the Volcker disinflation.

Put another way, what Rudd is saying is that the central bank, in particular (especially those like Bernanke who intentionally sought to tie monetary policy with the Great “Moderation”; see: Stock and Watson), invented expectations as a way to take credit for what happened thereby allowing it to further perpetuate both mainstream models as well as its stranglehold on total discourse.

And this apotheosis has occurred with minimal direct evidence, next-to-no examination of alternatives that might do a similar job fitting the available facts, and zero introspection as to whether it makes sense to use the particular assumptions or derived implications of a theoretical model to inform our priors (particularly when the ancillary assumptions of the model are so incredible and when the few clear predictions it makes are so wildly at odds with the available empirical evidence).

Yet, given all this, even after the multitudes of monetary failures only beginning in August 2007, only now does anyone stand up and declare Emperor Fed free from any clothing; if anything, the “money printing” meme is as alive today as it has ever been. See: dollar debasement.

There are, admittedly, reasonable questions about any assumed symmetries; meaning that expectations theories might not be directly translatable to the other side from inflation-fighting. Even if monetary policy using this framework to take credit for low inflation is indeed bunk, it might not necessarily discredit the same on the flipside trying to make inflation from none.

But it’s not off to a great start, is it?

And it only gets worse by examining the theoretical pieces, particularly how expectations theory tries to assemble (using the money illusion) a practical advice of real economy mechanics – how does labor, for example, actually translate these expectations into action? Rudd wonders:

In situations where inflation is relatively low on average, it also seems likely that there will be less of a concern on workers’ part about changes in the cost of living—that is, a smaller proportion of quits will reflect workers’ attempts to offset higher consumer prices by finding a better-paying job. But this is a story about outcomes, not expectations.

These questions are added to the growing volume of scholarship diminishing the previously uncritical view of QE and post-crisis inflation policies which depend exclusively on the same expectations manipulation agenda. Not only do Economists fail to produce any evidence for this, they don’t really know how it would work if it ever could!

Same is true of QE and QT. And now we can add tariff inflation to the graveyard. KC Jeff like Powell before last August worried expectations would sour and then produce price changes. Predictably, that never happened because that’s not how anything works.

Either monetary policy was perfectly spot on and effective from 1990 to 2007 for reasons lacking in evidence and explanation, not as much before that range nor at all after, or there must be another completely separate account which doesn’t require so many unbacked leaps as a matter of invented mathematical necessity.

Occam’s Razor needs to shave KC Jeff.

Jeremy Rudd’s summation of this missing support and verification is appropriate here: “And in some cases, the illusion of control is arguably more likely to cause problems than an actual lack of control.”

Well said and, dare I say, on the money.

Verify via CPI

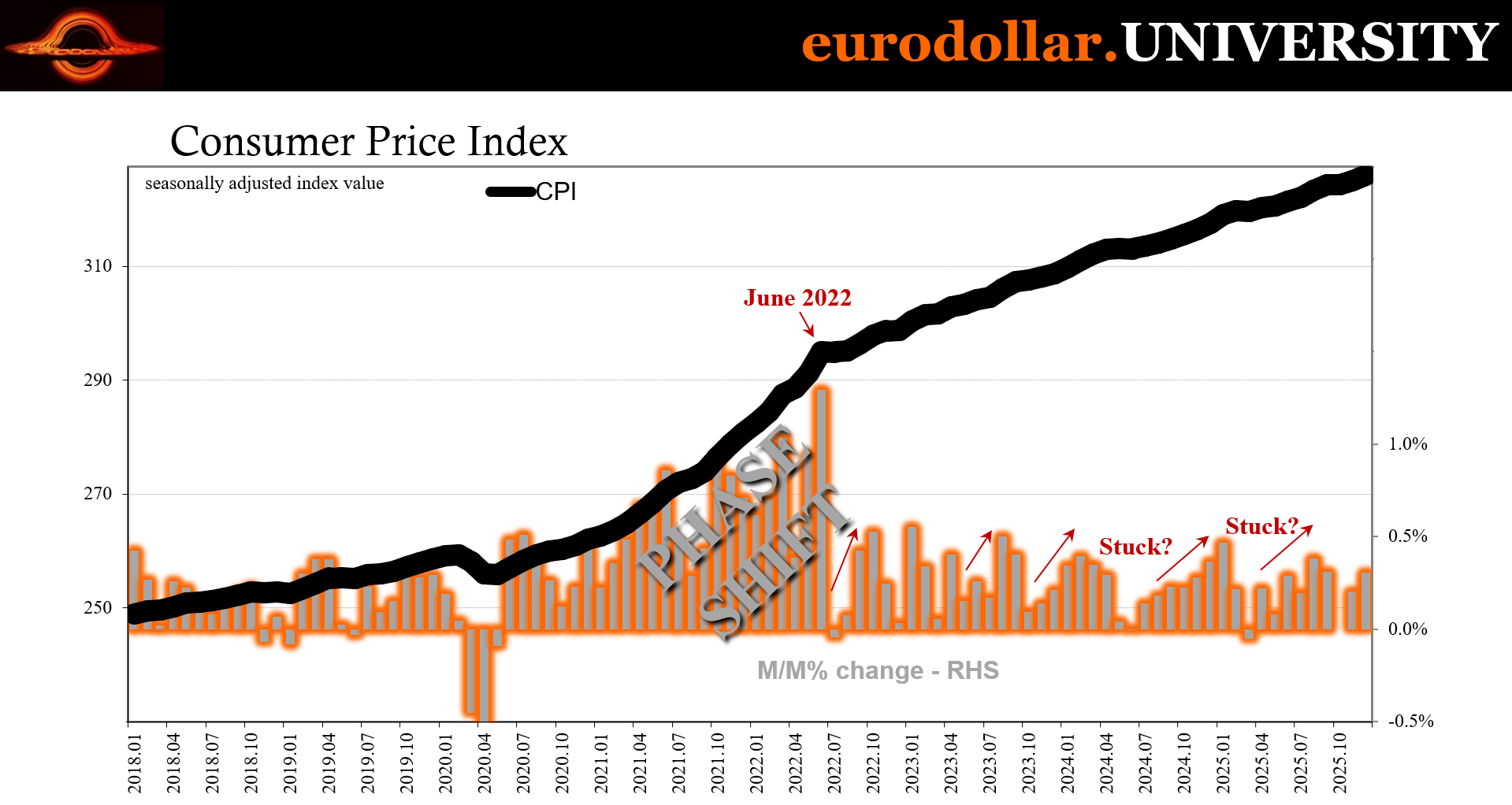

As I wrote at the top, December’s consumer prices rates were supposedly set to expose something off about November. Recall there was no CPI in October for the first time in its history, meaning the absence acted as an excuse for results that didn’t meet, ahem, expectations.

However, as I pointed out previously, it wasn’t as though the US alone had experienced the downshift in consumer price rates during that time frame. The UK even Canada and others, Germany, too, have seen the same thing at roughly the same time. Again, globally synchronized.

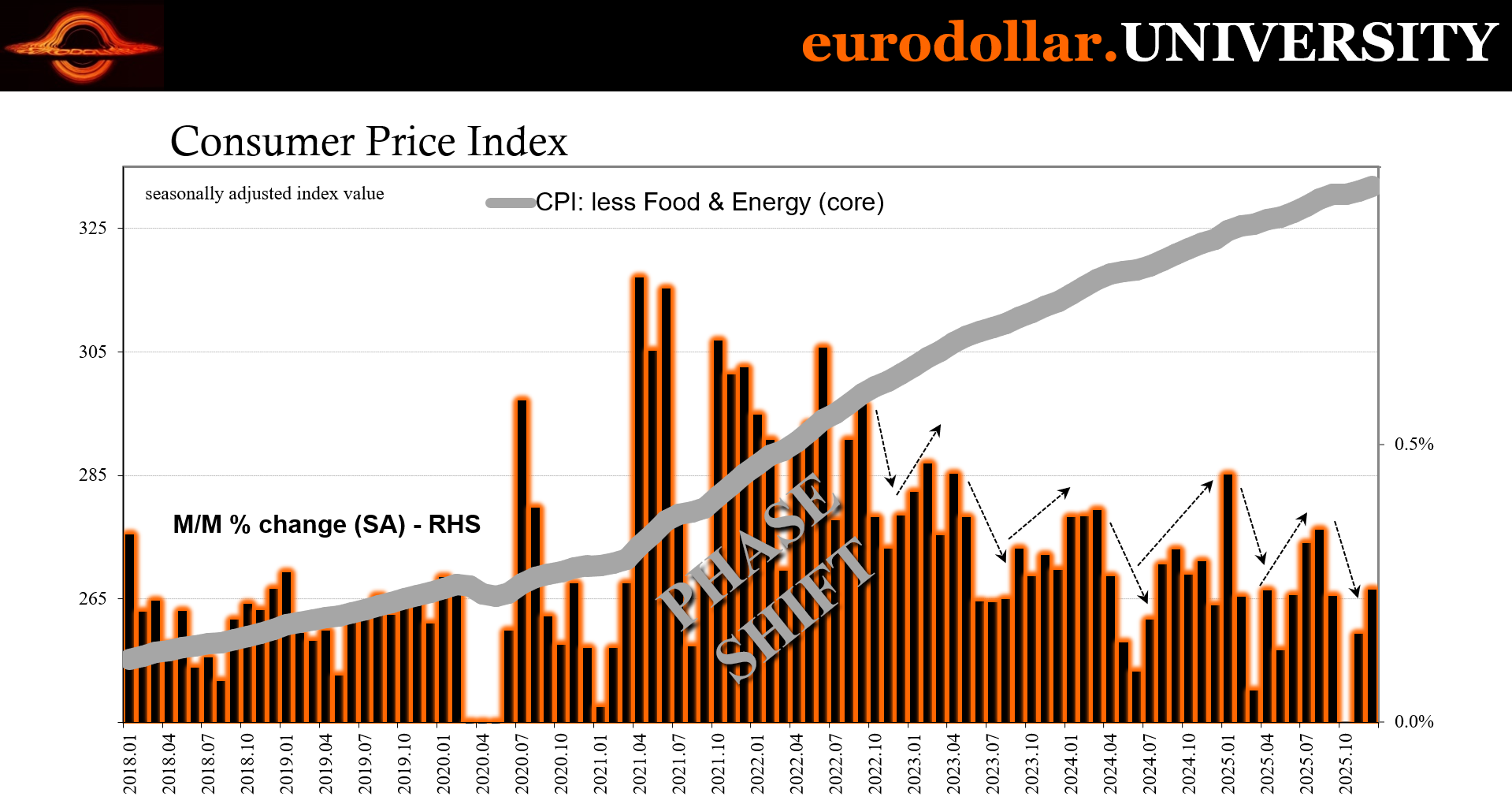

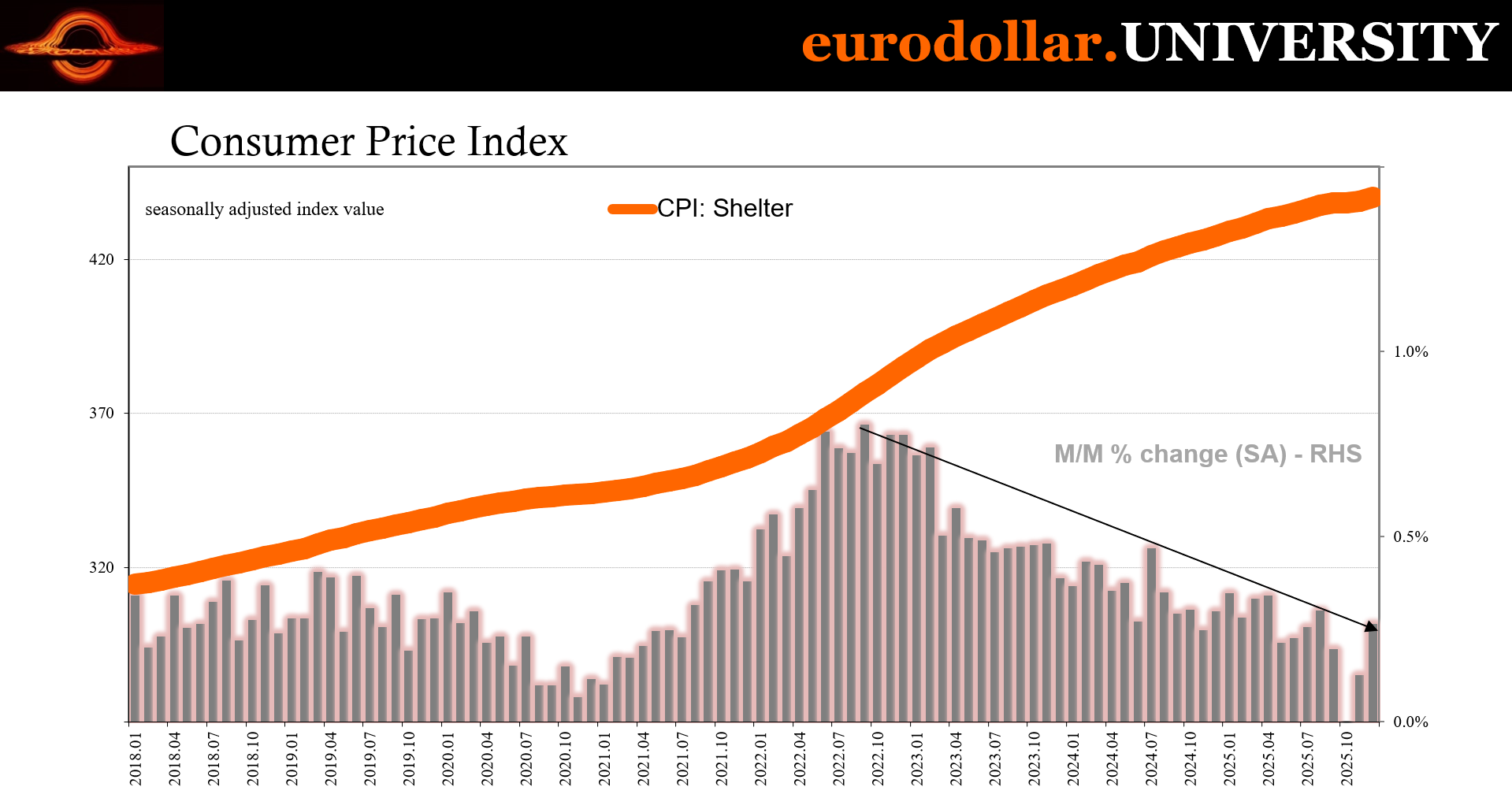

Yet, the latest consumer price estimates from the BLS underwhelmed in every category where it shouldn’t have, mainly the core. That key index came in at 0.24% m/m, up from 0.16% in that squirrelly November period (meaning something like 0.08% in October then November). Sure, it did rebound, though entirely on the strength of more fake shelter and even then not by much.

The BLS’s shelter index did what its complainants said it should, rising by 0.40% last month – most in any month since August. Yet, the rest of the CPI did much to offset that fakeness. Services prices (less rent) slowed materially rather than quickening so that excluding food, energy and shelter what’s left of the price bucket rose just 0.11%, down slightly from the 0.14% monthly rate so heavily criticized.

Take away shelter and the CPI would have been less than November in every way!

And we can go on and on over the details. Tariff inflation is dead because it never was. The idea was only kept alive by the superstitions of uniformed bureaucrats who remain in that state even when one of their own tries his best to inform some truth, injecting a few uncomfortable facts in the process, and setting the stage for years of thoroughly unrequited inflation fears whose only thin thread tied to that same questionable shelter set.

Maybe the quarterly results from Delta Airlines released earlier today should have the final word on this whole thing. The company missed guidance for 2026 even after previously indicating the airline business had itself turned a corner following last year’s “tariff uncertainty” – the astrological twin to tariff inflation.

The main reason for the hesitance is the economy. Delta said it can upgrade only some of its business, expecting that it will see some growth at least from premium travel. Everyone else, let’s just say they aren’t doing well enough to climb aboard a jet and go somewhere far enough.

At the same time, Bastian said demand from high-spending consumers continues to be strong. Delta has touted its premium products in the cabin and on the ground as it seeks to differentiate itself from budget carriers and appeal to well-heeled flyers.

“Effectively none of our growth in seats will be in the main cabin,” Bastian said. “They virtually all will be in the premium sector.”

They call it a K-shaped economy when it’s really a recession nobody wants to declare. Why? First, they said there were no job losses. Now that there are job losses, apparently there aren’t enough of them.

And still, all they want to talk about is inflation.

Economics is an irredeemable endeavor. The whole thing needs to be torched and burned to the ground. I keep telling you that central banks are the greatest source of uncertainty, not stability as was their promise, all because they haven’t a clue what they’re doing or why. The profession was detached by the monetary system and left all in it to wander around the intellectual universe blind and wholly uniformed.

Tariff inflation is merely the latest to prove it.