MUCH ADO ABOUT POWELL

EDU DDA Jan. 12, 2026

Summary: Jay Powell announced he is likely under criminal investigation from the DOJ about potentially having lied to Congress. This is supposed to be a HUGE deal, and in political circles it is being treated as such. Where anything matters, however, [insert shrug emoji here]. The Fed has been independent of the government, it has worked closely with political authorities, it has gone in other ways. None of it matters today just like it didn’t from a quarter-century ago and before. The only reason why this has come up is because “both” sides are starting to realize the truth - several of them.

It has set off a predictable “firestorm.” Not in the markets, of course, or anywhere it truly matters. In the financial media, the Federal Reserve’s “independence” is being threatened, and this is a huge deal. Or something.

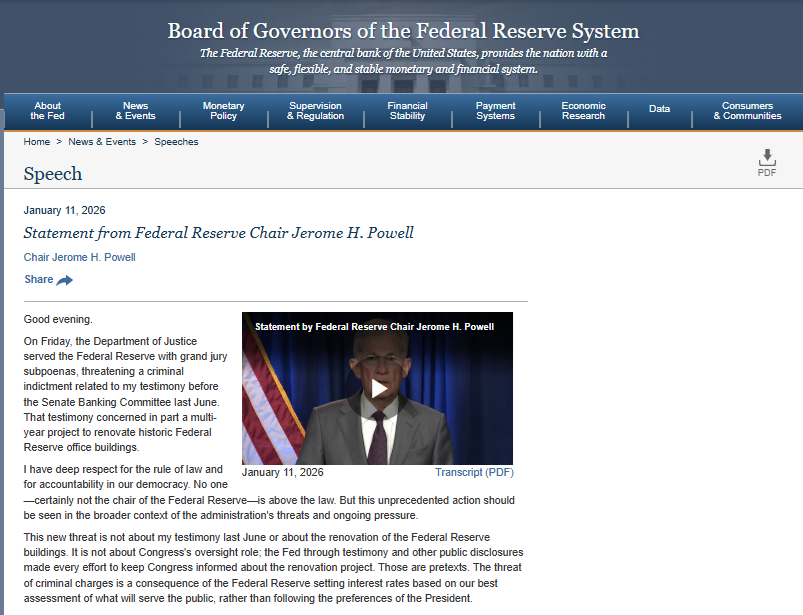

Federal Reserve Chair Powell issued a statement confirming he is the target of an investigation by the Department of Justice over testimony he gave to Congress wherein some of his statements may or may not have been factual. That’s for the courts to decide, apparently. Powell himself left no doubt as to what he thinks this is all about: interest rates.

ASK YOURSELF, WHO IS THIS REALLY FOR?

We went through this same panic last year and despite the production of nothing more than news articles touting sacred principals (that don’t exist) and their allegedly essential nature, the entire rest of the world collectively shrugged and moved on to vastly more important matters – like jobs and incomes.

There is already a sense among the rational and honest that the idea of interest rates doesn’t conform to the reality of interest rates. Everyone calls them “stimulus”, yet nothing is ever really stimulated. The Fed began its own pivot sixteen months ago to what end? Concerns about employment remain right at the top of consumers/voters’ minds anyway.

Those have only grown with each quarter-point tick downward in the fed funds range, some 175 bps in total.

Even Fed officials are increasingly worried about labor conditions, though careful to couch these views under cover of just being cautious. We are, according to Christine Lagarde, in a good place. In the US like Europe, no one outside the mainstream media and officialdom believes her.

That now includes the federal government, thus why the Trump administration has itself pivoted to various “stimulus” ideas, from tariff dividends as tax cuts to 50-year mortgages and maybe a GSE QE. No one is saying outright what is plainly going on here.

The idea of Fed independence has been overblown, both as it really is in terms of the relationship between the “central bank” and the government plus the notion it somehow makes a difference. We’re supposed to believe it’s huge when history shows everything else.

But why?

What is old is new again

Fed Chairs and their Presidents. The central bank is supposed to be independent, of course, but it’s not always been the case that either party sees it that way. More often than not, there is tremendous coordination among policy goals. In the depths of crisis during 2008, for example, the Federal Reserve came together with Congress in the last days of the Bush Administration to prove yet again none of them had any idea what they were doing.

On October 3, 2008, the Emergency Economic Stabilization Act was signed. Title I of the law delivered the Troubled Asset Relief Program, or TARP. Only ten days after being handed the authority to buy “troubled assets”, Treasury Secretary Henry Paulson in close consultation with Federal Reserve Chairman Ben Bernanke and others chose to “invest” a quarter trillion in banks instead.

It wasn’t working; it didn’t work. Rather than stabilize the economy, the US system would go on to shed an astounding 7.5 million payrolls over the next eighteen months. The worst economic contraction since the Great Depression propagated worldwide.

HMMMMM, THEY SEEM TO FIGHT WITH EACH OTHER WHEN THINGS AREN’T GOING WELL…

The seeds of the disaster were planted more than four decades earlier during a time when Fed officials weren’t so welcome at the White House, or wherever else the Chief Executive might’ve happened to be. In December 1965, President Lyndon Johnson recovering from gallbladder surgery at his Texas ranch was enraged at the central bank’s action. “You took advantage of me and I just want you to know that's a despicable thing to do,” the President told then- Fed Chairman William Martin.

Johnson had on his mind enlargement of the Vietnam War at the same time as fashioning his Great Society. These were hugely expansionary propositions. To Martin, they were hugely inflationary propositions.

LBJ knew that he needed a booming economy to help pay for everything. The Federal Reserve had voted to raise the discount rate to 4.5% from 4% despite weeks of negotiations and pleading. The President thought that he had gotten through to Martin, but the Federal Reserve Board, with Martin on board, felt differently.

“You've got me in a position where you can run a rapier into me and you've done it,” Johnson said when unleashing his famous temper on the mild-mannered central banker.

It wasn’t just LBJ’s agenda that the Federal Reserve had in mind, however. Since the late 1950’s, the Bretton Woods system had increasingly come apart. By November 1960, the formation of the London Gold Pool was a tacit admission that it no longer worked. The national parties to the agreement hoped that it would be a temporary fix, but contemporary accounts show quite conclusively that there wasn’t really much optimism nor much resolve to do anything about it.

The primary defect of Bretton Woods was that it never accounted for money demand globally. We today think of globalization as a relatively new phenomenon when in fact there have been repeated episodes throughout history. One big globalization push came in the 1910’s and 1920’s – only to be interrupted by the unequal distribution of gold/money once fear and hoarding following bank collapses in 1930 and onward obliterated the previous mechanisms for flow and redistribution.

The chief designers of Bretton Woods, John Maynard Keynes of the UK and Harry Dexter White of the US, didn’t allow for the possibility that globalization of earlier decades had been merely put on pause by the Great Depression. Increased global demand for trade required, unconditionally, a monetary system able to efficiently match money supply with money demand.

Bretton Woods could not, leading to what became known as Triffin’s Paradox. Robert Triffin proposed the two things were incompatible, yet simultaneously necessary. The US and UK together would have to supply sufficient currency, pounds and dollars, for use outside of their borders at the same time doing so would undermine the gold standing of each.

Following the Suez Crisis in 1956, which itself followed an enormous sterling crisis and devaluation in 1949, Bretton Woods would shift from a co-reserve system to a single reserve system based in dollar rather than pound denomination. Since trade and global economic expansion will always take first priority, that meant dollars would have to be overseas in abundance.

Where did they come from?

It seems like it should have been an easy answer. Grounded in traditional separate systems understanding, Economists and policymakers kept turning to the US current account. It never occurred to them that monetary innovations in the face of overwhelming need might render traditional notions, even to the point of monetary accounting itself, obsolete.

Money would come from bank ledgers, not some printing press.

Benign neglect

Several times throughout the decade of sixties, the Fed would act on their view of a rising current account deficit paired with the steady and sharp loss of gold reserves. Triffin’s very dilemma. The booming global economy needed money to stay booming, but it was playing havoc with central bankers. In 1964, the Federal Reserve Board noted the tension:

There was extensive discussion...about the proper course of monetary policy in the light of the serious and persistent balance of payments deficit and the urgent need for additional measures to deal with it. At the same time it was recognized that the domestic economy was not expanding at a rate sufficient to bring about full employment soon and that a more rapid rate of growth was to be desired.

The rate hike in December 1965 was only partially about the worries over inflationary consequences of the Johnson Administration’s activities. The US could ill-afford to lose more gold without further jeopardizing the dollar’s standing, many of them believed, and therefore the global framework that at the time was barely holding together. Plagued by so many concerns in so many different directions, the central bank’s actions were haphazard – one reason why LBJ wasn’t expecting opposition.

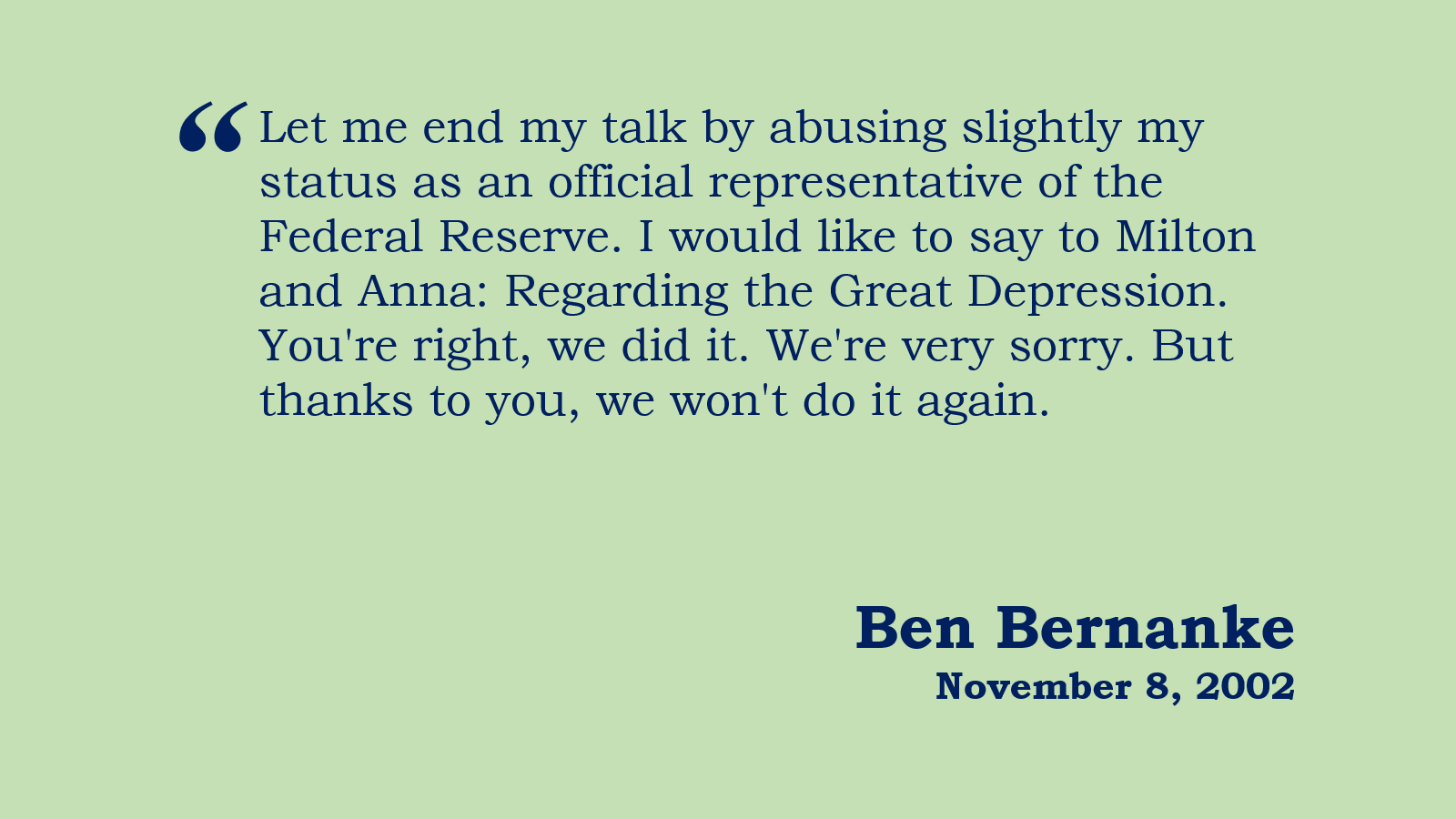

In 1971, Economist Paul Samuelson would call this dollar policy “benign neglect.” In a sense, the government would do very little about either the dollar or the budget and just hope for the best (never realizing the eurodollar provided it). The Federal Reserve was a full party to it, meaning ignorance, William Martin in 1970 finishing off his very long tenure in office saying, “I’ve failed.”

In August 1971, President Nixon officially closed the Bretton Woods era by defaulting on the country’s gold obligations – the dollar would no longer be convertible by anyone into gold or anything else. By then, only other governments even wanted bullion. The commercial world had long before moved on, meaning all the various agencies and institutions of the US government and among others overseas were conspiring and scheming to take care of a system that no longer effectively existed.

Benign neglect? Irrelevant ignorance. To this day!

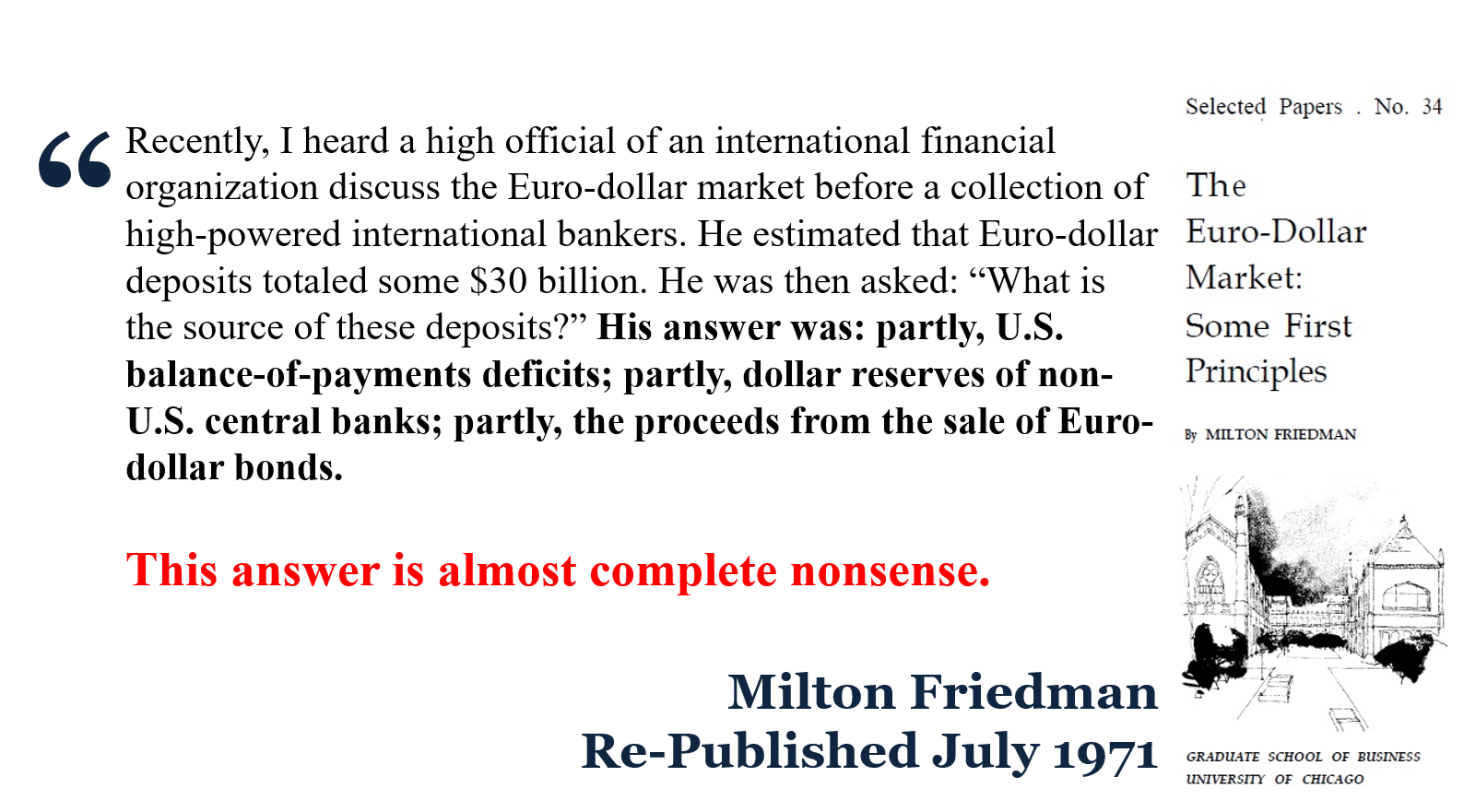

The following month, September 1971, Congress’ Joint Economic Committee held hearings on the proposed economic plans. On the second day of testimony, the Committee pitted Samuelson against Milton Friedman. The latter testified in his prepared remarks:

If I may summarize to you briefly what I have said in the rest of this particular section, it is that the President's action gave a formal signal that the Bretton Woods system is dead, that it will no longer be revived. This opens the opportunity for a more meaningful development in world monetary relations.

In Friedman’s view, a new international monetary order had to be created but it would not be imposed again from the top-down. “I think international systems grow out of real economic forces and cannot be invented, that basic economic forces are stronger than the Central Bankers or the international monetary officials.” Tell that to Bloomberg and it’s Fed-obsessed headlines.

By de-linking from gold, the balance-of-payments problem for the dollar would completely disappear. No more Triffin’s Paradox. Exactly how the world would manage money supply versus demand, Friedman wouldn’t venture a guess. He didn’t need to because the answer was already very well-entrenched by then, nearly two decades of eurodollar practice having supplanted the old order from back in the fifties.

Government bureaucrats kept fighting with each other, then working together, only to fight with each other some more. Meanwhile, money and commerce barely noticed their “power” plays.

If money is global, then national central banks make no sense

For Friedman, the argument was easy in the shape of globalization as we know it. The fixed gold price, or what he called the “fetish of fixed exchanges”, was inhibiting the free flow of goods and capital. It produced massive distortions, leading to “a waste of capital in building plants simply to scale tariff walls.”

Samuelson agreed that the gold window should have been closed but then worried about the direction of American labor.

In a moment, I shall comment upon various policies of benign neglect which are urged upon you gentlemen. But one of the greatest costs of that policy in the past and one of the costs of that policy in the future if you accede to it will be a perpetuation of the employment problems associated with international trade. And you will feed the fire of protectionism.

Indeed, President Nixon in allowing the dollar to float also imposed an enormous 10% import surcharge, one that has been completely forgotten because, like Bush’s helicopter in early 2008 or its later TARP fiasco, none of it worked. Authorities can work together, they can work independently, none of it matters because there isn’t one of them who understands basic monetary economics.

Even Friedman struggled mightily with the eurodollar.

The President’s (Nixon) intent was to correct for what Samuelson argued in front of Congress – that currency values did not accurately reflect parities. Therefore, simply revaluing the dollar in gold would not, in Samuelson’s mind, change the policy of benign neglect. The world needed a clear monetary directive, else protectionism (or populism) by default.

I think you do not change the Las Vegas odds by this token change here, that 30 years from now gold will be out of the monetary system by 1 percent probability. That has to be fought on its merits. And I will remind you of what Mr. Roosa used to remind you of in testimony when he was in office years ago, that de facto, a large part of the world's reserves today are official gold. Those will have to be replaced.

Robert Roosa also testified to the Joint Economic Committee in September of 1971. He had been Treasury Undersecretary for Monetary Affairs during the Kennedy Administration, using that position to advocate for a global dollar standard.

What he had to say to the Committee was a bit different from either Friedman or Samuelson; and not as a matter of politics or even economic debate. He agreed that the US should abandon gold at $35, but that it should not abandon gold. Gold reserves indeed would have to be replaced, but with what? His view was more toward the functionalities of this brave new emerging monetary order.

There had to be some flexible medium and gold wasn’t it.

Another contribution to the solution of the long-term international monetary problem would be the following: The United States is being urged by other countries to pay for its deficits in reserve assets-gold, SDR's and foreign currencies-instead of paying in dollars. This is a request that is not completely without reason. On the other hand, it is quite impossible for us to pay for our short-term capital movements in anything but dollars, because these run into the billions, and tens of billions. Very often, they have nothing to do with the United States. There may be movements out of the Eurodollar market into national currencies, say, out of the Eurodollar market into marks. We cannot be held responsible for that and come up with SDR payments or drawings on the IMF. That has to be settled in dollars.

It was a tacit recognition of the world behind the last decades of Bretton Woods. By being forced to substitute reserve assets for dollars on international markets, the US position was, under benign neglect, to simply do as little as possible, forcing the growing demand for international money to look elsewhere for it.

Misunderstanding was at the heart of every government action.

Roosa was proven correct, however. The eurodollar became the world’s reserve currency without so much as a central bank or government approving of the arrangement. Friedman was also correct about one key factor, that, again, “I think international systems grow out of real economic forces and cannot be invented, that basic economic forces are stronger than the Central Bankers or the international monetary officials.”

So it was in 1971, so it remains to this very day. We’re supposed to care about the Fed when the monetary world stopped doing so before both my parents were born.

Central banks are merely along for the ride. They pretend as though they can reach economic targets, that Congress can mandate Jay Powell employ all his wiles to maintain maximum employment and stable prices (which are both supposed to then supply the Fed’s third overlooked mandate, for moderate and stable interest rates!)

But the Fed abandoned maximum employment years ago after realizing they couldn’t figure out what it was in the 2010s – which, you might remember, importantly followed that monetary disaster in 2008. These things are all related!

So, too, the irrelevance of the Fed in anything approaching a real context. For workers, what the FOMC decides is immaterial. For consumer prices, the fed funds rate holds no meaning. In markets, the real ones apart from the NASDAQ casino, Jay Powell who?

But for politics, the Fed is the economic universe’s center. It is the agency by which to pretend government has the power and ability to shape the most important forces in the voting public’s lives. Apart from children and families, that means livelihoods.

See, that’s what this current political dustup is really about. The economy sucks and everyone knows it these days, both the President and the Fed Chair have finally come around to the truth. What they can’t figure out is what to do about anything. Whether they work together or not, whether they tear the institution apart, it’s all just noise.

Ask yourself, who is all this “Fed independence” really for?

Far better to realize it and move on to what really matters: Flat Beveridge and the potential for Stage 2 of cockroach garbage.