A SANE RATIO

EDU DDA Jan. 15, 2026

Summary: Silver is no longer parabolic, the price is now going straight upward. The question many are asking is why. Is this reflation, inflation, maybe the first rumble of hyperinflation? We have historical examples to draw on not to mention the behavior of other influences. In one of those, copper is behaving a lot like silver, if not to that extreme. So, the question is whether copper and silver together outduel gold taking the other side. The answer, it turns out, comes down to what the Chinese believe. And do.

WE’VE SEEN THIS BEFORE…

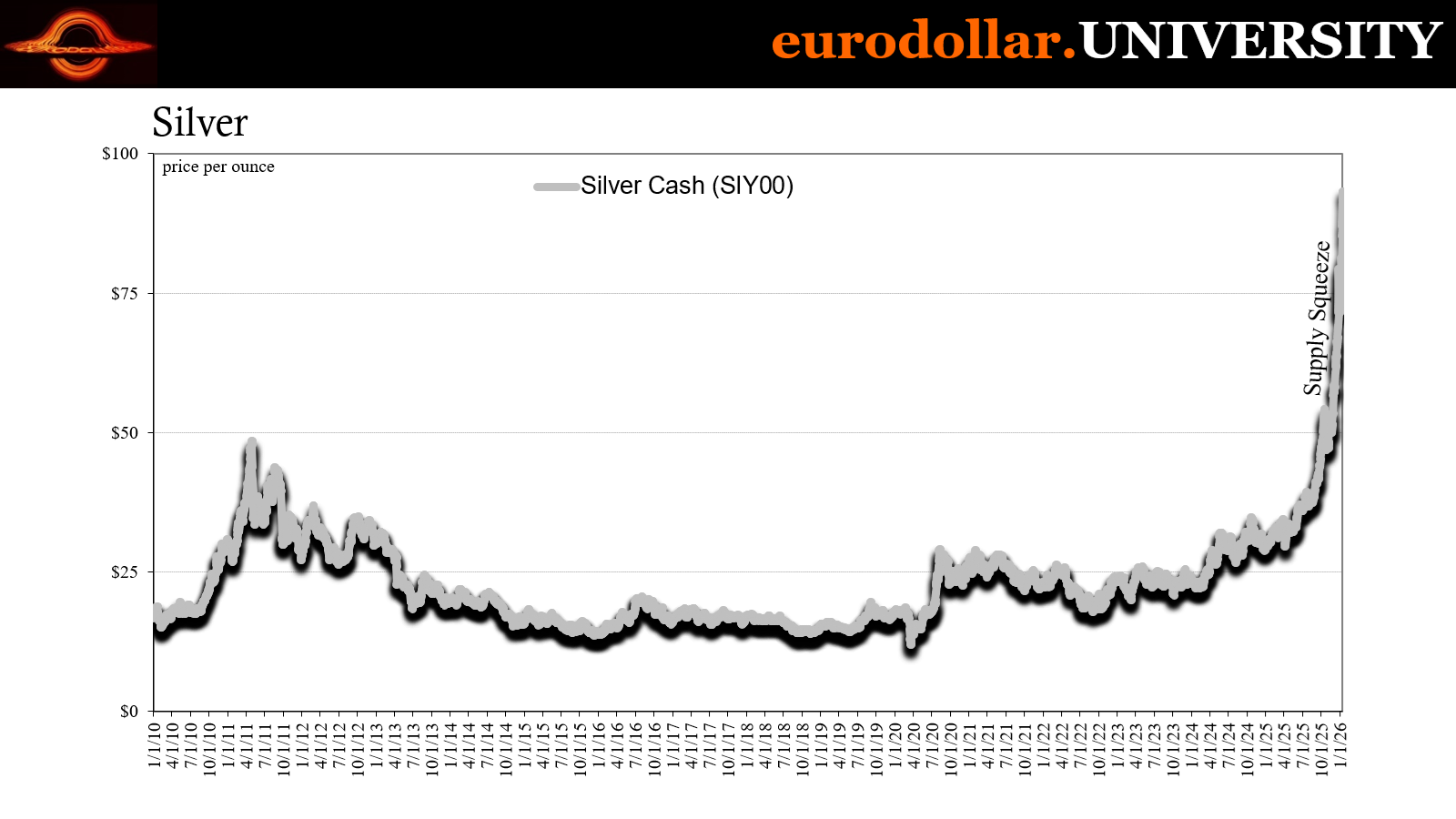

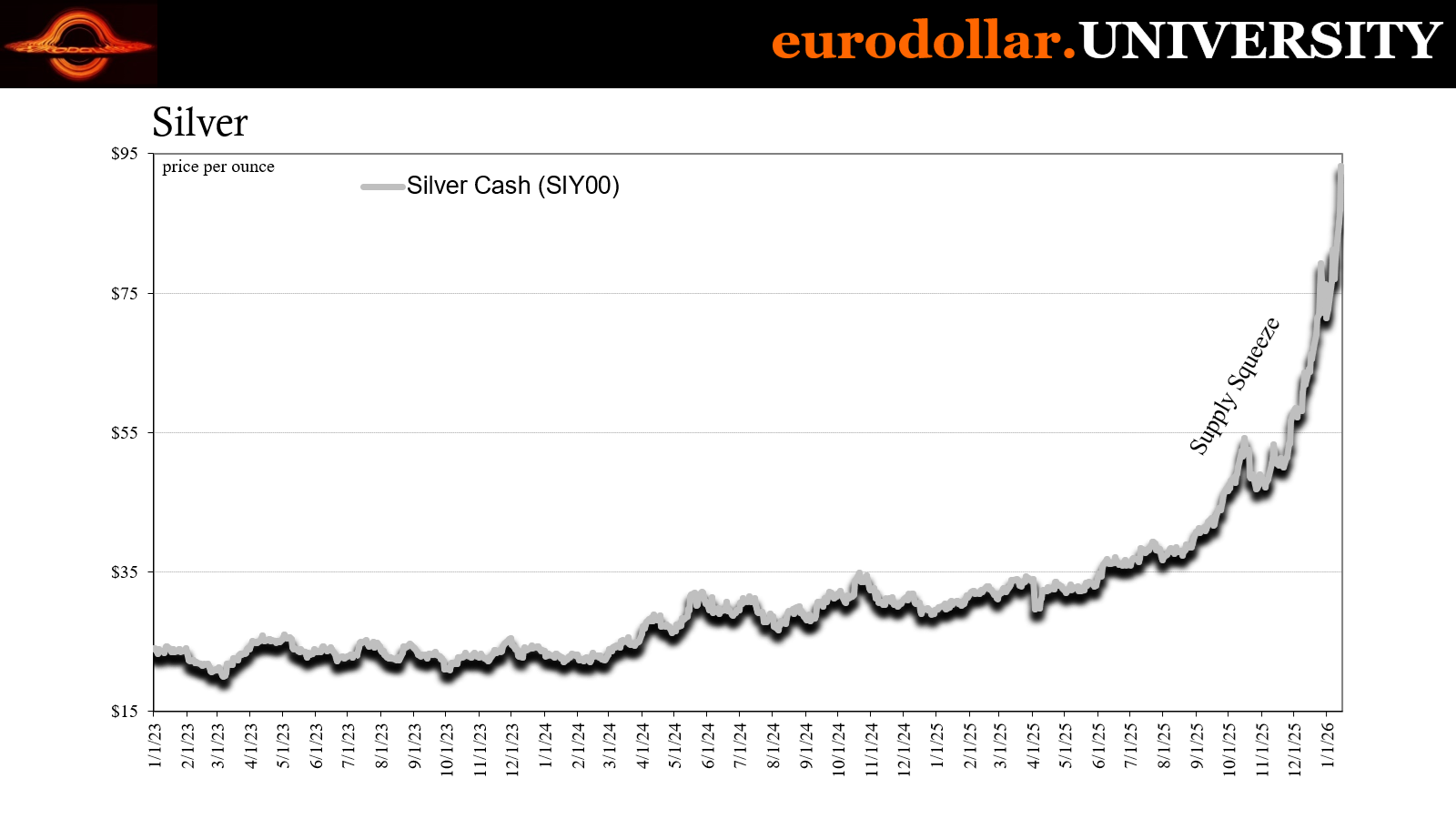

There is no universe in which a commodity price goes straight up – not even parabolic, literally straight up – and it ends well for that commodity and any interpretation of its rise that suggests it is real and permanent. Silver’s epic squeeze continues to run, putting the metal yesterday above $93 for the first time and raising the rate of return (in dollars) to 222% since the final days of 2024 when the trend got going.

As a result, despite gold’s ongoing binge bringing it to an all-time high of its own, the gold-to-silver ratio has completely collapsed, falling under 50 for the first time since early 2012. This has unleashed some debate and discussion centered on whether silver prices are finally catching up to “reality.” In other words, what should the ratio be?

To answer that question means digging into details that have a lot more on the line than precious metals: economic and monetary fundamentals.

Fortunately, we can draw on a number of historical examples and make informed comparisons. Silver has suffered artificial interference repeatedly throughout its history, and in both direction. The government was the primary reason in one that we will examine, though in the opposite way as what I believe is happening today.

The other we’ll look at was indeed “evil” speculators.

Silver is not an isolated instance or instrument. That’s why we have the gold-to-silver ratio in the first place. That also means others, including copper even though copper appears to be infected the same as silver, if not to the same degree.

So, that sets up the experiment: copper and silver on the one side with gold on the other. Which group is pricing reality, which the fleeting influences artificiality?

China’s latest on its banking sector definitely aids in determining which is which, not least because the Chinese are heavy buyers of at least two of those. But only one of those by choice.

Sub-50

The gold-to-silver ratio was 60 not all that long ago. In fact, it broke under that level for the first time in forever just over two weeks ago. Yes, we tend to overstate the importance of round numbers, but the truth is the ratio went from 60 to 50 in the blink of an eye.

And it’s not to difficult to see what for; we’ll get to why in a second. Silver went from just above $70 to a record $93 during that same short space. It was only back on Thanksgiving when the “other” metal was still around $50 and the ratio at 80.

This is insanity, neither a healthy nor sustainable advance. Speculation otherwise is unsound.

Much of this has been provoked by tariffs and the response to threats over them. Silver supplies have been critically disrupted, what was already a tight market by any historical standards pushed past its limits even before the rush of panic-buying hit the marketplace a few months ago. This isn’t just an obvious, standard supply squeeze, it has become epic and that’s not a good thing.

When I write that the price of silver is now straight up, I’m not exaggerating.

The questions becomes, could it possibly be the inflationary or hyperinflationary signal that certainly many silver enthusiasts are now claiming it is? After all, the last time anything like this happened was…2011. However, you don’t hear much about that supply shock because it is inconvenient to the idea (and we’ll skip it here).

Instead, everyone loves to point to 1979 and 1980. And even then, everyone also forgets or just ignores how much artificiality was in silver during much of that period, too. The Hunt Brothers’ cornering were yesteryear’s tariff distortion.

Misunderstood silver

The Hunt’s silver squeeze looked a ton like the one under way right now. It finally failed on March 27, 1980, when the COMEX introduced Silver Rule 7 which knee-capped the speculators who came riding the brothers’ coattails by restricting margin use. Silver before then had also been straight up and once the COMEX moved it wasn’t pretty.

I’ve always wondered why either of the Hunts didn’t anticipate such an action. Did they buy their own myth? It’s human nature to fall in love with whatever you’ve got that seems to be working that well. Care and caution is always required, more so in that case than the opposite. Confirmation bias is a killer (as well all know).

But how to “properly” analyze silver? If we start with gold, what’s the “right” ratio between the two?

Let’s look at a counter example.

COFFIN LITERALLY WROTE THE BOOK ON BANK EXAMINATION IN THE LATTER 19TH CENTURY

George Mathewes Coffin was in 1908 America’s foremost expert on banking and money. He had started in the office of Comptroller at the Treasury Department in 1886 as nothing more than a teller. In only a few months, he was promoted to chief of the issue division and in 1888 had been made head of the division of reports. That meant he was the nation’s chief supervisor of all bank examiners’ inspections (national banks).

What constrained any bank at that time was actual money, even as they evolved into a ledger money format (deposit banking). National banks since the Greenback era of the Civil War, the national emergency that brought national banks into existence, had been authorized to back their assets with government bonds rather than specifically specie. Even then, however, cash was the final settlement.

But the period between the Civil War and the Panic of 1893 had been one of experimentation over money. Silver coins had been a major staple of the American economy from the days before there was a United States. Following that War, they had largely disappeared from circulation. Left in their place was a gold standard alone almost by default, at least outwardly.

This was the “crime” to which William Jennings Bryan had ridden to the first two (1896, 1900) of his three (he was also nominated in 1908) Democratic Presidential nominations. Representing the South and Midwest largely farming economies, these silver populists accused bankers of misappropriating a gold standard to the direct harm of indebted farmers. This “cross of gold” was, they claimed, responsible for the devastating price deflation ravaging their communities.

Not so, many bankers responded. Among the more forceful voices in opposition to Bryan was George Coffin. In 1895, he wrote and published a powerful rejoinder made so by his well-earned reputation. Titled Silver and Common Sense, he completely dismantled the main points of the silver argument just before the all-important 1896 election.

From his position within the Comptrollers office, Coffin had unparalleled access to monetary and banking checks. Major money statistics were practically nil at the time, so what information Coffin could compile was definitive.

He had shown that between 1851 and 1873, silver production had been $1.19 billion. From 1874 to 1891, it nearly doubled to $2.03 billion, while an additional $601 million was added in the years 1892, 1893, and 1984.

Even with that huge increase in production, silver coins in actual circulation plummeted. Coffin wrote, “…that out of the large amount of 423,000,000 silver dollars coined since 1878 only about 53,000,000 of these pieces are now in actual circulation amongst the people, the balance all being held by the Government chiefly on deposit for the people who hold paper certificates for the silver dollars.”

Before the sharp increase in silver production, gold was mined far more heavily in relation. Thus, a silver dollar (officially determined to be coined in a ratio of 16 to 1 silver to gold content) that had been given a market price of 101 cents in 1849 (gold rush) had risen to 105 cents by 1859. It was still at a slight premium, 100.46 cents, in 1873 but averaged just 81 cents (according to Coffin’s numbers) from 1874 to 1891 as silver production doubled, and only 53 cents in the three years following.

As the Government will deliver silver dollars free of freight charges anywhere in the United States, if the people want them and prefer them to other money why do they not take them?

What we call Gresham’s Law today was responsible for all the silver ending up in bullion at the Treasury Department. Coinage laws forced the government to buy up silver regardless of actual demand at 16 to 1, so Americans simply disposed of their silver upon the feds and never took the coins back.

Agricultural price deflation was misattributed to widespread preference for gold and the apparent scarcity of silver in circulation. What the populists claimed was monetary deflation was instead the productive advance of industrialization.

Again, it is stated by the advocates of free silver coinage that prices of products are low because money is scarce, but this is not true, for the amount of money in circulation per capita in the United States has almost steadily increased from $18 per capita in 1873 to over $24 per capita in 1894, as official statistics conclusively show, and yet the prices of products have steadily decreased during the same period; so this contention cannot be true, and, as already states, the decline in prices has been almost entirely due to the action of the law of supply and demand affected by labor-saving devices and not the volume of money.

George Coffin wrote that the primary use of silver coins for low denomination commerce was itself an evolution, taking over for other base metals first iron then copper then silver. That forward progress in money had been a primary step to the industrial revolution and what that meant was far more good than bad.

As an illustration, it has been computed that iron nails are now so cheap that if a carpenter drops every other nail while he is working, the labor cost of his time in picking them up would exceed the cost of nails dropped.

From too much to not enough

In 2025 now 2026, silver is at the opposite end of the spectrum. To begin with, real economy applications that didn’t exist a hundred years ago are now prevalent. Silver has become an industrial commodity far more than a precious metal.

And yet, despite a proliferation of uses, the ratio of gold to silver remained heavily in gold’s favor throughout the last several decades though, as gold detractors like to always point out, you can’t eat gold. Silver has real economy demand, gold has none. Yet, gold was the one outperforming. No one as yet has found a way to turn silver edible, either, but industrious people have indeed put the metal into a lot of modern society.

So, if we are on the flipside of the latter nineteenth century, where there might today be more demand and not enough supply, shouldn’t we expect silver to outdistance gold and do so by quite a lot?

If all that was still true, how it would take place wouldn’t be a straight line upward. The latter is 1980 and Hunt Brothers, not widespread spreading AI data centers. Plus, we also have copper to consider.

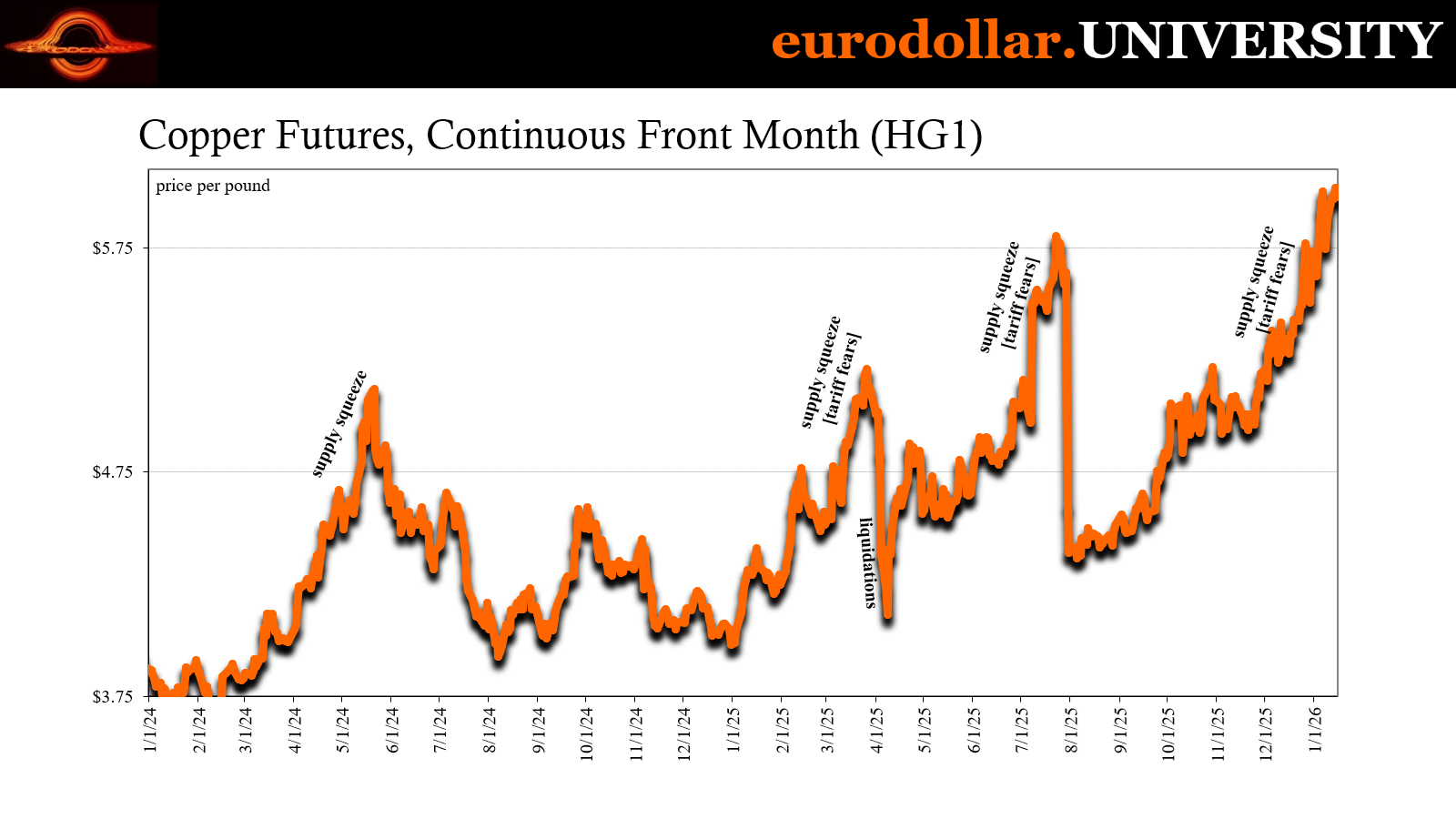

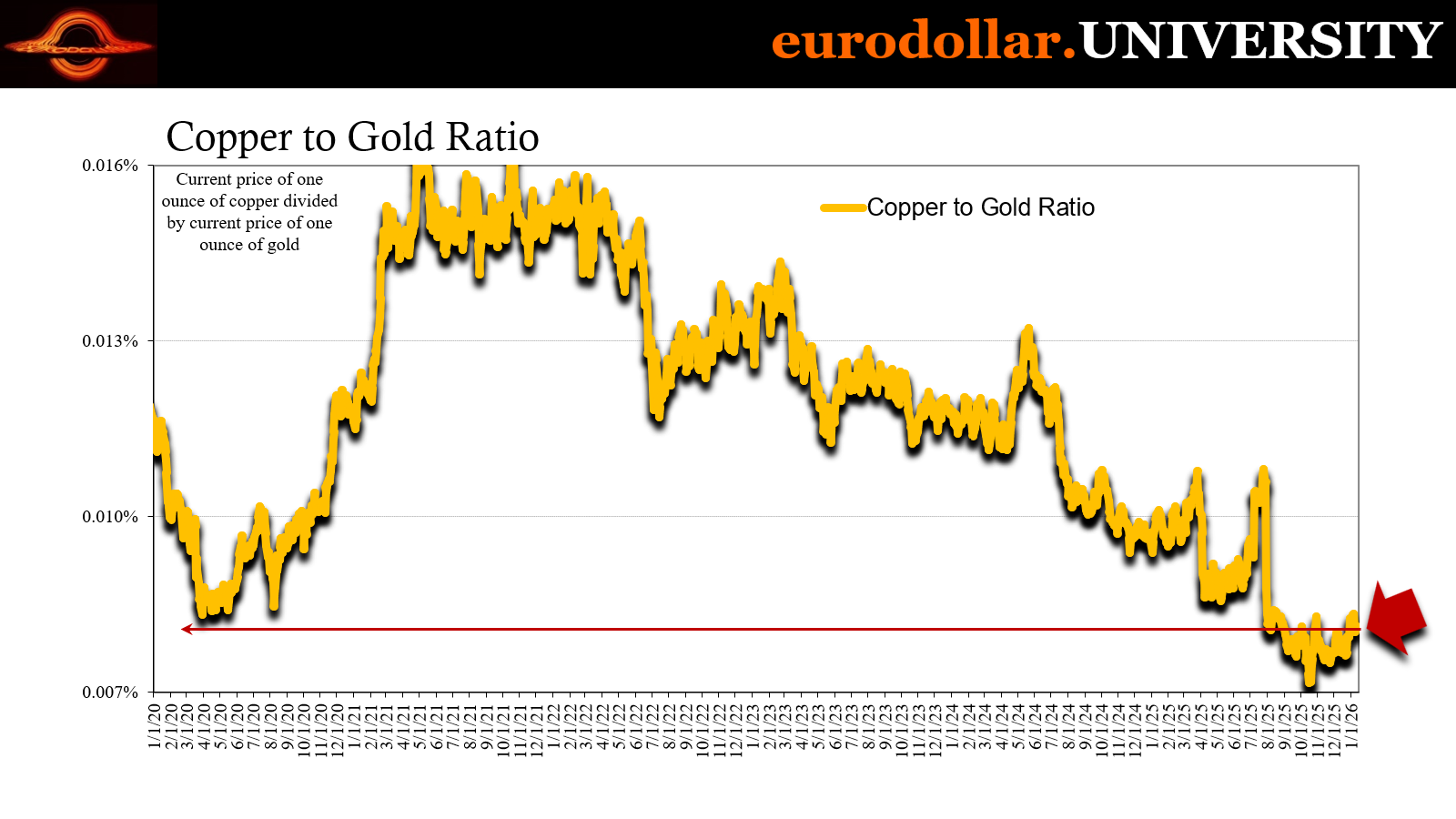

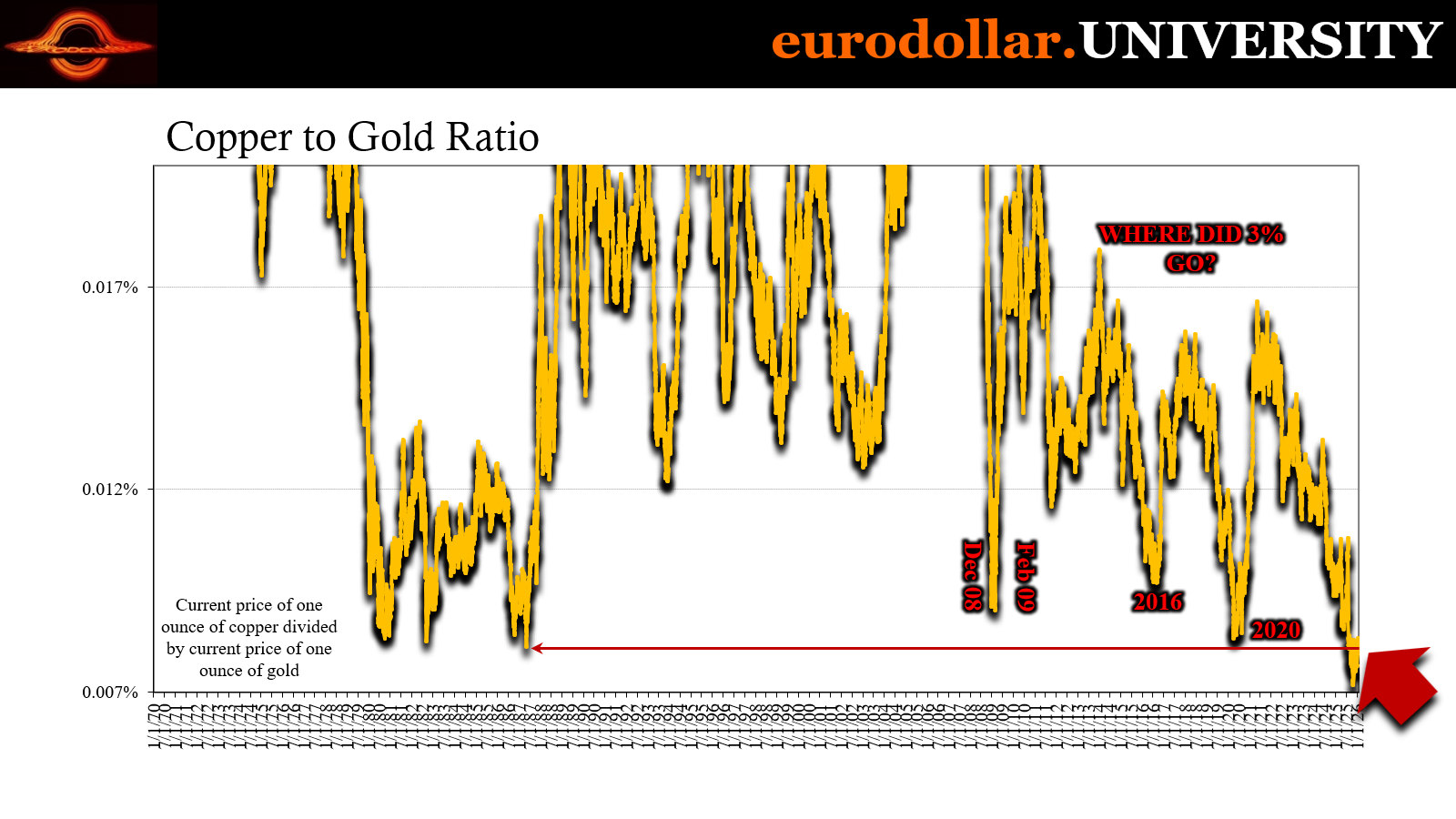

Copper prices have also surged, hitting their own record highs not all that long ago. Dr. Copper’s top has been noticeably more restrained, however, even as the use cases for this metal are far stronger and more numerous than silver’s. If the latter is booming for more electronics in our future, the former really should be booming a lot more first.

Instead, the same story shows up here, too. Copper’s price is tainted by tariffs in the same way, if inverse, from how silver had been via government activity way back when. In other words, these are all symptoms – and pretty clear ones – of artificiality. These are not what might be considered natural or organic results.

We can see it also in copper’s relation to gold. Copper-to-gold is barely clinging to 0.008%, not far off its record low. As we know only too well, low CtG is a solid deflationary signal, an opposite of an AI-fueled boom rippling in inflationary fashion around the global economy. That low signal is instead definitive about silver and copper, both being artificially squeezed by non-economic forces.

The modern version of Coffin’s critique, the Hunts reborn and reformed.

Thus, to make the case for either silver or copper it would necessarily require defeating the signal from gold. Perhaps it is gold that is “wrong” here and both the other metals are the “true” price action for a world going right and perceived to be heading that way quicker than anyone, even the most optimistic, appears to expect.

China banks on gold

The idea of 3% growth used to be so uncontroversial it was practically religion. The postwar average of real GDP was 3.2% in the US, including recessions, so to make 3% a baseline would be so perfectly natural.

In 2017, however, the Trump administration budget’s use of it, by contrast, produced an enormous backlash. Much of that was simply due to the political climate of 2017 where the mere mention of his name invoked immediate emotion, but we must remember that the climate of 2017was itself almost entirely a product of that same debate.

Remarking to CNBC on the budget proposal, former Federal Reserve Vice Chairman Alice Rivlin stated the issue perhaps as well as might be expected. With respect to these expectations for economic vitality, she said very simply, “We haven’t seen 3 percent growth for a long time.”

Why doesn’t this resonate the way it should? Shouldn’t the whole world be wondering where that additional percent of growth disappeared to?

THE MARKETS ACTUALLY AGREED WITH RIVLIN, BUT NOT WHY

Instead, what happened is central bankers successfully convinced everyone 3% was no longer attainable and did so using the most dastardly “logic” – since their policies failed to restore what used to be taken for granted, officials explain that 3% is simply no longer possible rather than having anyone consider those policies failed.

We were conditioned to accept 2% and less rather than realize QE didn’t work.

Markets, on the contrary, were not. This is why gold outperformed relative to silver as copper underperformed it. Not to mention interest rates and financial signals up and down the spectrum, all pointing to the massive deficiency of 2%. As Einstein supposed said, compound interest is the most powerful force in the universe and it applies to economic growth just as much.

Shave only a percent off the rate but do so for a long time and watch the world eventually burn.

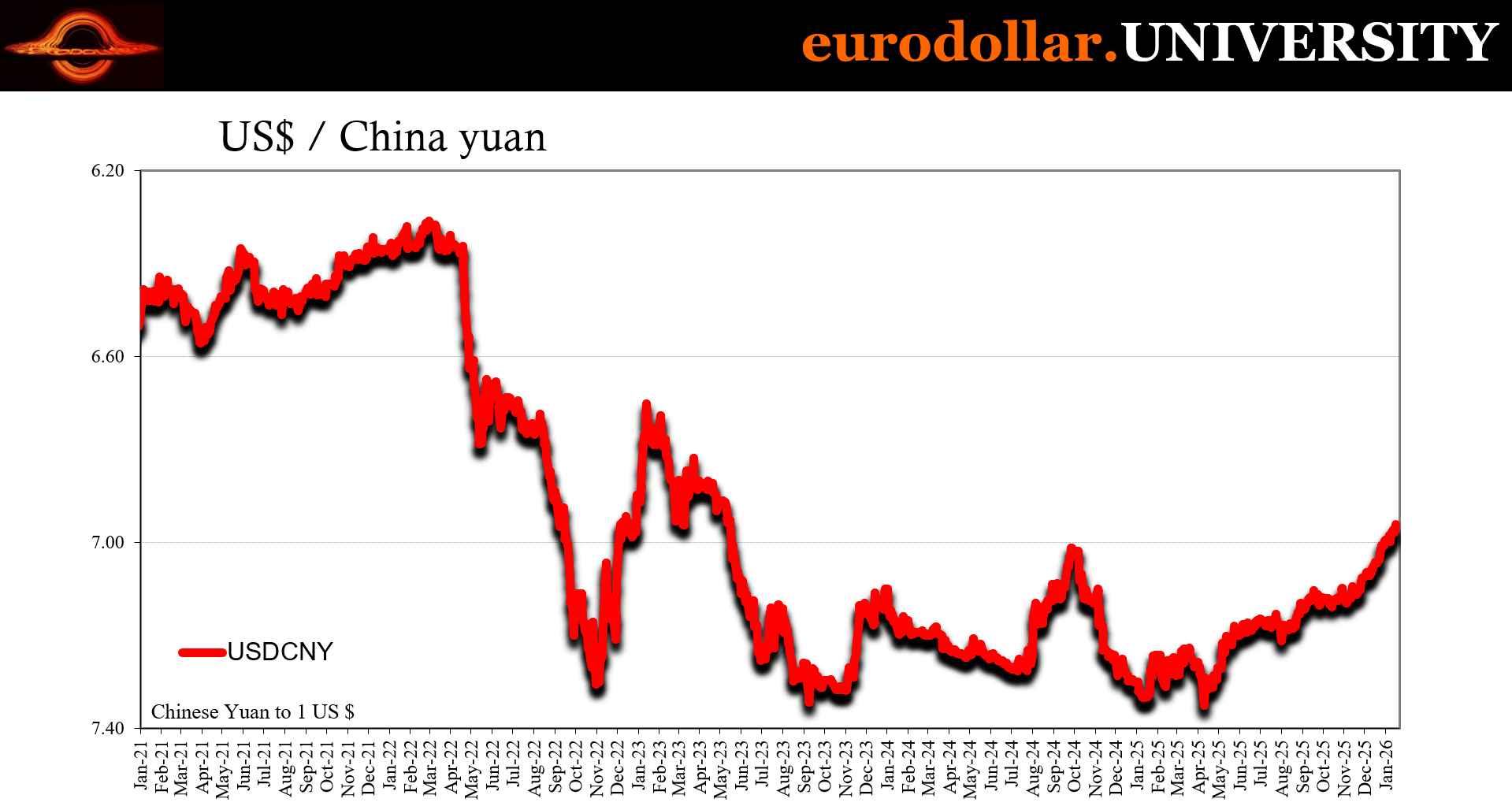

Since we are hip deep in silver and copper discussion, much of it falls on China. The Chinese have achieved a precarious equilibrium of sorts these days, if it can be called that. On the one hand, they’ve been able to dump a biblical amount of merchandise on the rest of the world outside the United States to the tune of a $1.2 trillion trade surplus.

This is the primary reason for CNY’s ongoing strength; the mountain of eurodollars that surplus brings is so enormous mechanically China is overflowing with them. The opposite of the dollar shortage we normally find around Shanghai and Hong Kong markets.

But what are the Chinese doing with all that ledger money?

They’re buying gold. Loods of it.

Think about what happens to everything in China if - maybe when - that trade surplus shrinks again. Should other countries follow Mexico who is already following Trump and put up trade barriers, exports won’t support China’s trade balance. That would undermine what little is left supporting the troubled internal economy.

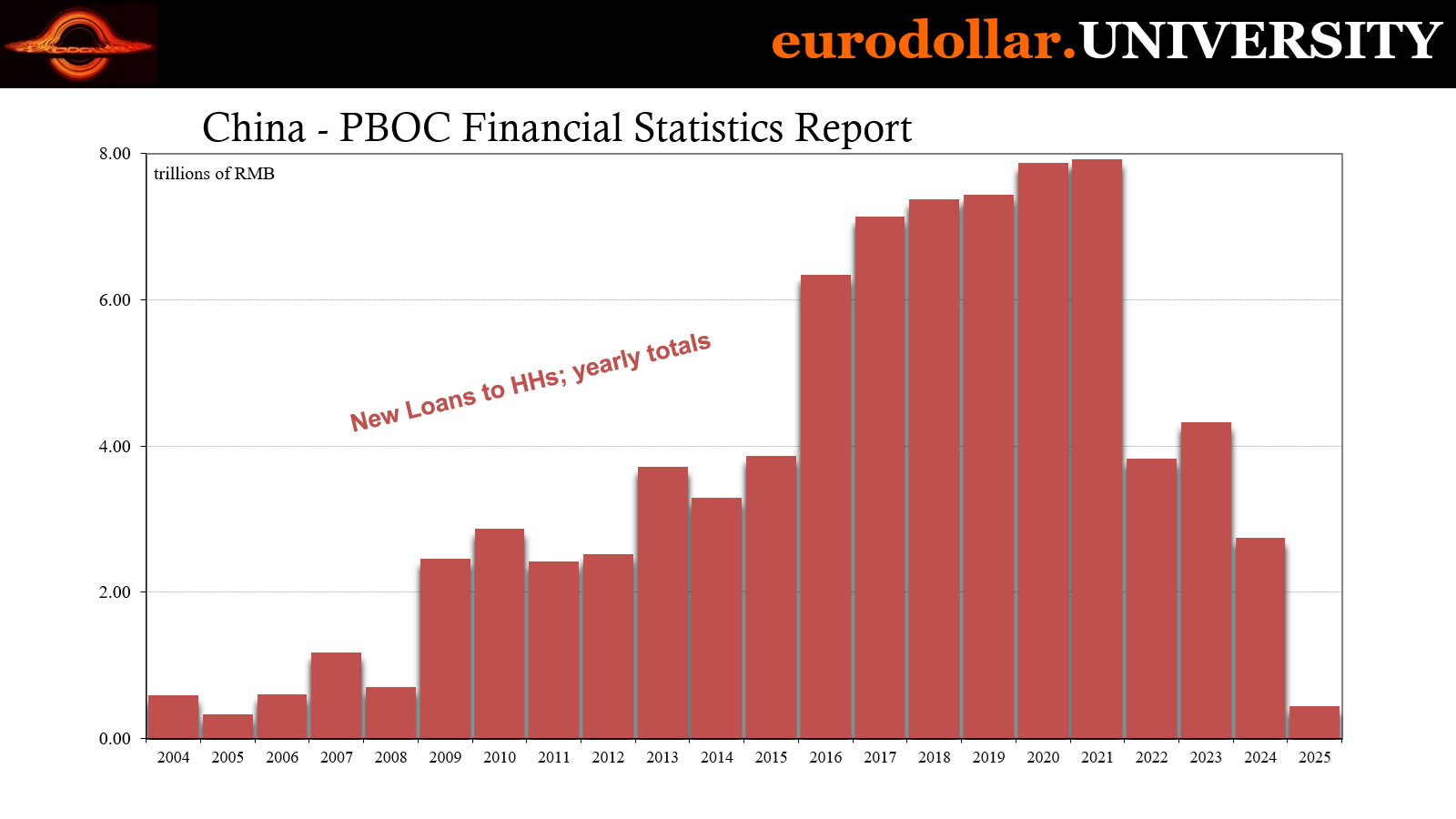

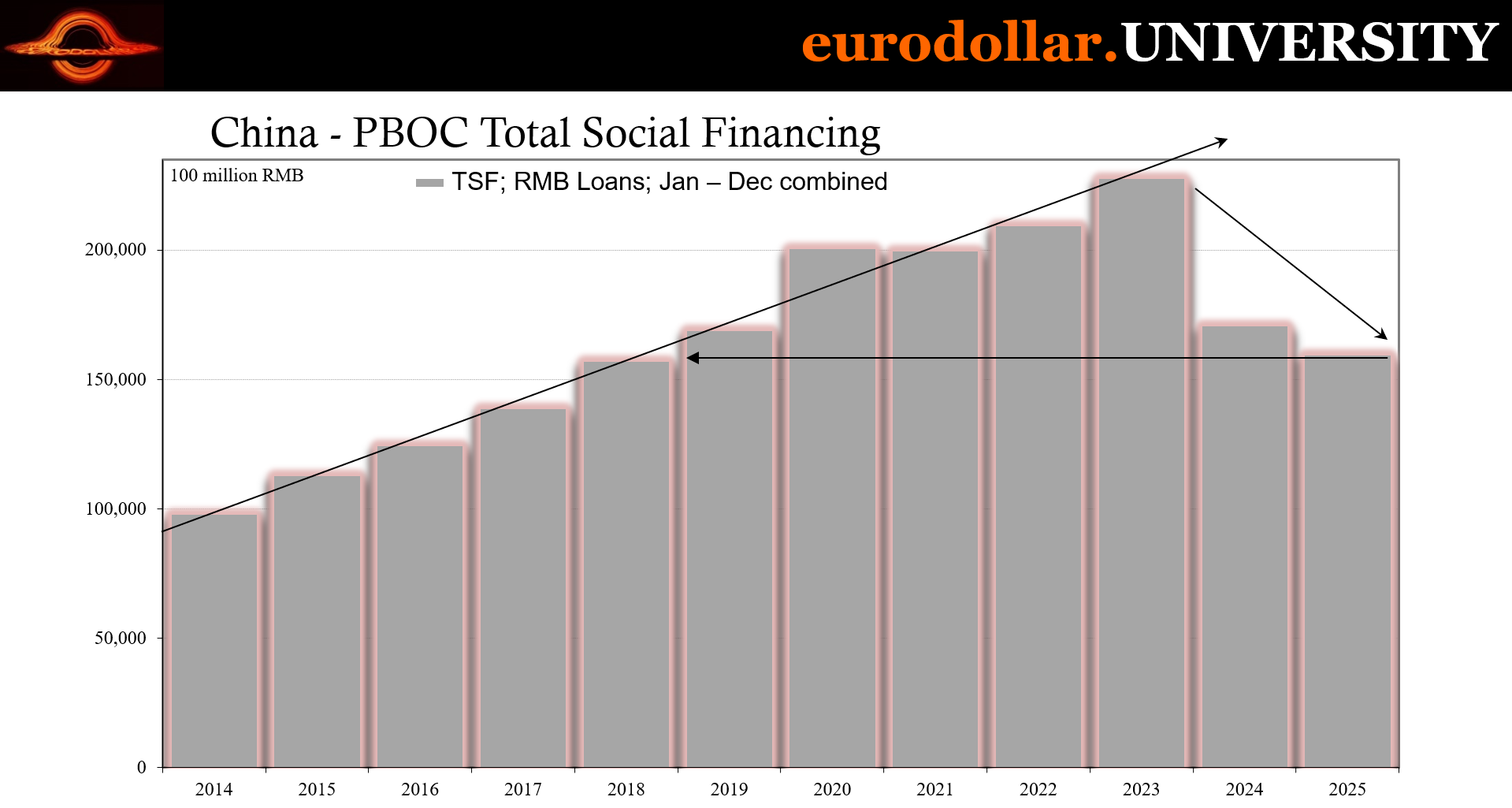

We were reminded of how much serious trouble again today with full-year 2025 tallies on banks and loan flows. The word “ugly” doesn’t do it justice. Lending to/borrowing by households utterly collapsed last year. Collapsed. Net loans went from CNY8 trillion in 2021 to practically zero in 2025.

Overall bank loan flows were the lowest since 2018. You get the picture.

In other words, China’s banks like its economy look like copper-to-gold not gold-to-silver. Then there is the fact the Chinese are responsible for buying much of that gold. Given how precarious their position is from trade to finance why wouldn’t they buy gold as deflationary protection?

Should the trade surplus reverse, straight away CNY is going to plunge just as a start. Gold as a portfolio (not monetary) asset makes perfect sense in that case.

On the flipside, the Chinese are only buying copper because of tariff restrictions. There is too much – way too much – copper inventory being squirreled away in the United States where it wouldn’t normally be only in case the Trump administration decides to include it in future duties. In other words, China is choosing to buy the gold in huge amounts while being forced into copper for only the short run (see: early 2024).

Silver looks like 1980, copper appears to be 2024, and gold is the one behaving in a way consistent with everything else. Sure, AI is booming on Wall Street (though not so much recently) but outside of purely data center building and more so borrowing, it does not suggest silver going straight up.

The Hunt pattern, on the contrary, sure does. And in its own inverse way, Coffin’s description of silver’s fall from grace way back when.

Artificial factors can and have created massive price distortions. We’ve seen it numerous times in history, a couple of those shown above from vastly different time periods.

It isn’t so difficult to check them against other information and test assumptions. Nothing is definitive, nothing ever will be until someone invents a portal able to see into the future. Without one, the preponderance of evidence, not to mention the overwhelming balance of common sense, says everything we’re getting is exactly what it appears to be.

For silver, too good to be true.

China is buying gold on purpose, copper because it has to, and silver has been taken over by temporary insanity. All because of government influence and interference. The more things change….

They say this time is never different. It would be nice if that was true, but there is no sane ratio which suggests it is.