‘SHOCK’ FROM THE OTHER BLS

EDU DDA Feb. 6, 2026

Summary: While we wait for the next report from the US BLS on payrolls, the ECB’s BLS on banking for the fourth quarter had a ton to say. Europe’s banks shocked observers and ECB researches with what they reported. It shouldn’t have been even a modest surprise given what really happened over the final three cockroach months of 2025. While hardly unexpected, the implications of this confirmation are enormous. That’s particularly true given the latest jobs data this time from Canada. More “unexpected” flat Beveridge.

ABOUT THAT GLOBAL RETURN OF RATE HIKES…

Markets did manage to calm enough for dip-buyers and bargain hunters, reversing some of the previous losses. Gold rose 4% while silver rebounded 10%. Bitcoin climbed 12%. Blue Owl regained almost 8%. Same volatility as before, only today was with the upside.

Will the tough times continue? The answer to that question may come from a surprising source; surprising to most people. European banks were queried by the ECB last month, as is the case every quarter, but they came back with shocking answers about plans for 2026.

The phrase from the Bank Lending Survey which stood out like a sore thumb was, “…net tightening signalled a high degree of risk aversion and a prudent approach to lending by banks.”

It doesn’t sound at all like “a good place” as Christine Lagarde and her minions at the ECB have been insisting, this “high degree of risk aversion.” That, instead, is entirely consistent with all this market volatility and maybe a lot more if it gets put too heavily into place.

The key in global credit dynamics right now is the willingness of banks to stand behind the system, mainly shadow banks. Many are contractually obligated to do so, perhaps as much as $2 trillion and equivalent across the US and European credit markets. But if the flat Beveridge world keeps flattening, contracts or no, banks have lawyers and have in the past not been shy about slamming the door on liquidity.

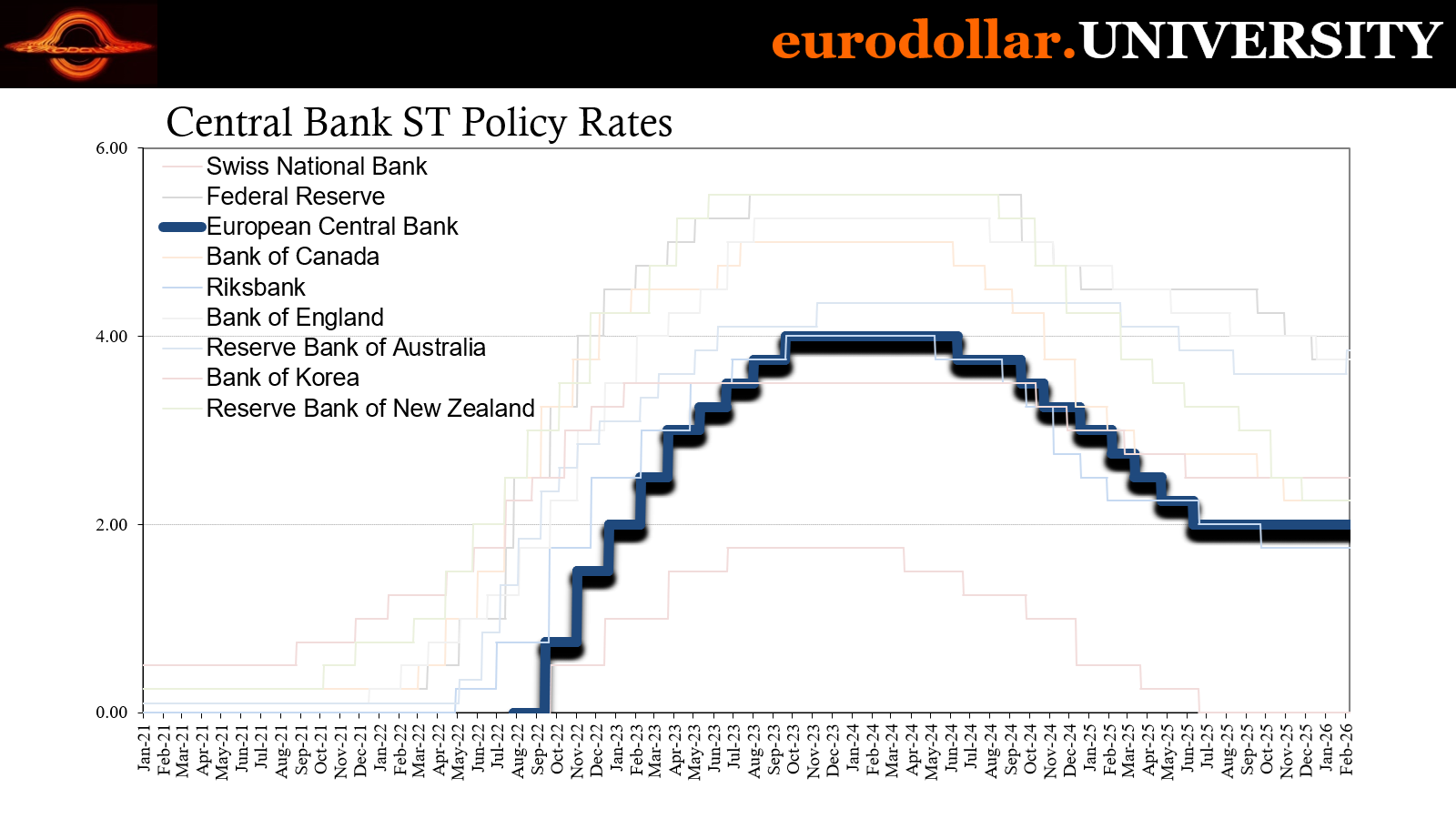

It’s another reason why the idea of all the world’s central banks following Australia’s in 2026 is already losing its appeal. Even though the ECB held its policy rates steady this past week, and as many Economist-types still hold out hope Lagarde or maybe her successor’s next move is a hike, Pringles are lurking.

More confirmation of such came from another part of the globe, this time from Canada where more “unexpected” job losses showed up and exposed the 2026-will-be-better narrative as largely based on artificial highs and tariff distortions, bad theory not economics.

Not that BLS

Today was supposed to have been January payrolls from the US Bureau of Labor Statistics, but, as noted previously, the release will be delayed until next Wednesday. In its absence, Canada provided some more flat Beveridge data (more on that below). Meanwhile, the lack of the jobs data gives us a chance to highlight Europe’s version of a BLS, or Bank Lending Survey.

It did not come out in the manner everyone was expecting. With the ECB having lowered rates by two full percentage points between June 2024 and June 2025 – far faster and farther than anyone had previously imagined; keep that in mind – it was supposed to have delivered powerful support to the European economy.

How?

Economists can’t really say for sure, it’s left as one of those things you just take on faith. For most people, it seems like it should have something to do with banks and lending. Lower rates mean lower borrowing costs. For borrowers, borrowing should therefore have greater appeal.

For banks and other lenders (like those lurking in shadows), a decline in interest rates might have the opposite effect since it could make returns on lending too low to be economical. Instead, central bank policy rates are thought to lower borrowing costs in money markets to help balance that out; if not go farther to the point the spread between short-term money and long-term loans (and debt securities) becomes favorable.

And all that is entirely plausible, yet still incomplete at best. Economics demands we take interest rates to be the primary, if not sole input. This is, once again, partly due to Economics’ reliance on econometrics which requires (over)simplification so as to avoid vastly more complex mathematics (a two variable covariance matrix has four inputs, three variables increases to nine, and by the time you get to ten that’s already a hundred so trying a more realistic model with tens of thousands is impossible).

But should computation and complexity issues for models dictate how we conceive of economic processes? That seems entirely backward, a major problem that has been raised in other areas of econometric-led study, namely inflation expectations.

For interest rate “stimulus”, the story doesn’t end with interest rates at either end of the yield curve even if, for the public, central banks simply want everyone to believe the simple model.

Rates are merely one input into the bank lending equation, more often than not a minor one. Instead, any lender must consider risks first and foremost. It’s the most basic yet least understood and never talked-about law of finance. Nominal returns by themselves are meaningless, everything works on a risk-adjusted basis.

That means even if the central bank is successful in lowering near-term money rates more than LT lending rates might decline (steepening), on paper the spread between them appears to have grown more favorable (“easing”) but only if those higher returns are not considered to be of greater risk.

In the latter case, though the nominal opportunity for lending is better, on a risk-adjusted basis the overall appeal of lending may not be. Rates go down, but lending isn’t stimulated since risk-adjusted returns have fallen more as perceived risks rise. Basically, balance sheet factors are what dictate lending activity and any changes in it.

ECB’s Q4 BLS ended up being yet another reminder of these basic small “e” economics.

A good place that’s not good

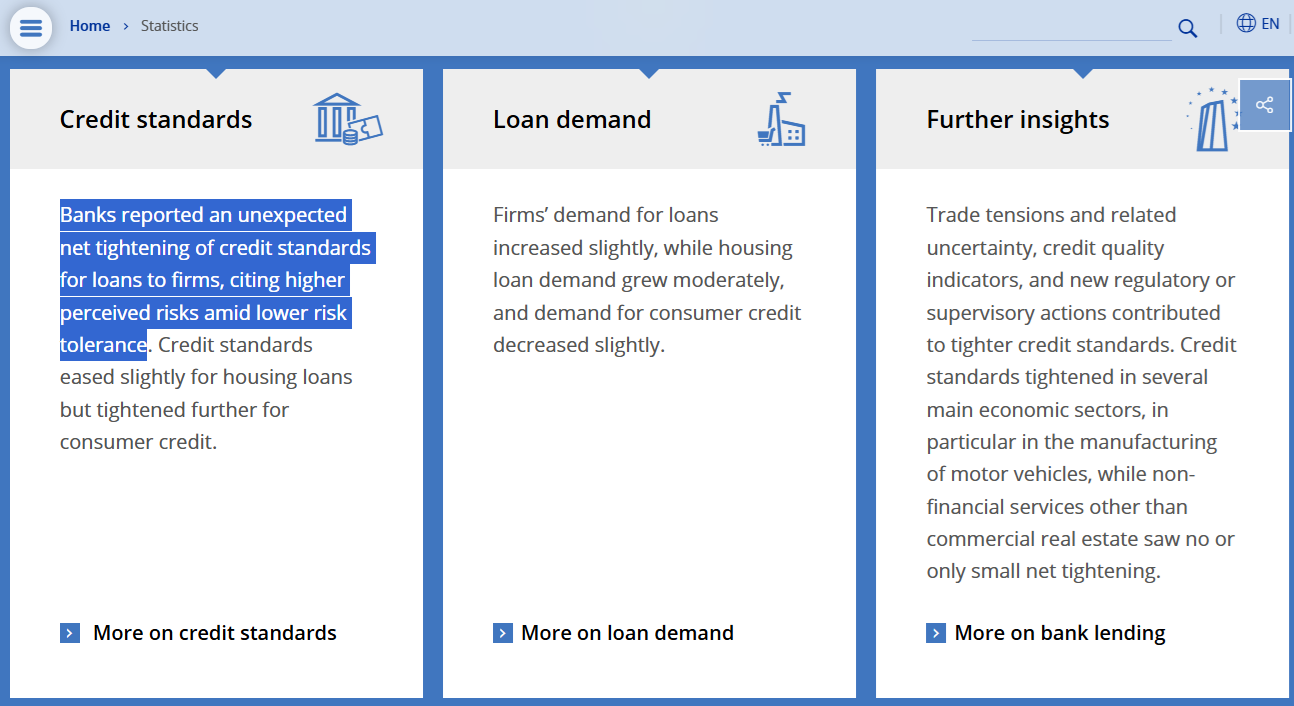

In tightening credit standards for corporates, the BLS noted how MFIs (monetary financial institutions, how the ECB categorizes banks) blamed basically everything for it. In other words, it wasn’t one thing or another, it was everything: perceptions of firm-specific issues, industry-specific matters, even the general economic climate. While the ECB continues to claim Europe is in a good place, its banking sector thinks quite the opposite.

From the BLS (the full quote to what was cited in the intro):

Concerns about the outlook for firms and the broader economy, as well as banks’ lower risk tolerance, led to tighter credit standards. The net tightening signalled a high degree of risk aversion and a prudent approach to lending by banks. [emphasis added]

It simply does not comport with either interest rate “stimulus” or the general outlook as expressed by the mainstream for Europe. The former is largely why the report calls this, “an unexpected net tightening of credit standards for loans or credit lines to firms in the fourth quarter of 2025.”

But it’s not just what banks are saying or thinking, they’ve already been acting on these perceptions and considerations.

Given what we of them, it already fits the profile. Loan values and balances are rising in absolute terms, but outside of any borrowing made by shadow banks (either voluntarily to under contractual obligation of pre-existing revolving credit lines) lending into the real economy continues to contract in yet another example of how small positive rates do not equal growth.

There is no material difference from when lending was outright shrinking from 2022 into 2024. The re-emergence of small positive increases for real economy loans merely indicates a smaller rate of ongoing contraction even as maturity spreads (the difference between ST rates banks might borrow at and LT yields they might receive in lending) grew more favorable.

This “puzzle” had already sent some at the ECB searching for answers (that are not hard to find and understand when outside of Economics ideology). In a blog post from late last month:

Current credit growth is weak by the standards of most previous recoveries. Our findings show that, especially in the first phase of the current monetary policy easing cycle, overall credit to the private non-financial sector grew at a rate that only slightly exceeded the rebounds seen in the wake of the global financial and sovereign debt crises.

As we know only too well, the rebound (not recovery) in bank activity following Euro$ #1 (2007-09) and Euro$ #2 (2010-12) was entirely too small for recovery conditions to materialize in the real economy, the top factor in turning the monetary crisis into an extended economic depression (see: Ben Bernanke).

In other words, what the ECB is “shockingly” figuring out is how those depression economics are already visible again here in the 2020s. It’s another way of saying forgot-how-to-grow and doing so from the banking perspective.

Trying to come up with some answer for why, the authors simply say they don’t really know even though they include the answer right up front on their list:

Higher risk perceptions, rising bank funding costs and tighter prudential requirements have further restrained lending. Meanwhile, direct lending from banks to non-bank financial institutions has risen significantly, partially substituting credit to firms, while non-bank financing has not expanded enough to make up the shortfall. Additionally, elevated uncertainty surrounding economic policy – also stemming from trade policy tensions – may have weighed on credit dynamics during the current policy cycle. [emphasis added]

The “policy uncertainty” excuse is really just another angle on “higher risk perceptions.” Either way, the Q4 BLS answers the “puzzle” more definitively with its “high degree of risk aversion.” Add the growing problems in private credit portfolios and this gets to be a much bigger problem moving forward.

Forward to a place that is not good.

Depression economics can’t be canceled

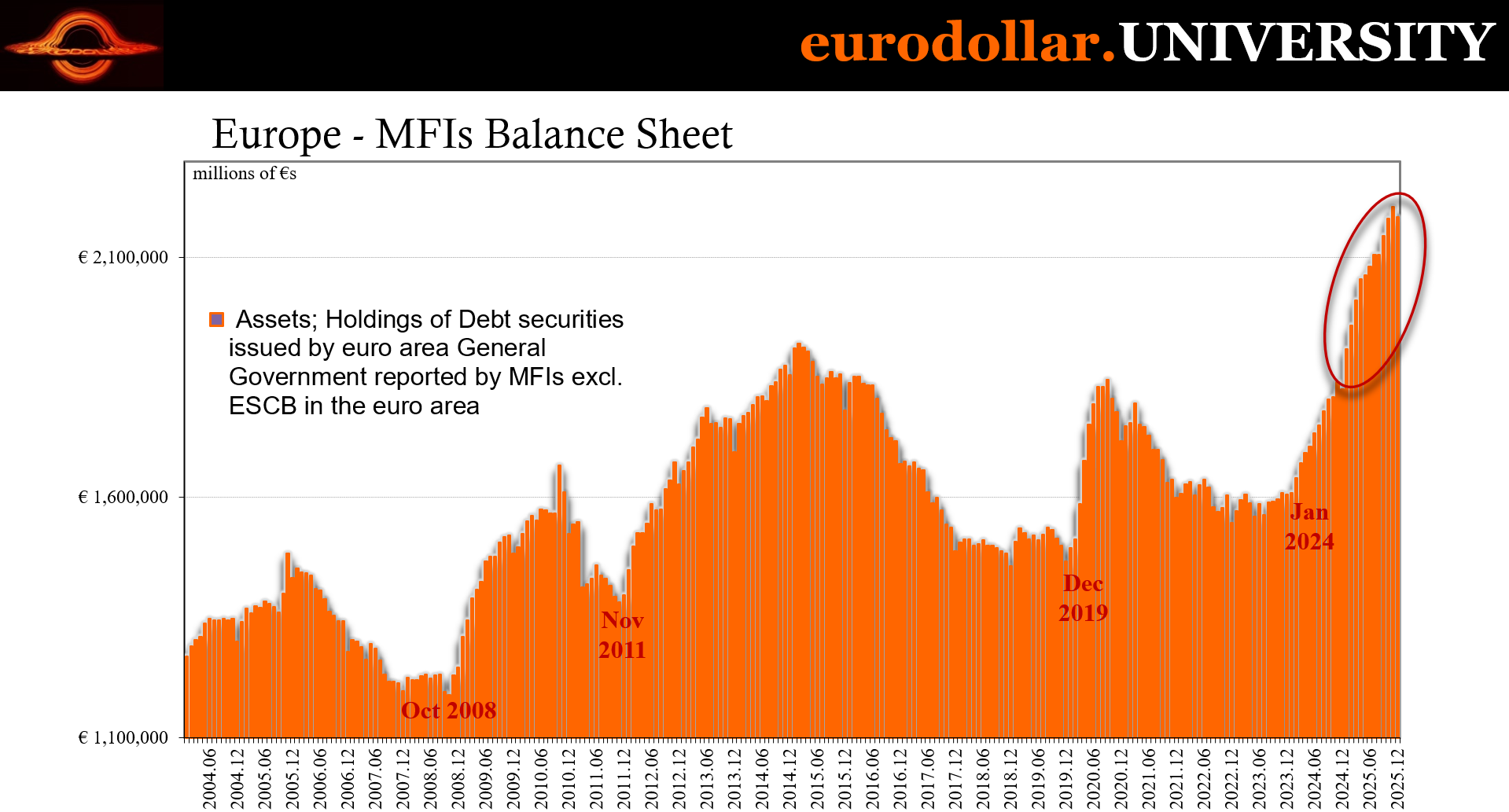

Unlike Economists, we already knew this was going to be the case just by how European banks were behaving over the past several years. Sure, they were lending to shadow banks, but more so building up massive, historic stockpiles of government bonds. According to the ECB’s data, MFIs added a mind-boggling €358.8 billion just in 2025, including the typical December drawdown (-€20.2 billion).

Not only is that a 20% increase on the year, it’s also substantially more than the “shocking” €220.1 billion MFIs had piled up in 2024 – which was a warning about the way things were headed.

Once the ECB began to cut rates, rather than convince European bankers those rate cuts were going to lead Europe to a good place, all it did was confirm rates are going to go down and that safe assets were the way to go for both reasons – safety as well as price appreciation on those bonds as rates fall to stay. Lending has done nothing at the same time, all of which makes perfect sense from the standpoint of risk-adjusted returns.

Government debt has very low risks, either liquidity or credit. Price risk is entirely about central banks, as everyone knows from 2022. Thus, the fact European banks undertook an epic bond binge in 2024 and 2025 shows they considered – and still consider – policy-driven price risk to be non-existent. If anything, it remains favorable even if the ECB would like the world to believe its next policy move will be toward higher rates.

Banks are not just disagreeing, they’re betting massively against it.

It’s yet another mainstream assumption that isn’t faring well in practice. Just like with the Bank of England, there is a growing realization that RBA and its rate hikes will be an outlier on that side rather than some signal for the start of a categorical shift worldwide. Economists have said they believe the rate-cutting cycle has reached its end, while European banks (and a lot more) are betting far heavier on a lot more Pringles still lying ahead.

Part of this disconnect also stems from how the mainstream views other forms of “stimulus”, that from the fiscal side:

For economic growth, hope rests on a massive fiscal impulse as governments raise spending on infrastructure and defense. Respondents predict Germany will benefit more from these investments than the euro zone as a whole.

Econometric models favor government spending, actual banks and commercial participants don’t see anything favorable about it given the complete and constant failure of any large program to achieve anything close to their stated goals (see: China). Berlin’s ongoing bazooka has to be considered in the context of China’s failed one even as the media and Economics won’t.

Stimulus has never been falsified, apart from every time it has been falsified - which is also every time.

If the upside for the “good place” rests largely on ECB rate cuts plus Germany’s massive bureaucracy allocating spending resources wisely and productively, no wonder European banks are under a heightened state of risk aversion and flooding into the comparative safety of government bonds just like it was the early 2010s all over again! It’s a mystery to ECB researchers and policymakers, standard economics and common sense to everyone else.

Let’s also not forget, all of this even before any real downside in shadow banking and private credit on both sides of the Atlantic really materializes.

Oh Canada

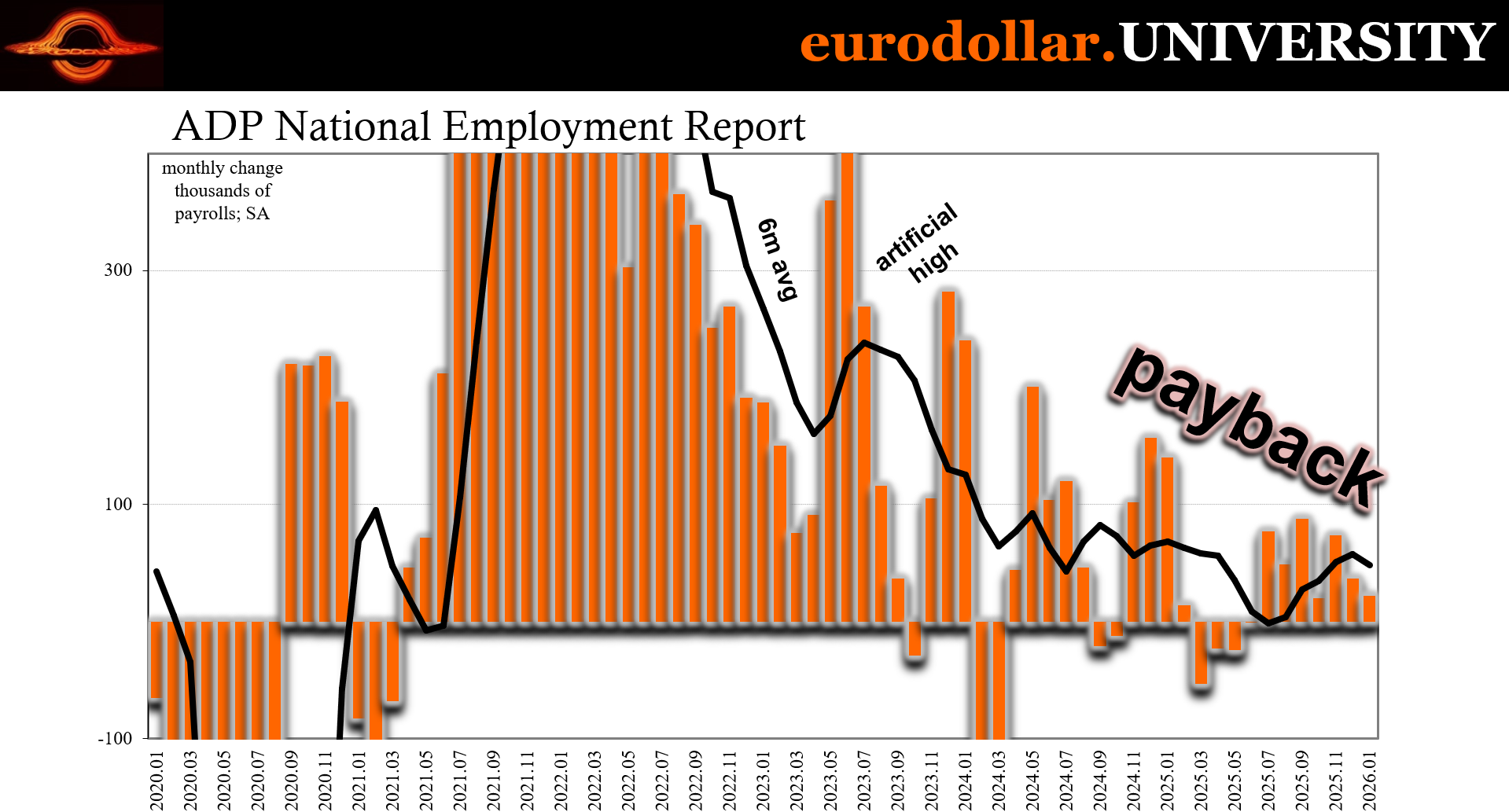

We saw this same pattern emerge from the new benchmark series from ADP for US private payrolls. The American labor market has been highly unstable since around late 2023 – right when the bond buying binge and global rally got going, no coincidence. In other words, the data is only now realizing what the markets did at the time.

Keep that in mind.

What the new figures from ADP show are job losses interspersed with job gains; a period of several months where net negatives arise followed by several more with additions. But rather than those increases starting a recovery trend, they always yield to more and even larger losses moving forward. The net result of this back and forth (a forgot-how-to-grow signal) is the trend keeps moving downward despite these short run variations surrounding it.

It becomes more visible in measures like the unemployment and underemployment rates even if mainstream attention focuses exclusively on the monthly changes – getting very excited about the positive ones only to then try to dismiss or excuse away the “unexpected” reappearance of negative months (plural).

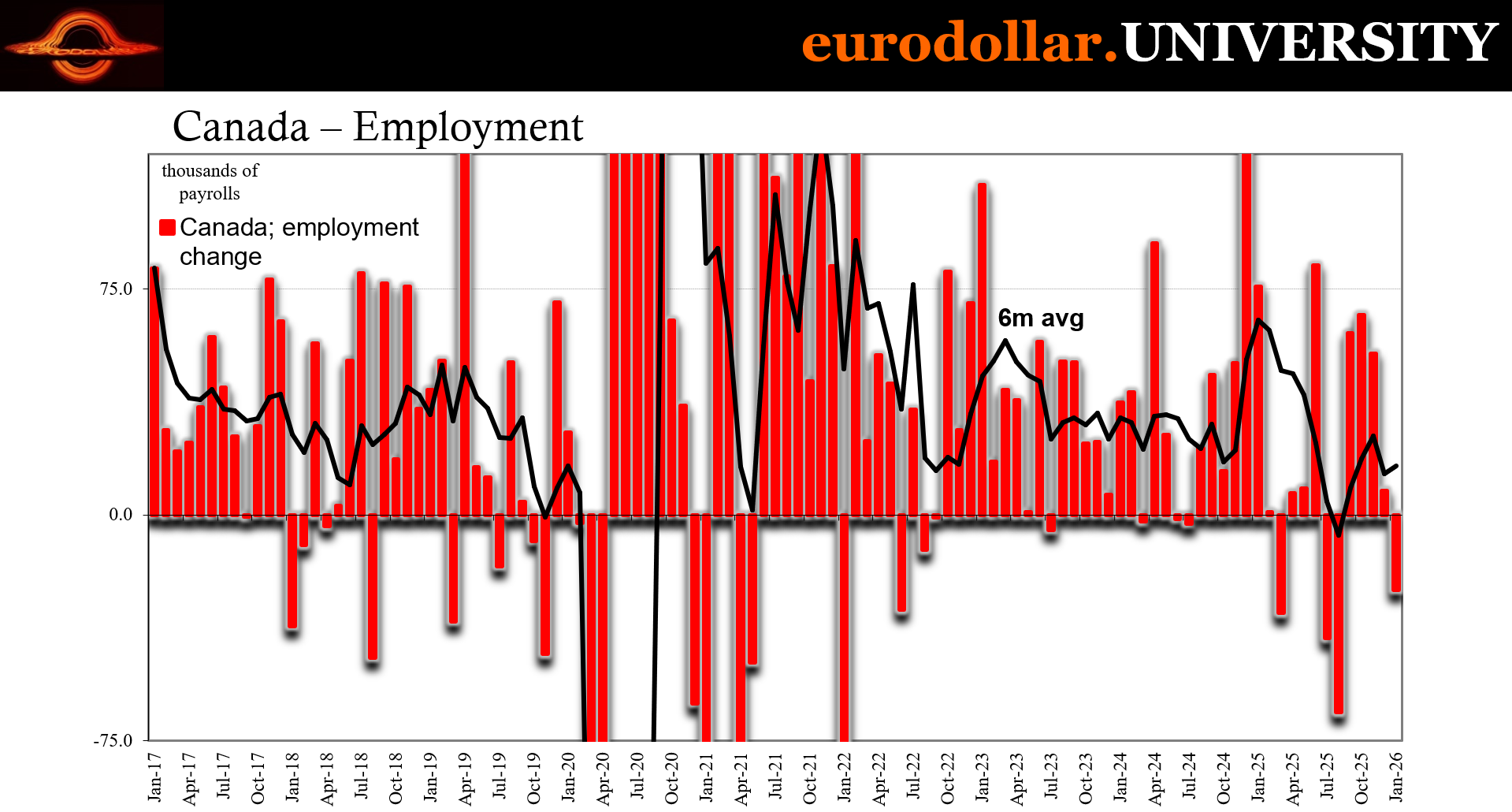

The same instability has been seen in Canada’s data, too. Only in Canada’s case, each and every time the monthly payroll numbers turn positive the Bank of Canada is quick to take credit and declare a full recovery. Tiff Macklem doesn’t even wait for the “long and variable” lags most Economists admit it would take for rate cuts to have an effect, assuming they ever could.

Tiff had done so early last year when the tariff front-loading late in 2024 and early 2025 had produced a clearly artificial spike in employment. Only to then pivot and blame the same tariffs for when the jobs numbers turned negative not long thereafter.

Like ADP, its new series, Canada’s employment data rebounded in the summer which fed into the mainstream narrative of a global economy stabilizing thanks to rate cuts and the end of “tariff uncertainty.” BoC even started to forecast its current policy level of 2.25% as its terminal rate, though careful to hedge its statements by claiming it would respond to any downside risks official models calculated had diminished.

But to finish out 2025, December employment growth slowed significantly, increasing just 8,200 which was basically zero (if not slightly negative in reality). That was followed up by today’s release which said Canada once again outright lost jobs (-24,800) for January 2026. Just like the US data from Challenger as well as ADP, this year which was supposed to start out on the upswing instead suggests another downside to the same back and forth forgot-how-to-grow pattern.

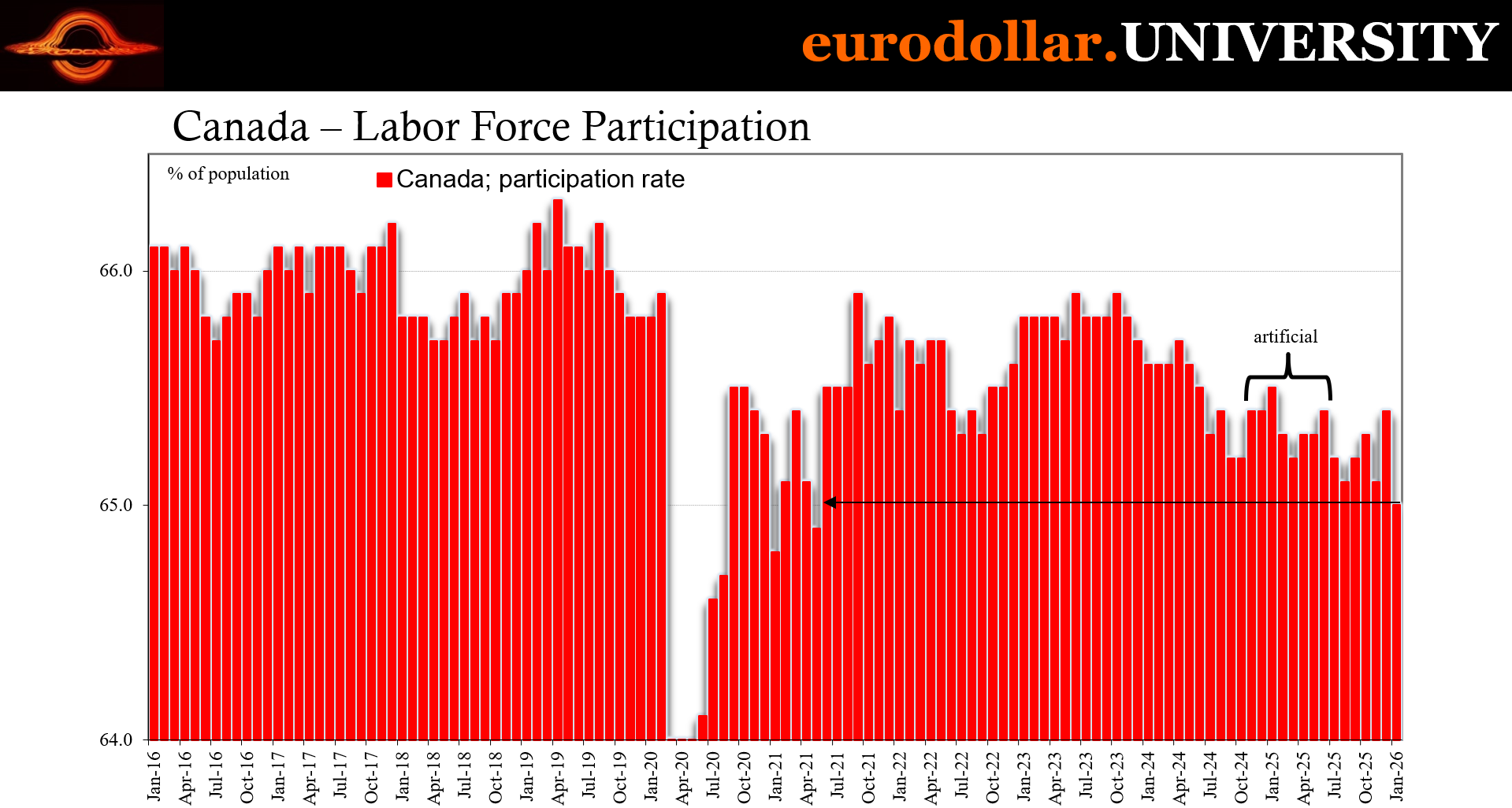

CANADA’S UNEMPLOYMENT RATE HAS DROPPED BECAUSE PARTICIPATION HAS COLLAPSED; WITH NO JOBS, FORMER WORKERS ARE DROPPING OUT OF THE OFFICIAL LABOR FORCE (SEE: BELOW)

In other words, there was no recovery last year because it wasn’t tariffs responsible for what was nothing more than the latest downside instability.

All of which on this side of cockroaches and historic shadow bailouts of shadow banks, European banks have no trouble defying “a good place” understanding the far greater implications behind labor market woes.

Stage 1 of any credit crisis is when money begins to reverse for the first time. The prior bubble saw only inflows as rationalizations, greed, and recency bias overwhelm rational thinking and plain common sense. Eventually, some sanity prevails, questions start getting asked and the excesses begin to unwind.

What distinguishes Stage 1 from Stage 2 is that during Stage 1 other sources of funding stand ready to make up the difference. Some investors want out and manage to get out, yet there are others who haven’t yet appreciated the dangers who take their place. By and large, though, it is the banking sector which must fill in the gap as outflows emerge.

Stage 2 is therefore when mainly banks stop doing so.

Given what we know of the real economy around the world, particularly through the lens of its labor situation, add that to what we just learned from European banks and their “high degree of risk aversion”, it wouldn’t be too big of a leap from where we are now to Stage 2, would it? A lot less than maybe it seemed before the BLS.

Now we wait for the other BLS and its benchmark revisions.