GOLD GETS CRUSHED

EDU DDA Jun. 10, 2026

Summary: Gold is being crushed, as is silver. While this isn’t unexpected, there is still value in the signal assuming we can untangle the reasons why it might be happening and, just as important, why it is right now. The mainstream will tell you its payrolls and CPIs. That doesn’t fit the actual evidence, however, starting with other financial signals. What instead emerges is a familiar property: an illiquid solution to a liquidity problem that has to first be liquidated.

Precious metals are getting hammered, continuing their deep selloff which began on Friday. That seems to suggest fears over Fed rate hikes might be responsible for the drop. However, as we know rates didn’t move all that much nor did the current CPI data for last month provide anything to suggest there is a greater possibility for KC Jeff Trichet to get a series of hikes.

The connection between rates and gold/silver has always been far more tenuous than it’s made out to be. If there is a correlation with yields (not specifically central bank policies) that would be the curve shape more than nominal levels. Even then, it doesn’t hold for long periods (such as the mid-2010s).

In the intermediate term, metals are havens (sometimes silver) and generally follow a fear factor. But in the short run, gold as a widely held reserve becomes an illiquid solution to a liquidity problem. Central banks and private sources liquidate bullion into some of the worst dollar shortage situations.

That’s what looks like might be happening here. I did a video today on the growing desperation among Asian authorities to contain their deepening currency woes which are, of course, triggered by…dollar problems. We already know those governments and central banks have been using reserves to supply dollar currency (eurodollar ledgers) to prop up their exchange rates, so it isn’t a big leap from liquid assets like USTs to another form which had been building up on various official balance sheets.

An asset that no longer has the same obvious upside price appeal it once did a few months ago.

Given the release of the US May CPI, we can quickly eliminate any connection to “inflation”, more specifically reflation (the “strong” and “resilient” economy). It’s a bit more ambiguous where it comes to rates, but we’ve already examined the curves for evidence on that factor.

I had been expected precious metals weren’t done with their “volatility.” Even so, falling prices are indicating something potentially significant.

Dropping fast

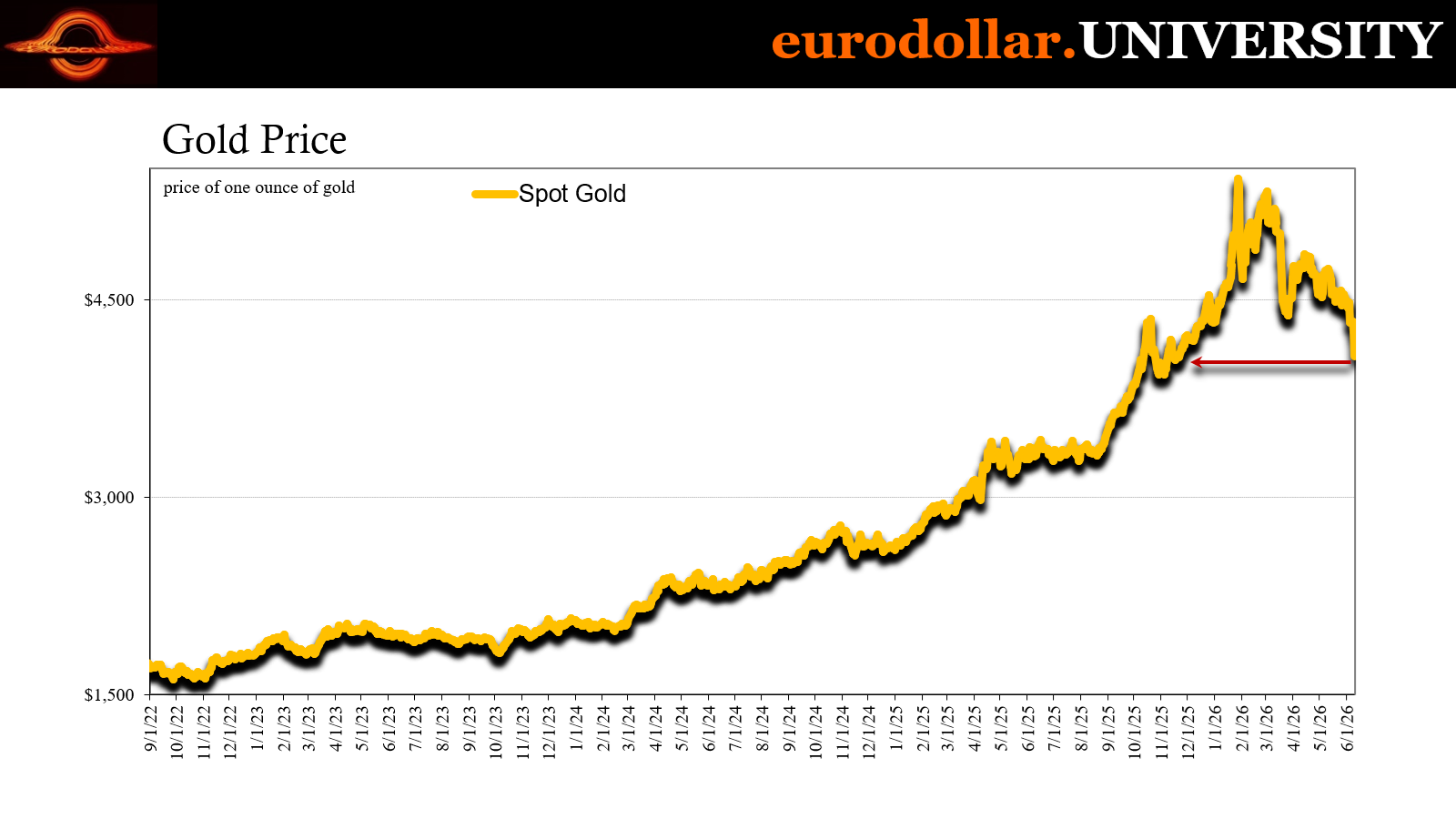

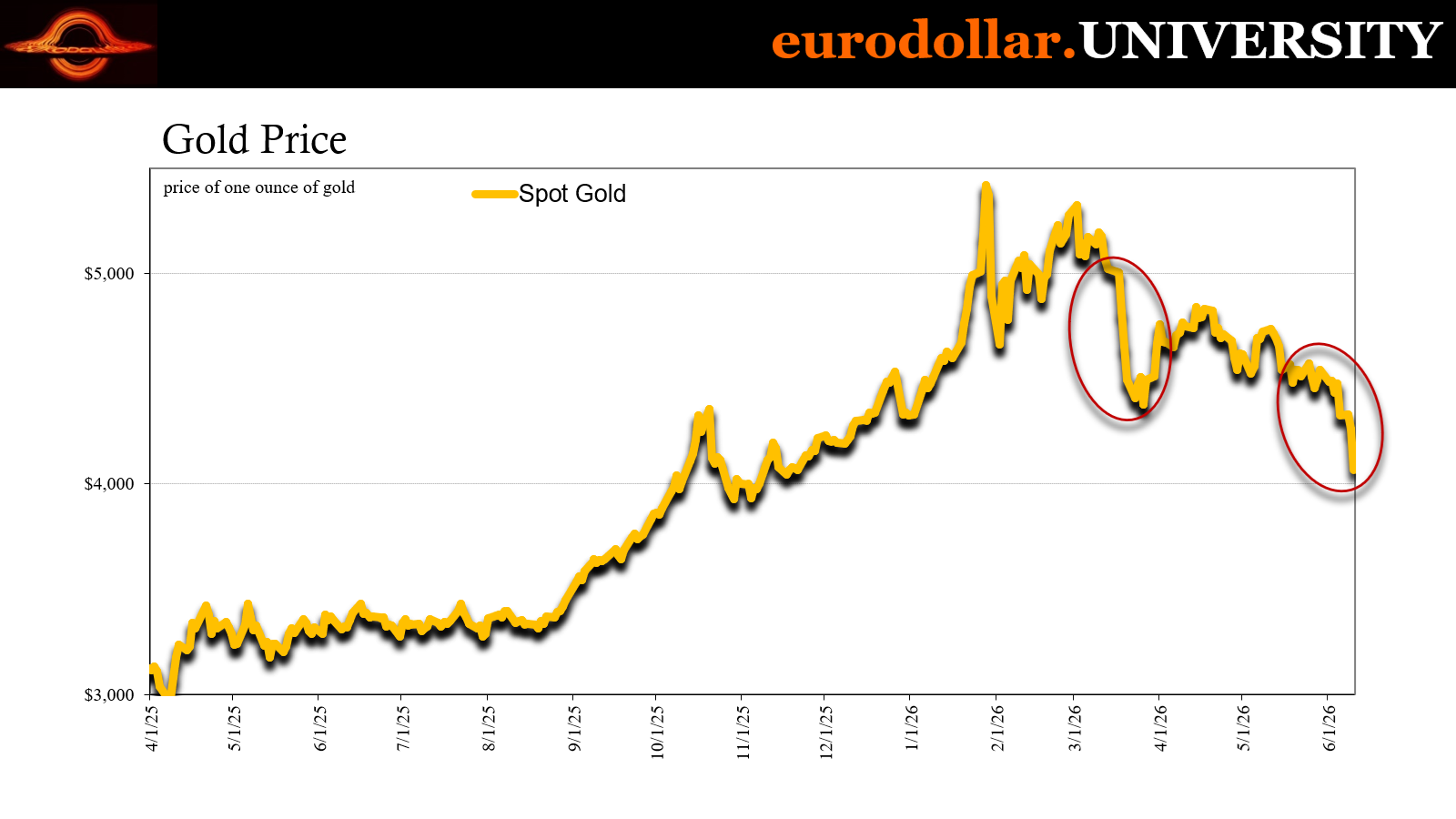

As I type, gold is trading below $4040 per ounce, having crashed by 5.3% today alone. That’s the lowest since November 7, representing a painful 25% fall from its record high in January. This isn’t a surprise since the yellow metal was due for an honest-to-goodness correction which it hasn’t suffered in a few years. Having soared as far and as fast as it had last year and to start 2026, the downside case was as strong as it was multifaceted.

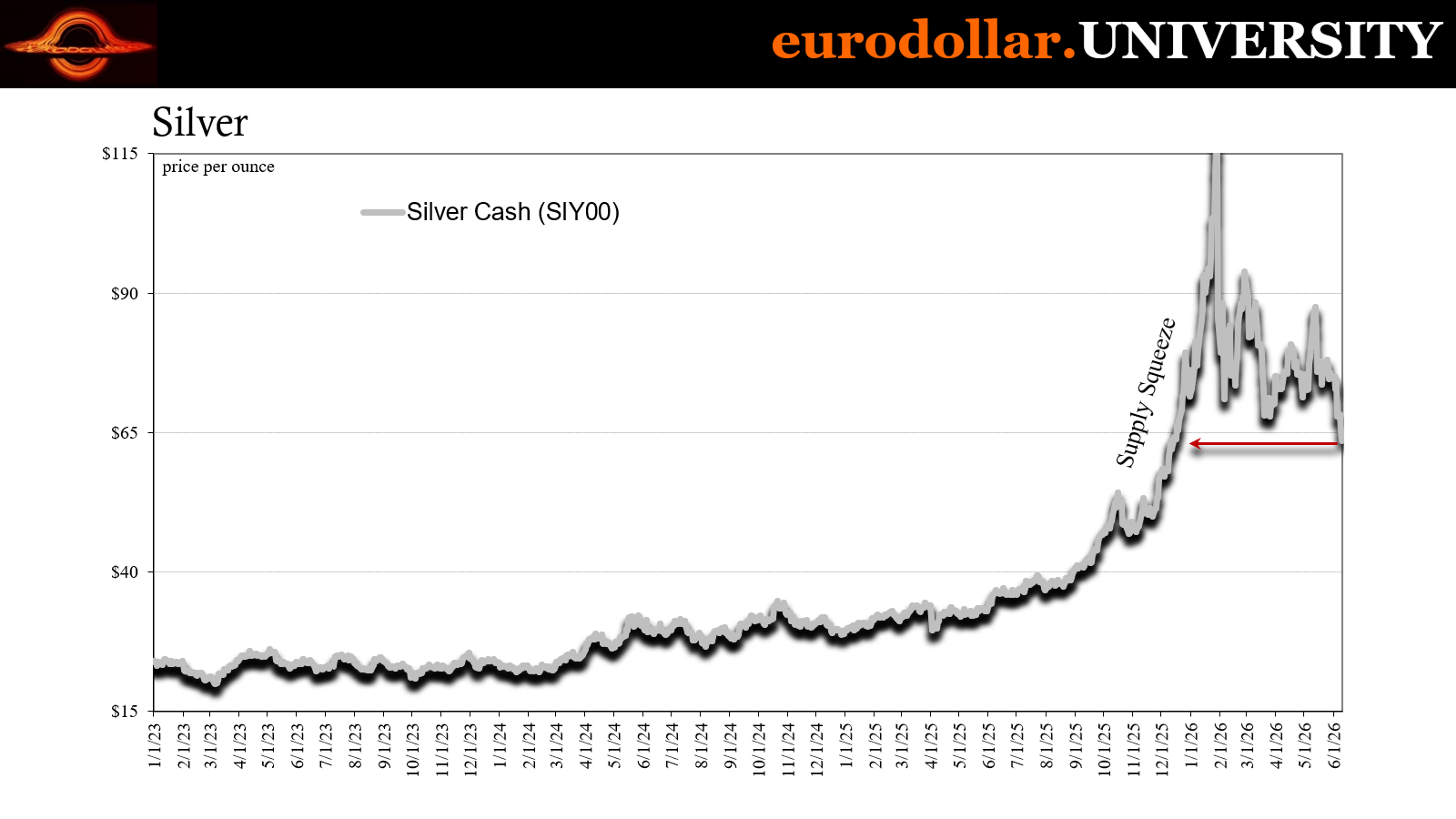

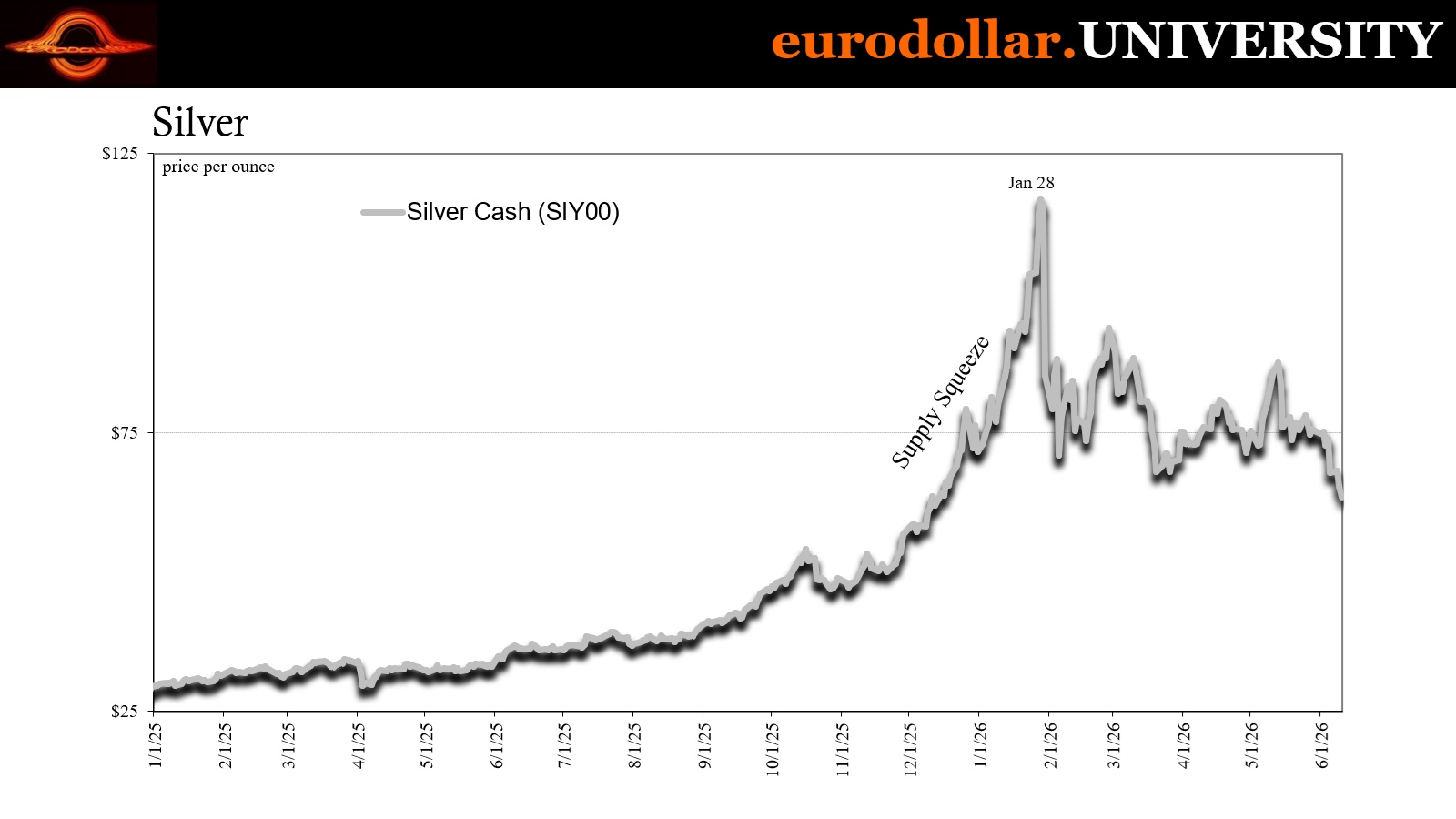

The crazy in silver didn’t help; talk about too far too fast and for the wrong reasons. I still believe that silver has a tremendous downside to its price (more in a minute), but the manner in which it comes about is just as important as how far down it could slide. Right now, silver is at $61.43, a nearly 6% daily drop and almost half off its all-time high.

Sticking with gold, this isn’t the first big-time crash over the last several months. Between March 17 and 26, bullion took a 12% hit. At the time, I wrote how much that looked like liquidations driven by what was then an emerging dollar shock triggered by an energy shock right then truly getting serious. So, the drop in gold was obscured by the initial arrival of the “inflation” narrative feeding rate hiking frenzy.

Later on, various governments and authorities would confirm they had liquidated gold to help address the dollar part of the shock, led by Turkey. Even the National Bank of Poland, one of the biggest official buyers the past few years, at the time indicated it might have to dispose of some of its accumulated holdings.

The current downturn is just shy of a 10% drop in only a few days, very similar to mid-March. While mainstream sources see Fed and KC Jeff, to me that’s much more like the prior example related to forced liquidations created by a growing dollar funding problem.

For silver, the damage is much worse, down roughly 17% currently from last Thursday. The downdraft in gold is one key catalyst for it, but also the higher beta because of how overdone the previous rally (parabolic surge) had been. Holders have been on edge ever since even when it looked like silver might rally again (which always happens) knowing there was a lot of that supply squeeze still needing to be addressed.

Despite the AI bubble and demand from industrial sources, last year’s enormous supply-driven jump greatly overstated the “reflationary” conditions in the real economy. In other words, there wasn’t nearly as much fundamental value in $100+ silver as had been said at the time or for the several months afterward. Tech buildout or not, there was no justification for silver being priced at those levels let alone the $200 people were convinced was coming next thanks to “robust” economic potential.

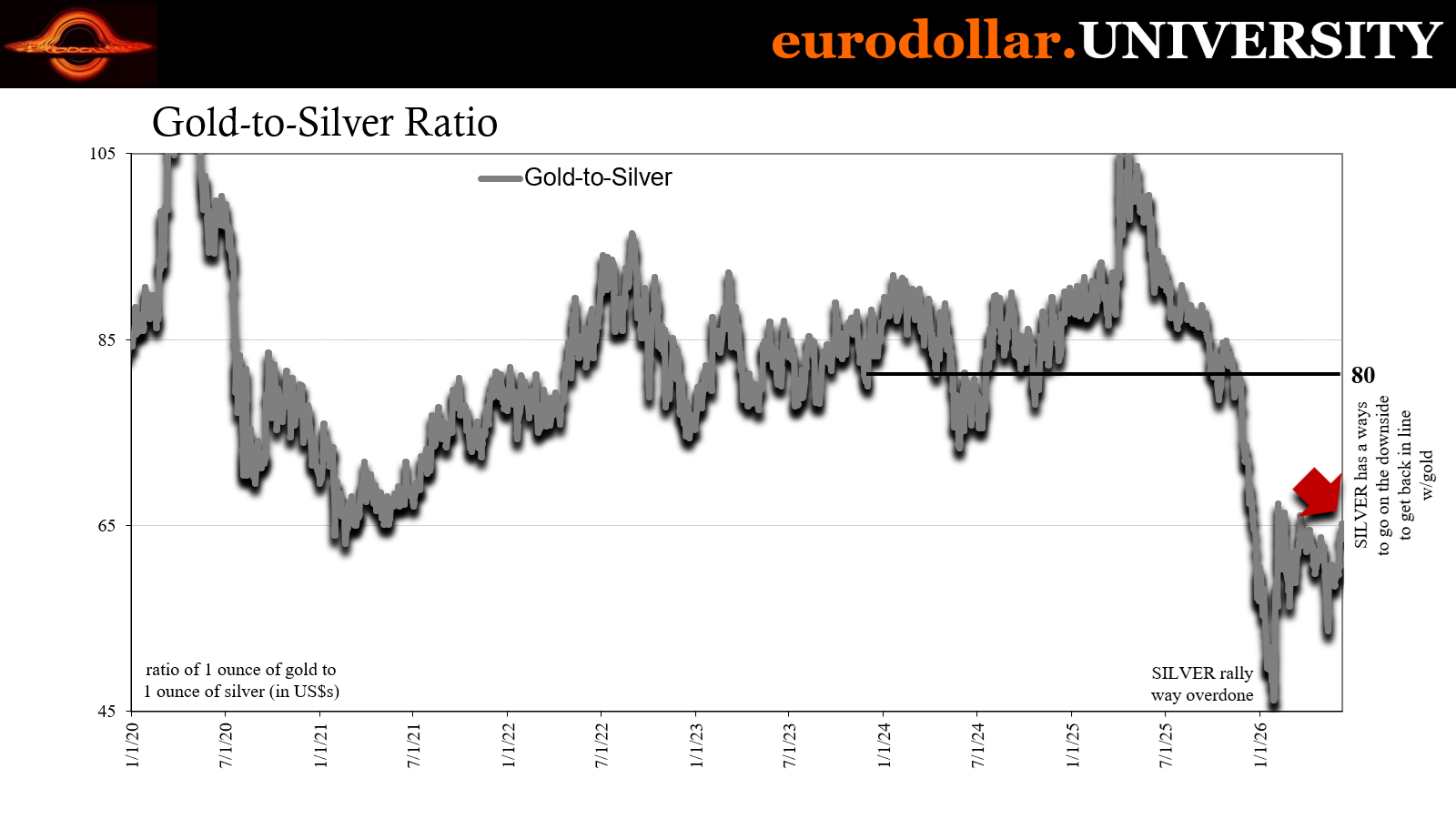

From the precious metals perspective, silver remained significantly overextended compared to gold. The gold-to-silver ratio had crashed to just 46, which straight away proved the surge had gone long past any sane price scheme. Since the trough in late January, the ratio never retraced more than partway back to more fundamental amounts, bouncing around between 55 and 65.

With this latest selloff, GtS is still just below 66 – and that’s with gold down sharply. If bullion didn’t drop any further, to get back to 80 – which is the likely minimum – silver would have to fall to $50, which is exactly what I wrote last fall. Knowing, too, how markets always overshoot in both directions, fifty bucks is probably just the start to where the true bottom is likely a lot lower still.

Should it get that far, it would represent a tremendous buying opportunity. Same goes for gold. The fundamentals for the latter remain fully intact, those of the safe haven and yield curve connections. And should the curve prove accurate on the future of rates ahead, meaning the full Trichet both up and then later down, all the more reason for precious metals.

Another important question for specifically silver is what its downside might signal for the industrial part of its price and what it might further indicate about expectations for, or even current perceptions of, what’s really happening with demand surrounding AI. Not stock market views, real commerce and physical material. But that’s a topic for another day.

Right now, gold looks liquidated which fingers eurodollar conditions and Asia. Again.

Rate side

Any mainstream commentary about gold will only point to either interest rates or inflation. However, the latter obviously doesn’t fit since most people are convinced inflation is a threat – thus, rate hikes – but gold isn’t responding the way it “should.”

That’s because gold is not an inflation hedge and never really was, not in its demonetized format. Gold is not money and hasn’t been in so long there are few currently alive who could have experienced otherwise. That means it doesn’t “compete” with the dollar (really eurodollar) so it wouldn’t therefore be an inflation hedge.

It is purely a portfolio (reserve) asset. That’s one reason why gold is stacked up against interest rates, competing with Treasuries for safe haven demand, except where bonds pay interest. The opportunity cost is thought to be a key component to precious metal demand.

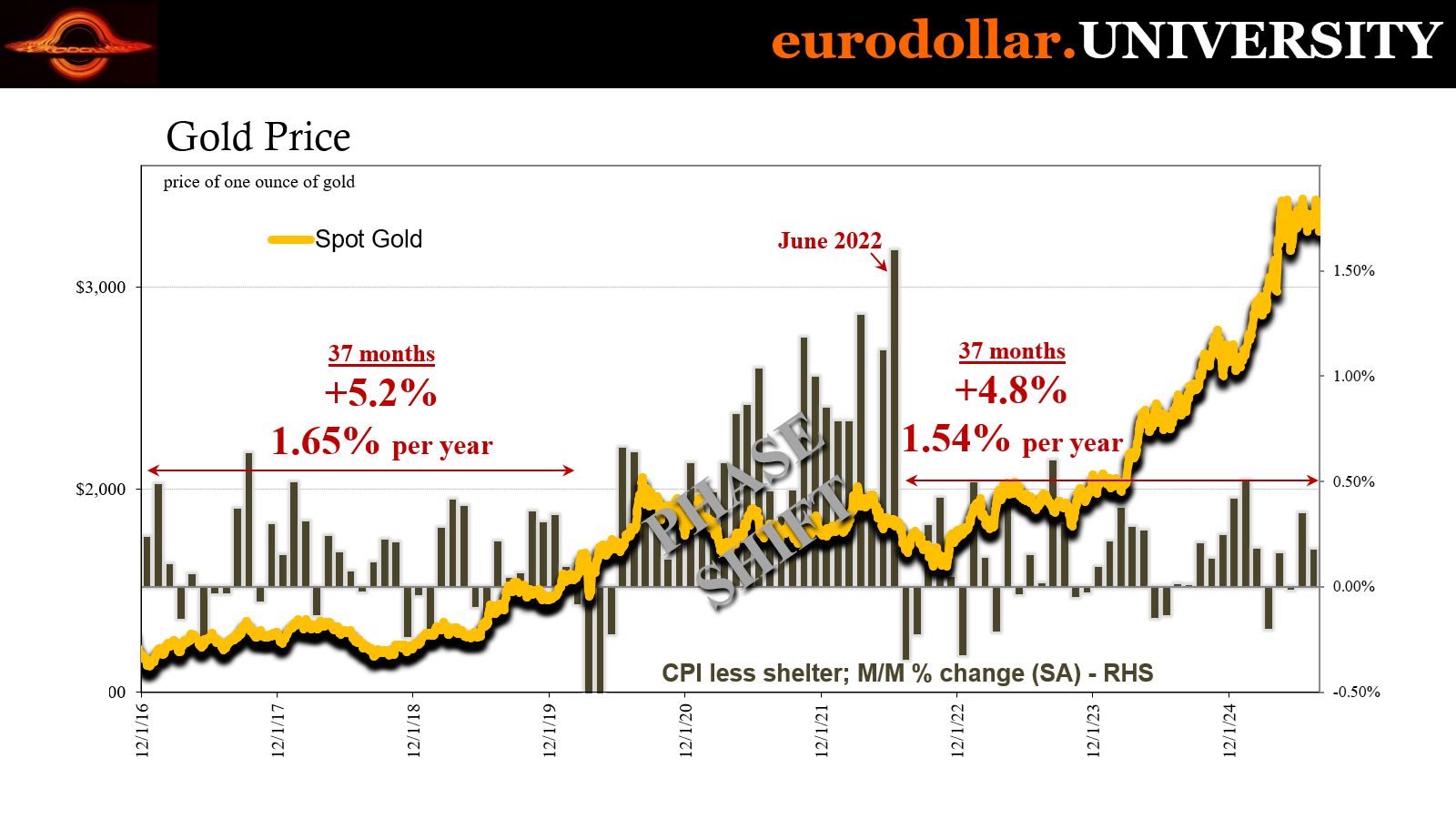

Yet, there are several instances when that doesn’t work, either, including a few more recently here in the 2020s. Gold started to rebound in 2022 even while central bank policy rates were still rising rapidly and UST (and other) market rates were at least moving higher. Despite the initially unfavorable opportunity cost, demand for bullion was steady anyway due to the perceived need for safe havens (forgot-how-to-grow recessions rather than 1970s inflation).

You could make that into an interest rate argument, but it still ends up in the same place; meaning, those buying gold starting late ’22 and throughout the hawkish ’23 were doing so anticipating lower general rates in the not-distant future, which did happen starting in ’24. Gold buyers were looking somewhat further down the road past the mainstream rhetoric of the time.

But that’s why there is a correlation with rate curves, which were increasingly pricing the same thing. That’s what inversion had been, a signal for the growing need to find safety beyond the short run.

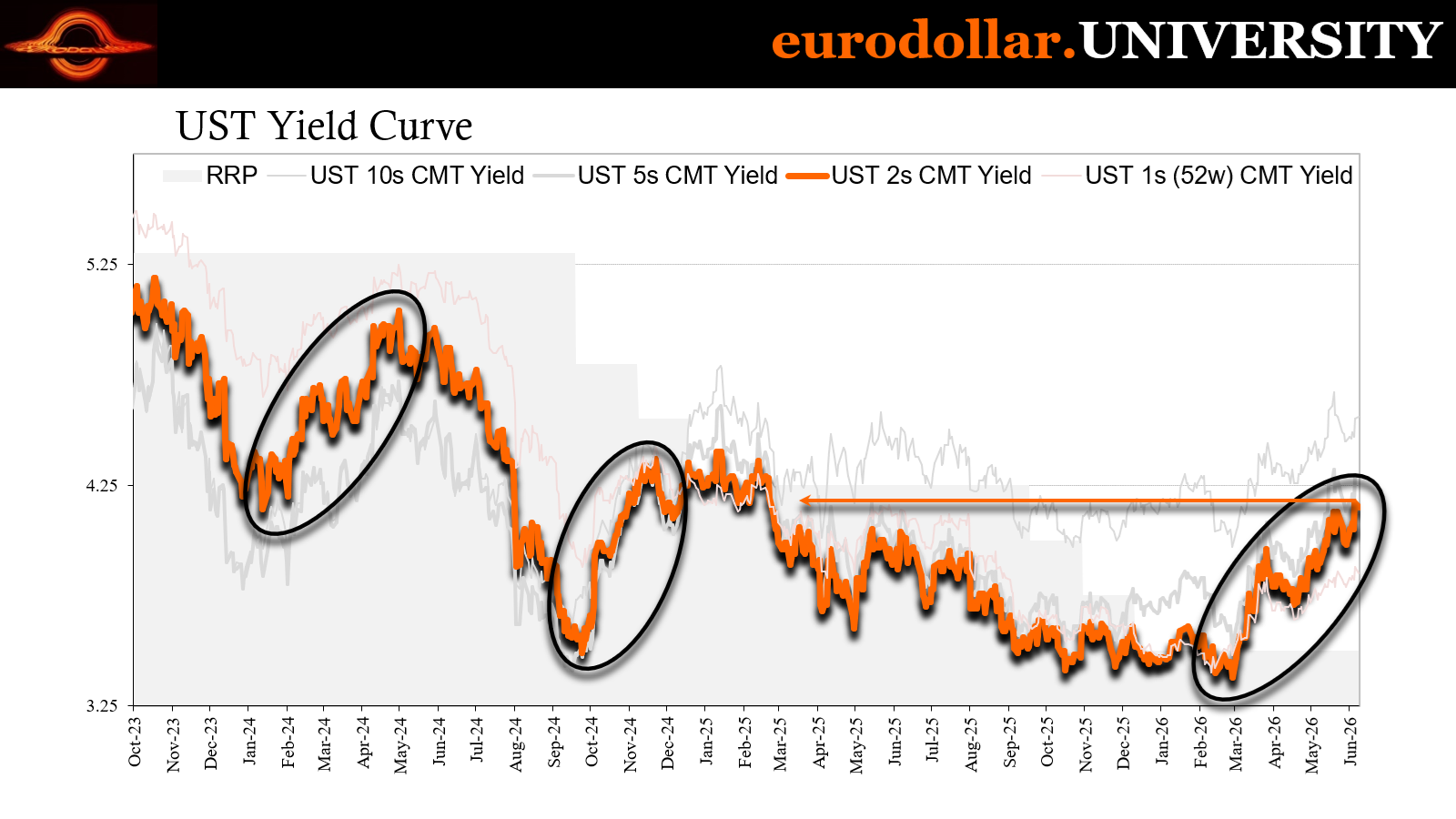

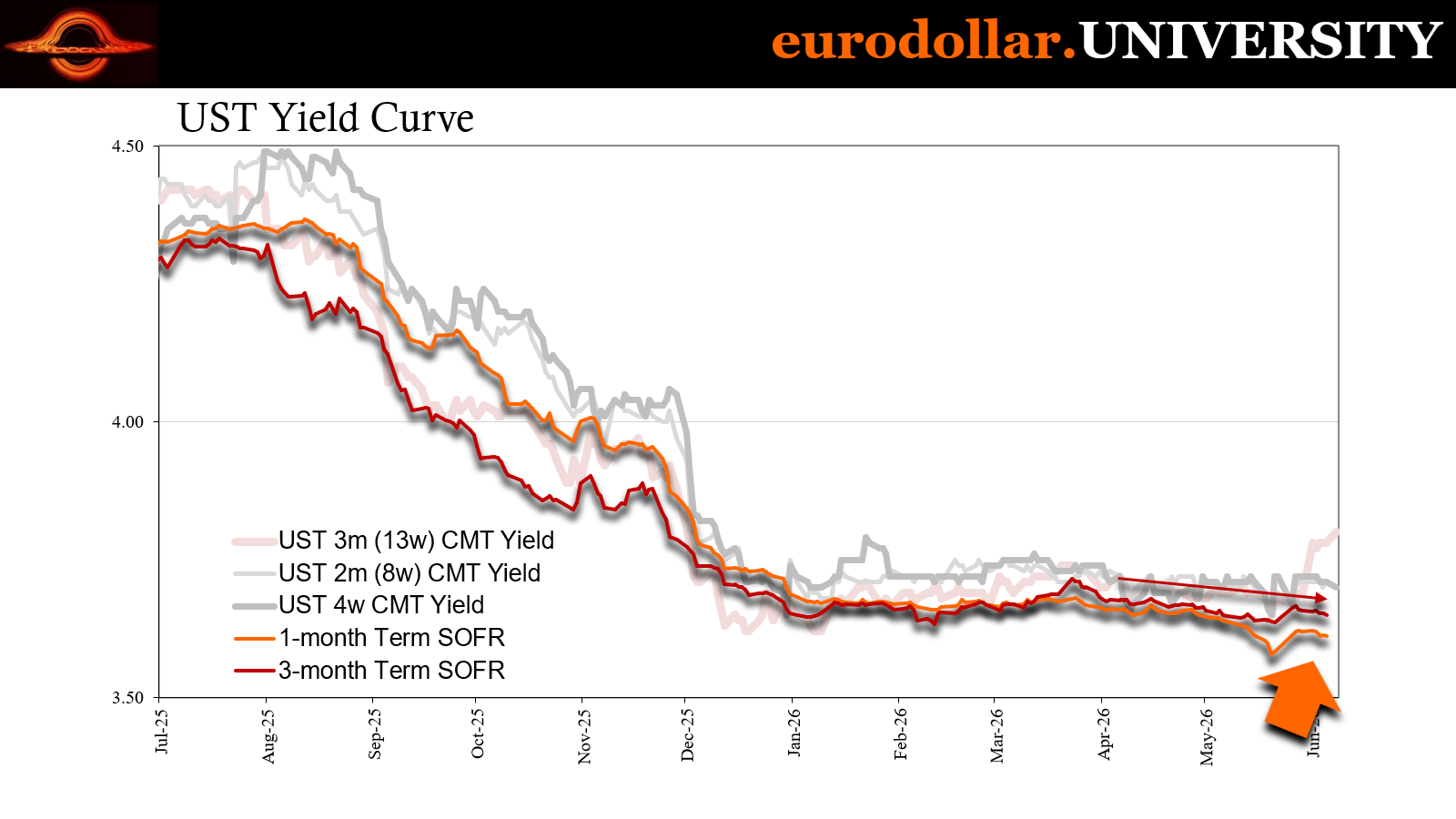

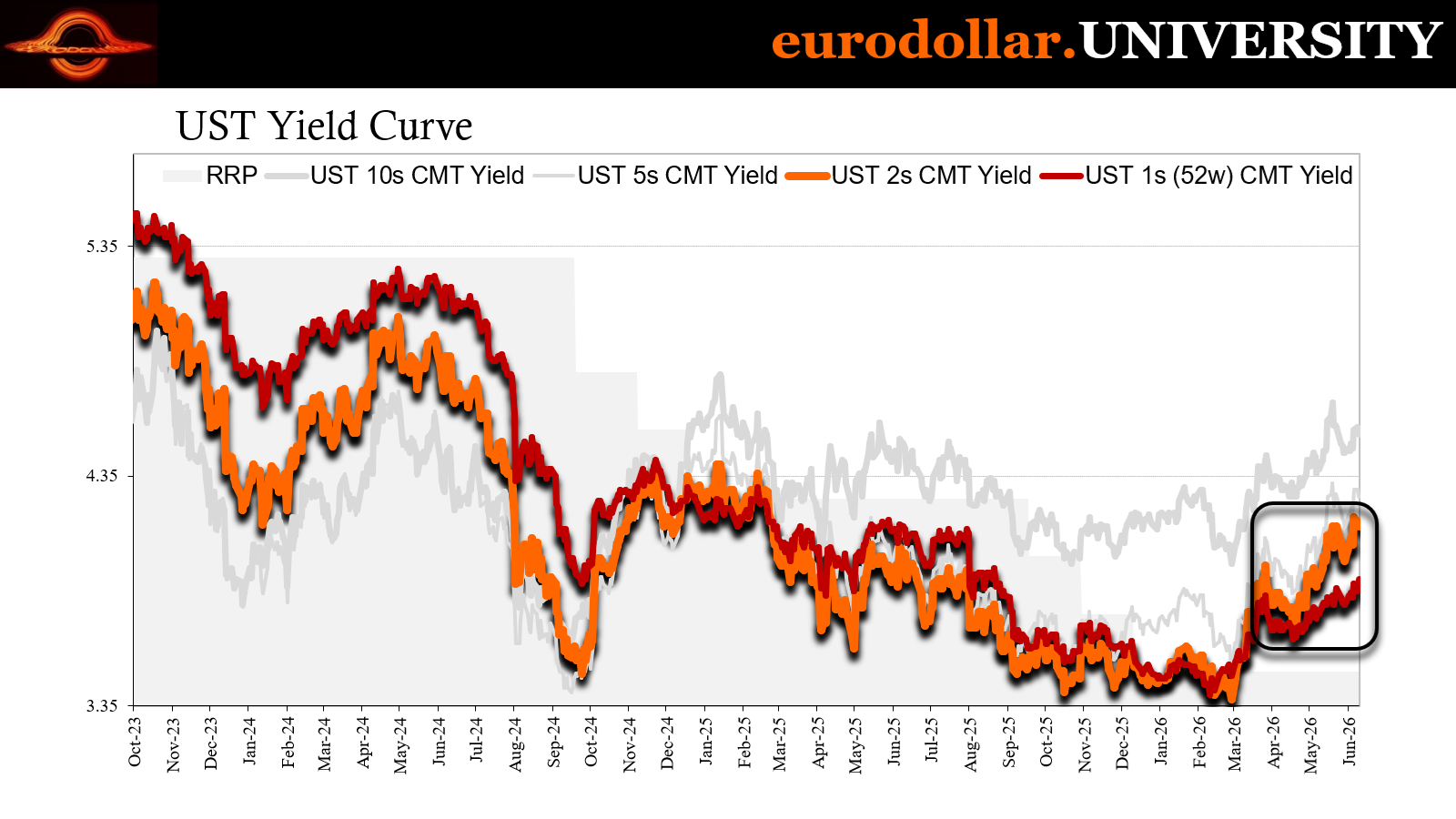

As far as June 2026, there is the superficial connection between the current selloff and perceptions of a hawkish shift for various central banks starting with the Fed. The “resilient” labor market represented by the May payroll headline makes the prospect for a rate hike or two more likely for mainstream observers. But as noted yesterday and Monday, the yield curve is only modestly hedging for something like that.

Though the 2-year yield reached its highest since last February, that is overselling the move. As also previously discussed, the backup in Treasury rates this time is comparable to two other recent examples, both in 2024. In fact, the increase in yields (at any spot on the curve) is less right now than either of those. Yet, gold didn’t crash while they happened two years ago.

GOLD DID NOT CRASH EITHER TIME IN 2024 WHEN RATES AND HAWKISHNESS WERE RISING

Some other factor has to explain why this time gold is experiencing such a violent backlash. The last time it had was early last April when the metal sank 5% in a couple of days – during that dollar shortage. It was similarly liquidated before haven demand stabilized the price.

Throughout last spring and summer, gold was mainly sideways not because rates were rising over hawkish central bank statements fixated on “tariff inflation”, rather a period of consolidation as the acute safety bid lost some of its urgency while risky markets (such as stocks) rapidly re-risked.

Once the jobs and credit markets revealed more weakness (not to mention the summertime confirmation of China’s downturn), consistent with the bull steepening on the yield curve, gold took off and didn’t look back until January.

There is nothing today which suggests interest rates over the intermediate term are going to be anything other than the same general range, including the possibility of a Fed hike in there, too. Even if KC Jeff can get the FOMC to go along with Trichet-ing itself, would +25 bps for fed funds and SOFR really account for a 25% drop in gold, both 10+% crashes making up most of that slide?

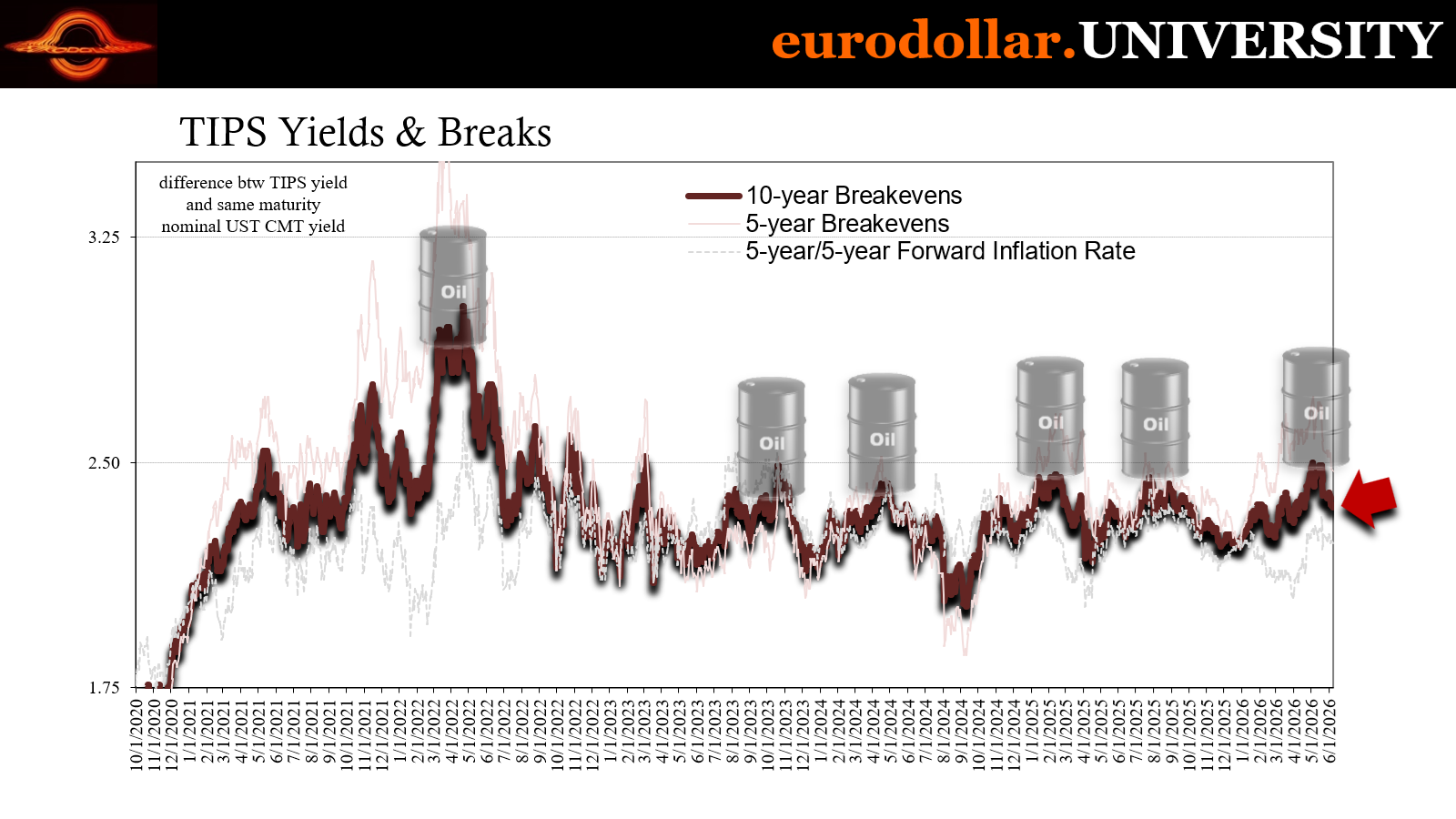

It’s another example of how the mainstream forces everyone to default back to the Fed without thinking. Don’t Fight Whomever The Current Chair Is. But that’s not what either gold or rates markets are saying. TIPS breakevens were steady at recent lows today while the front-end bills were down slightly. Even the 3m rate, which had moved higher on a potential rate hike, moved back down a few bps.

There is something far bigger depressing PMs than the rantings of obsessed central bankers who claim to be chasing inflation that, once again, the markets don’t buy nor is there any evidence for.

Here we go again

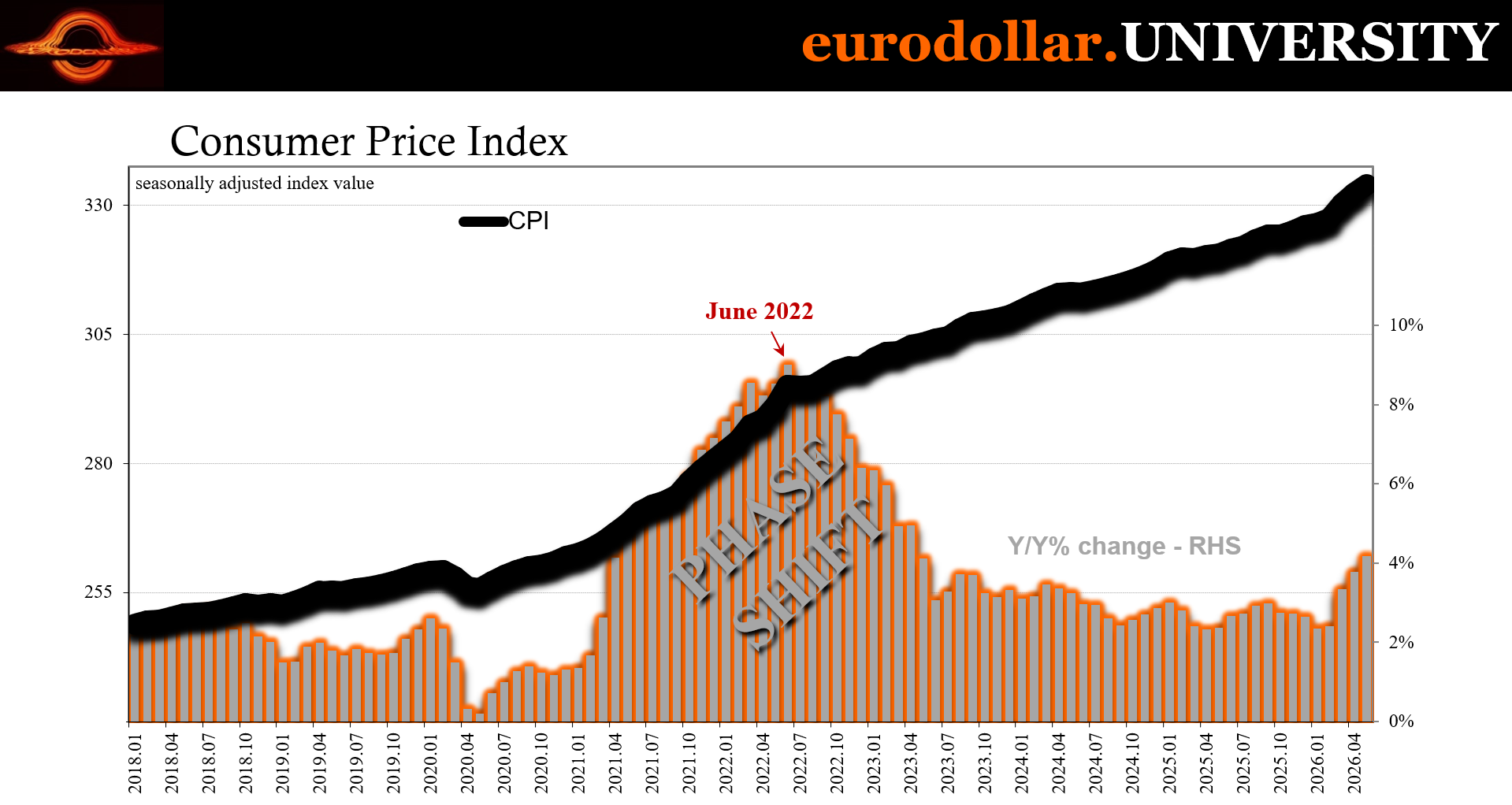

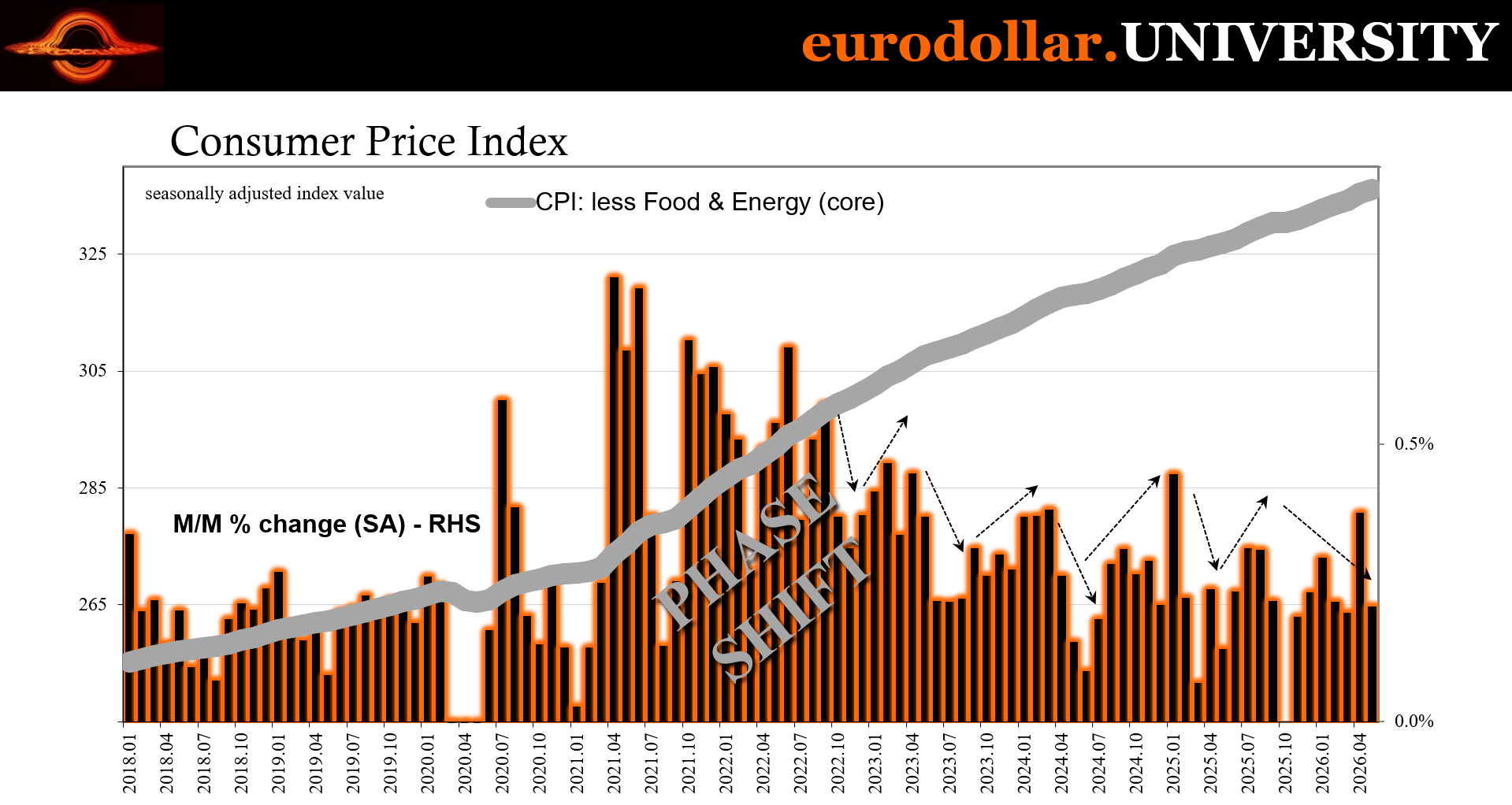

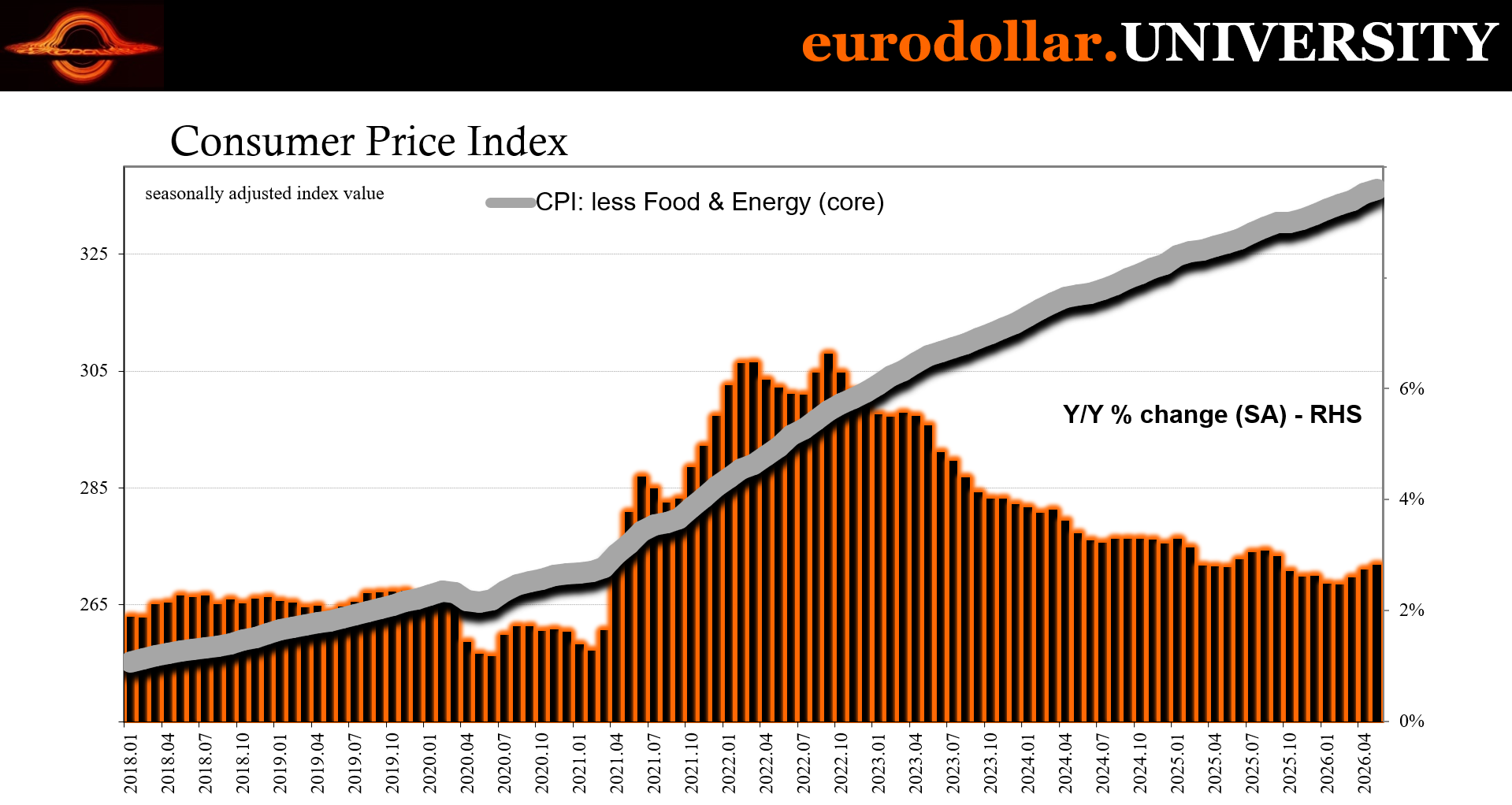

Yes, we just did this with “tariff inflation.” To be fair, there is a key difference this year compared to last: headline CPI rates have indeed surged in a way they weren’t ever going to in 2025. The latest data puts the annual change for May back above 4% for the first time since May 2023. It was just 2.35% back in January.

But that entire acceleration has been contained to the energy shock and its direct impact through motor fuel. What central bankers and Economists (same thing) are on edge about is what they call second order effects; that is, gasoline and diesel costs go up forcing other businesses to raise their prices in response. This is the part that sounds most plausible; after all, profit-maximizing firms aren’t going to willingly take a hit to their margins.

Just like tariffs, however, the choice isn’t entirely theirs to make. If consumers can’t afford higher gas, then a service provider who does have to pay higher energy costs to provide that service won’t be able to raise its price no matter how much the business might want or even need to. This is basic economics (small “e”), not that other stuff thrown around in central bank econometrics.

In 2025, there was never any evidence for second order “inflation.” Never mind how the markets (TIPS, yield curve, forward rate, swaps) consistently priced zero chance of it, the CPI and PCE data consistently failed to show any other. “Tariff inflation” was never anything more than an evidence-free theory; one KC Jeff was willing to rhetorically die for anyway.

Any day, they said.

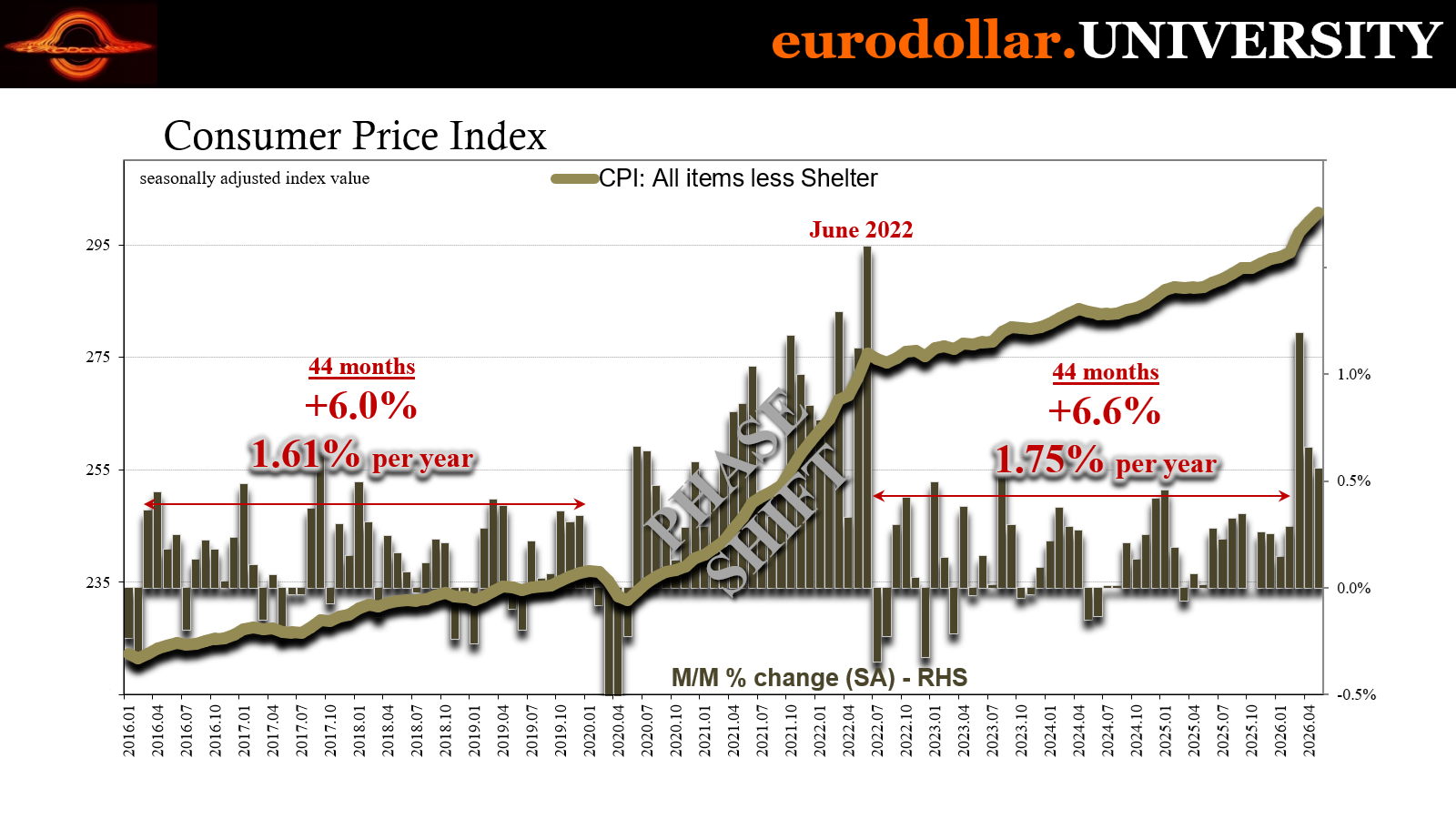

The same is unfolding the last three months. Despite that much more sizable impact from gasoline on the headline, core rates and other measures continue to show nothing apart from the continued fakery in shelter. The core CPI for April was somewhat elevated, which triggered the expected backlash and warnings. Except the May data reversed course, exposing the previous month’s acceleration as nothing more than a typical variation produced entirely by the unreliable fakery of shelter.

Stripping out shelter/OER, before the energy shock in March the entire rest of the CPI had basically matched the final years of the thoroughly disinflationary 2010s. Over the final 44 months of the decade, the CPI less shelter rose at an annualized rate of 1.61% per year. Between the end of the supply shock in mid-2022 until the start of March 2026, over those 44 months the CPI excluding shelter increased at a 1.75% per year rate.

No sticky nor tariff inflation whatsoever.

What that shows is the only post-supply shock factor producing elevated price rates in the 2020s had been shelter. Starting with March 2026, there now just two factors accelerating the consumer index are gasoline and shelter. That’s it.

The core CPI still includes those fake rents and still was tame, but when you strip out food, energy and shelter you see just how narrow the current “inflation” actually is. There are no second order effects – ZERO - three months in.

Not only that, a key reason why is critical prices within the rest of the price bucket are either close to zero or have turned negative. One of the latter, importantly, is transportation services which straight away points to the other side of higher energy costs – the demand destruction that unfortunately will keep “inflation” in check.

Turning back to the gold discussion and its signal, the fact “Iran inflation” is turning out to be a lot like “tariff inflation” helps explain what interest rates and curves are doing, meaning a limited upside to KC Jeff and therefore yields. Even if those did impact gold, with the current evidence all around the economy this cannot explain these sharply lower precious metal prices.

There is no inflation and therefore a very narrow window for any rate hikes. Exactly what the curves are pricing.

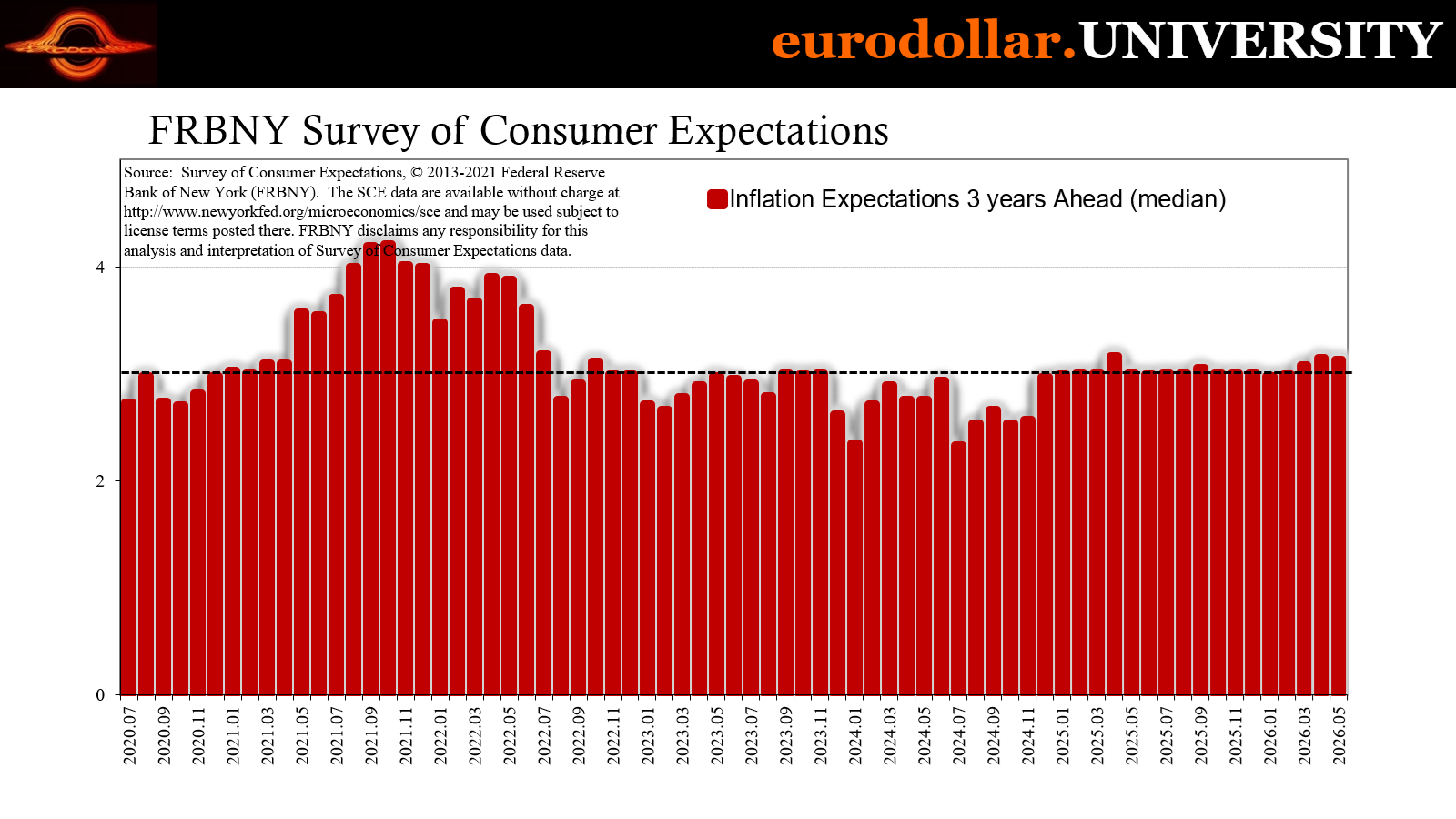

Of course, officials are also looking for the possibility consumer price expectations “unanchor”, the broader part of Economics’ absurd inflation framework. As discussed on Monday, there is also no evidence those are doing so from either consumers themselves (FRBNY) or within the Treasury market (TIPS).

There just isn’t a pathway for significantly higher rates for an extended period which might have even a small chance of justifying such a big drop in gold.

That leaves us with two remaining factors. First, the silver matter. Gold is, to some extent, caught up in the ongoing repricing of silver. Some of that is how the “other” metal had gone way too far during its supply squeeze. Another part could be related to sagging industrial demand, now or the not-too-distant future.

In the short run, it really does appear that gold is being liquidated and therefore pointing to an increasingly unstable dollar funding environment that wasn’t in a great position to begin with. As I went through in today’s YT video, this fits with the increasing desperation displayed by various governments and central banks around Asia – the same which have liquidated gold previously in response to the same problem.

Dollars, as in eurodollar.

By attempting to target a stable exchange rate, those foreign authorities are being forced to supply marginal dollars from out of their reserves. When using gold, since it isn’t money and is illiquid in large size, the effect is outsized on the price and brings all these various pieces together.

And it’s another reason why the Treasury curve has been so restrained despite the hawks and CPIs. Weak economy, classic energy shock case, plus the dollar shock which clearly comes along with it.