WOW CHINA APRIL

EDU DDA May 18, 2026

Summary: The ugliness in China was not shy for April. Retail sales the worst since lockdowns. Fixed Asset Investment re-crashed. Even industry stumbled. But was it the oil shock, or instead what bonds had been bull steepening from well before Iran? If that was the case, then the real object isn’t the confirmation of China’s resumed downfall last month, it’s more about what might be happening there this month as the deeper energy shock collides with that pre-existing fragility.

DID ONE OF XI’S UNDERLINGS RISK TELLING HIM THE TRUTH ABOUT JAN/FEB?

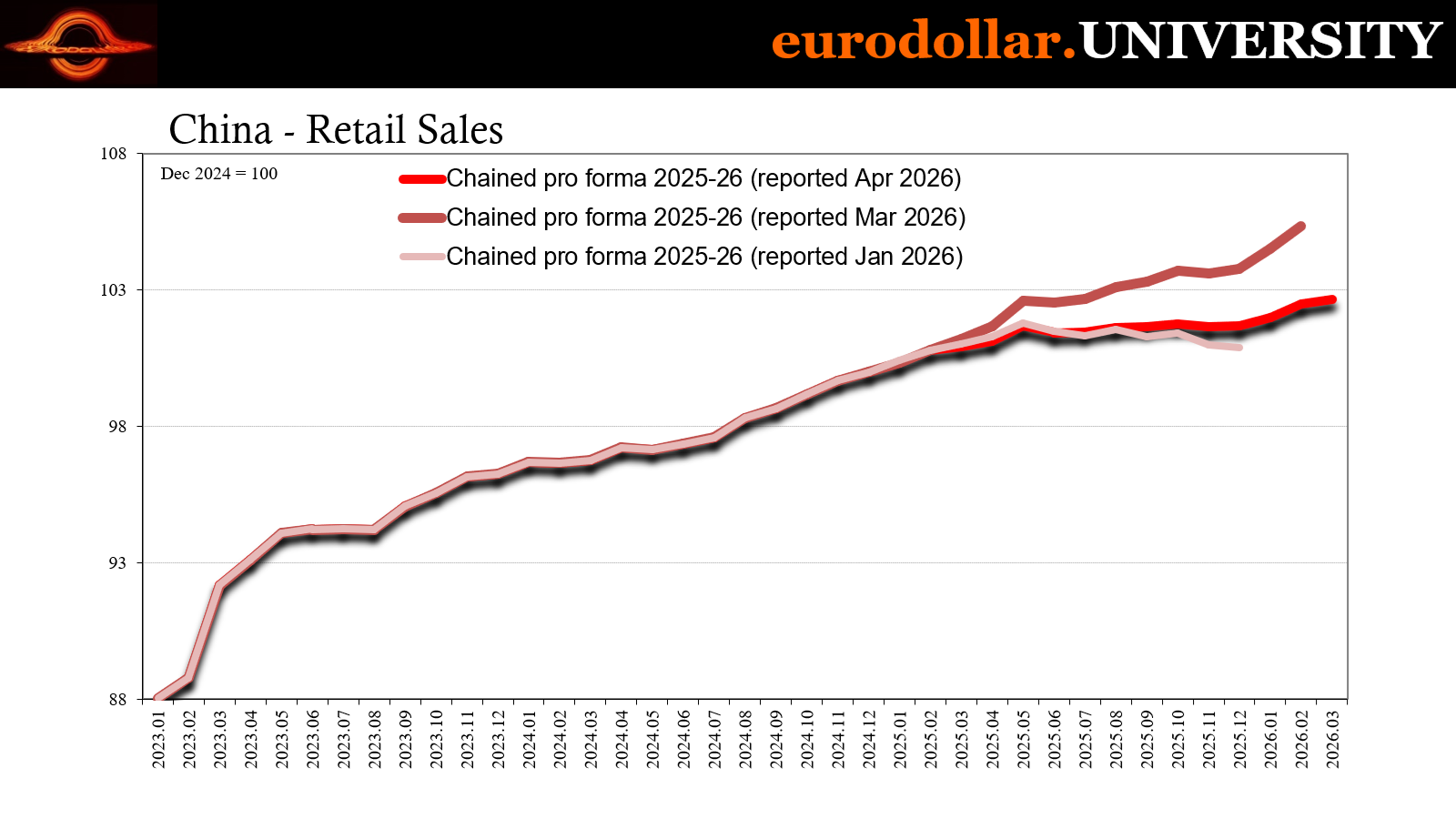

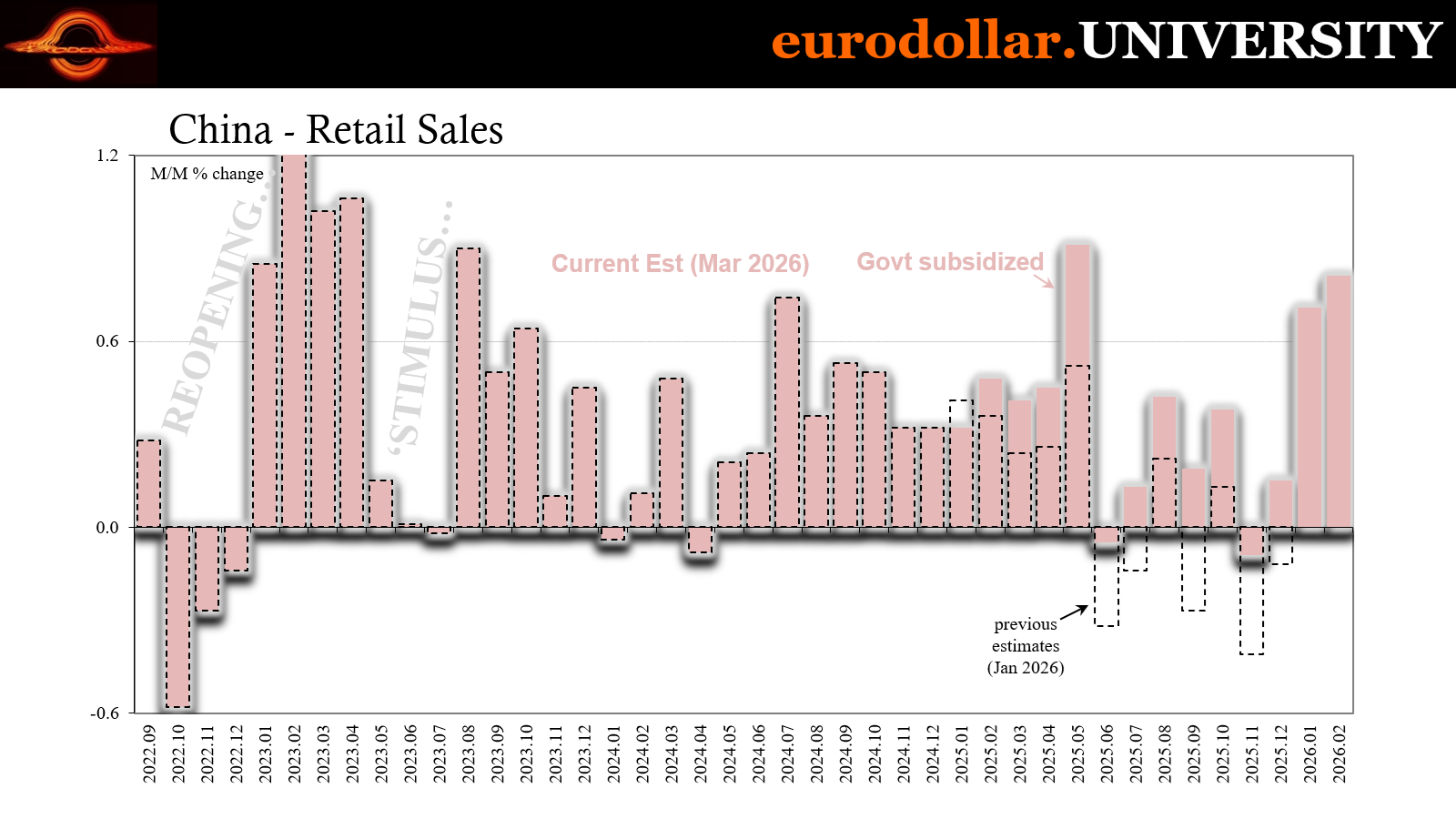

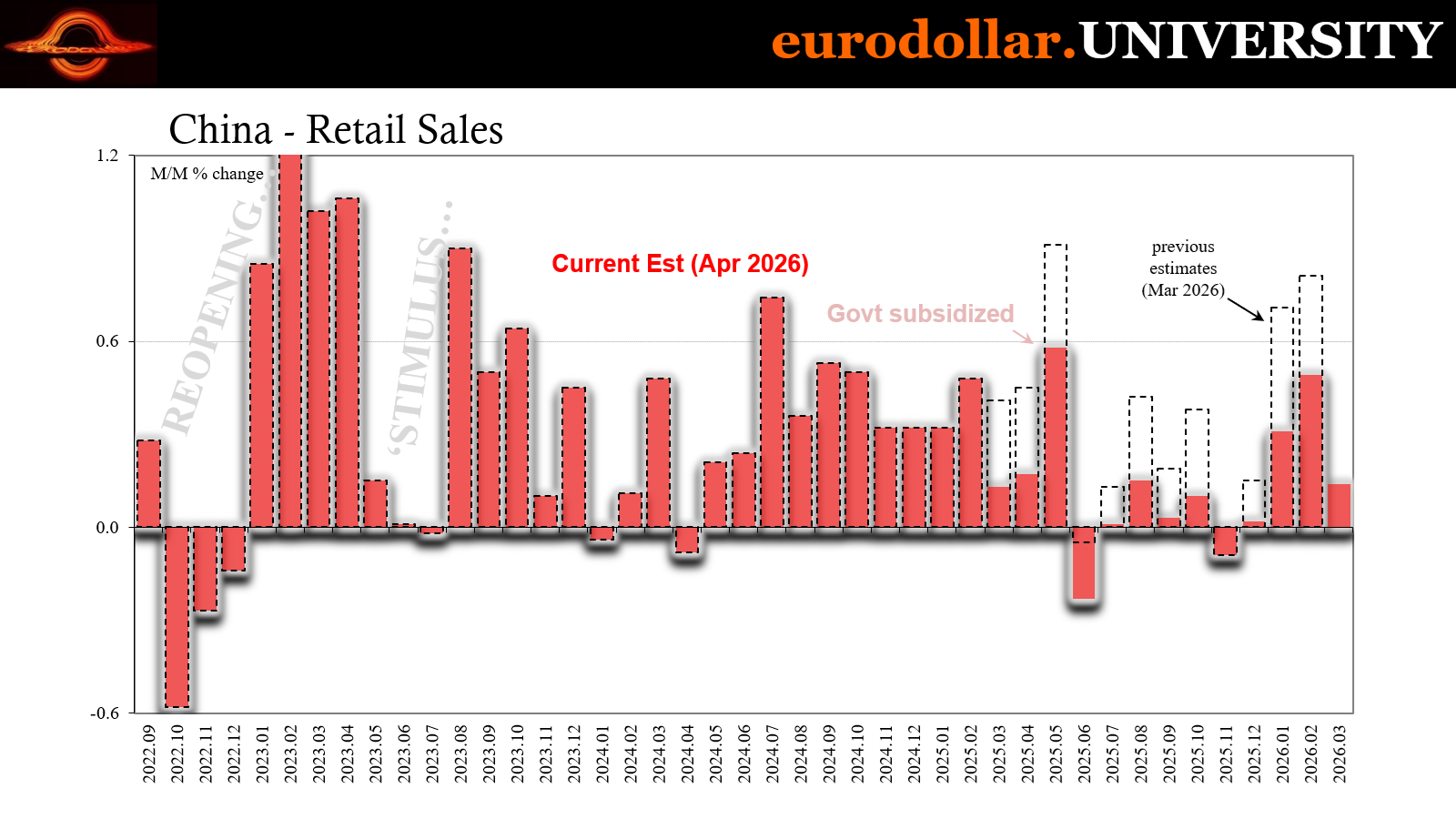

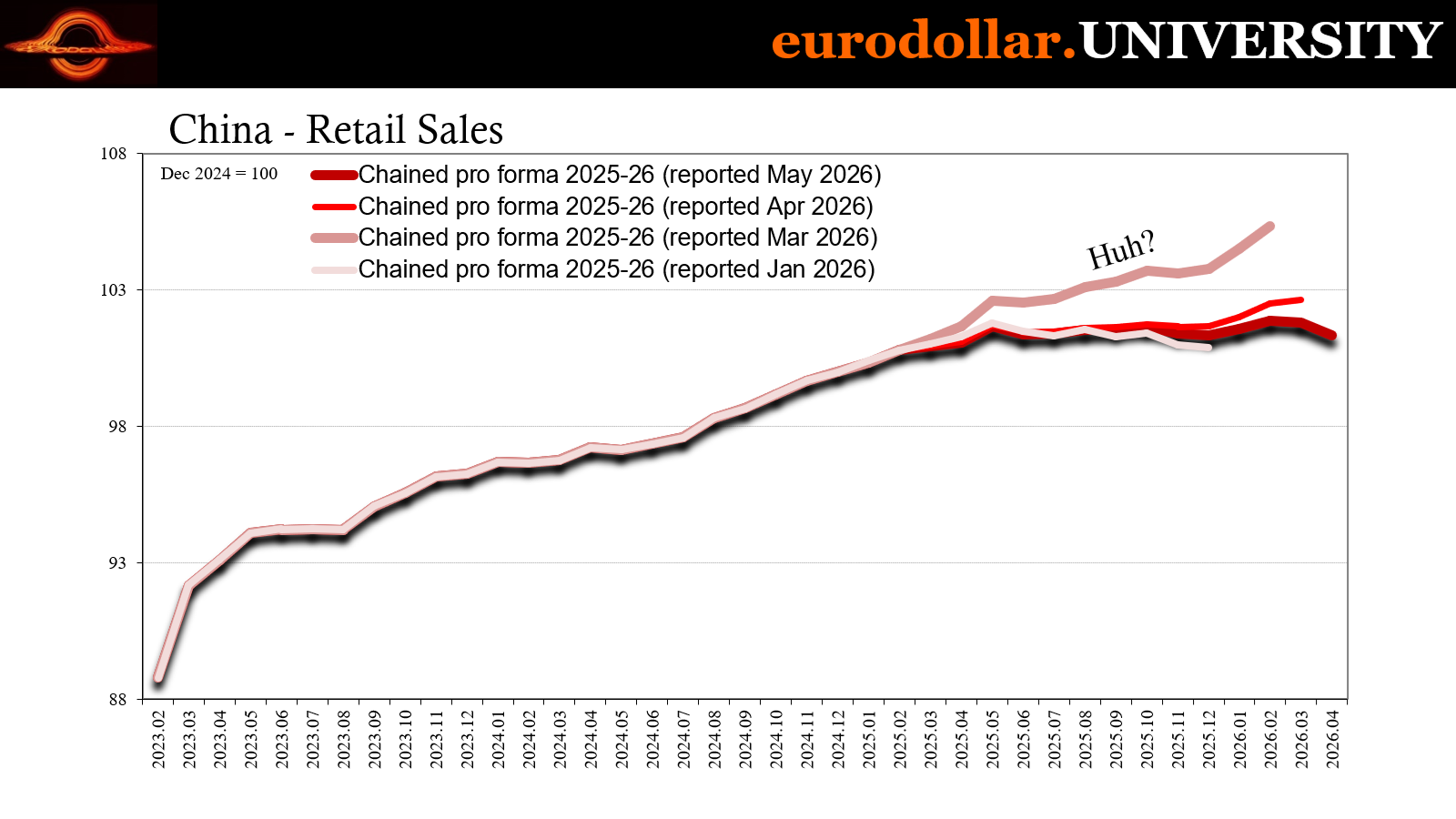

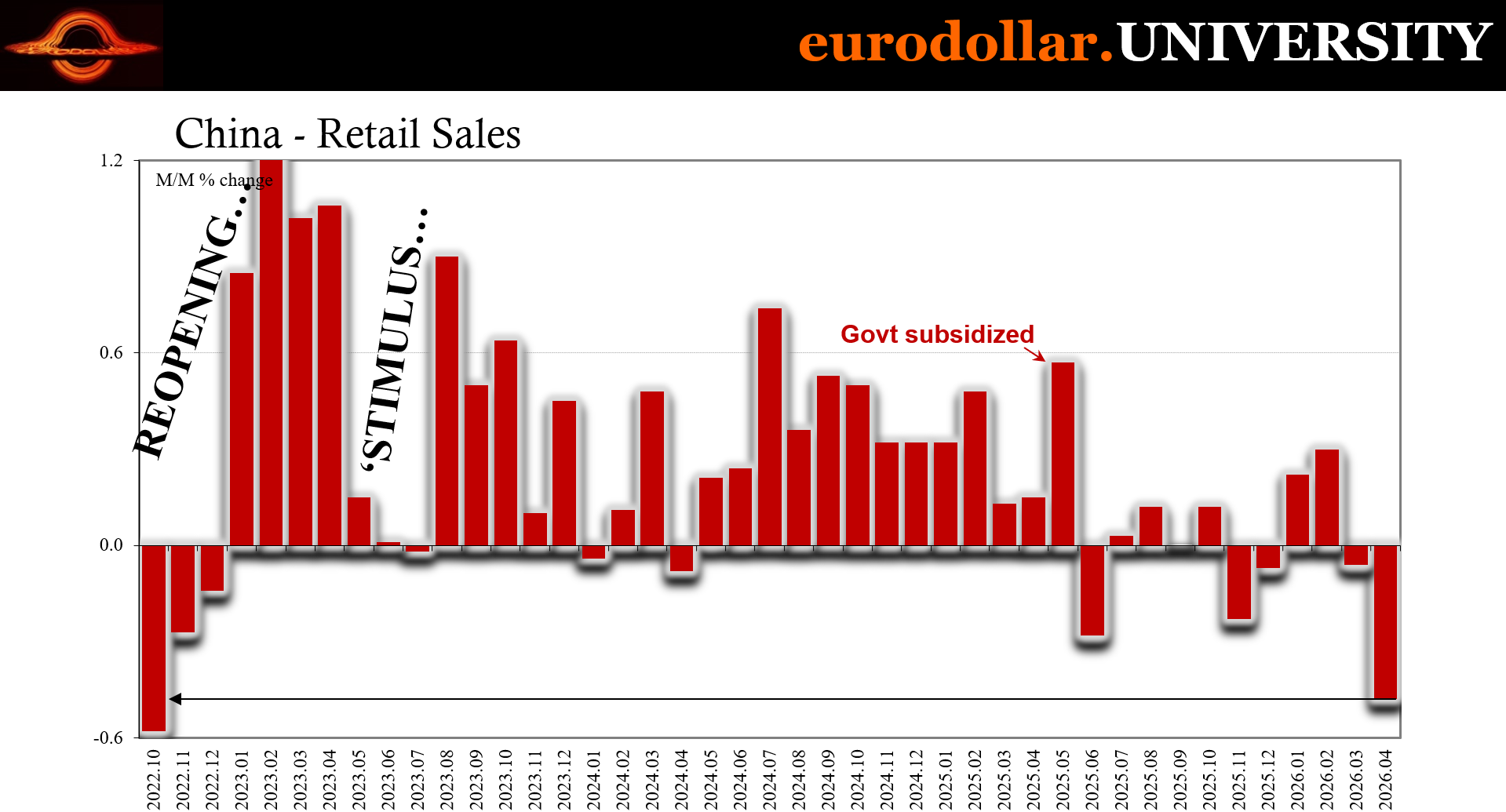

Remember China’s retail sales report from March? The one where the NBS suddenly, seemingly out of nowhere, nearly totally revised prior estimates and in the process erased most of what had been an alarming downturn? They were revised again last month basically restoring the previous downtrend. Today with the release of the April figures, that downside just got a whole lot worse.

That raises one question as a start: just who were those one-time revisions for? It’s an interesting political angle that provides maybe an indirect window into a lot more than just the worsening state of China’s economy. Some background notes to keep in your ear as we go through the cacophony of further macro and money noise.

We knew the numbers were going to be ugly, having already gone through the bank and credit reports just a few days ago. Yet, the results across the macroeconomic stats managed to outdo those: retail sales fell by the most since the lockdowns, investments re-crashed, and even industry, the lone standout, didn’t stand out last month.

China was already gripped by its own internal mess and now it appears to have been caught up in the energy shock, too. If this is a glimpse at what we’ve been cautioning about, the fragile economy from well before the Iran conflict then colliding with the fallout from it, the numbers merely confirm what we’re expecting as that paints an alarming picture.

Not surprisingly, it stunned Economists and analysts. None of them were expecting such dramatic reversals. Quite predictably, they’re all going nuts over more “stimulus”, including expectations for rate cuts. These “experts” are entirely incapable of learning; how interest rates are information, signals, not levers to be manipulated by technocrats who themselves are completely clueless.

And that may be for one or another reason.

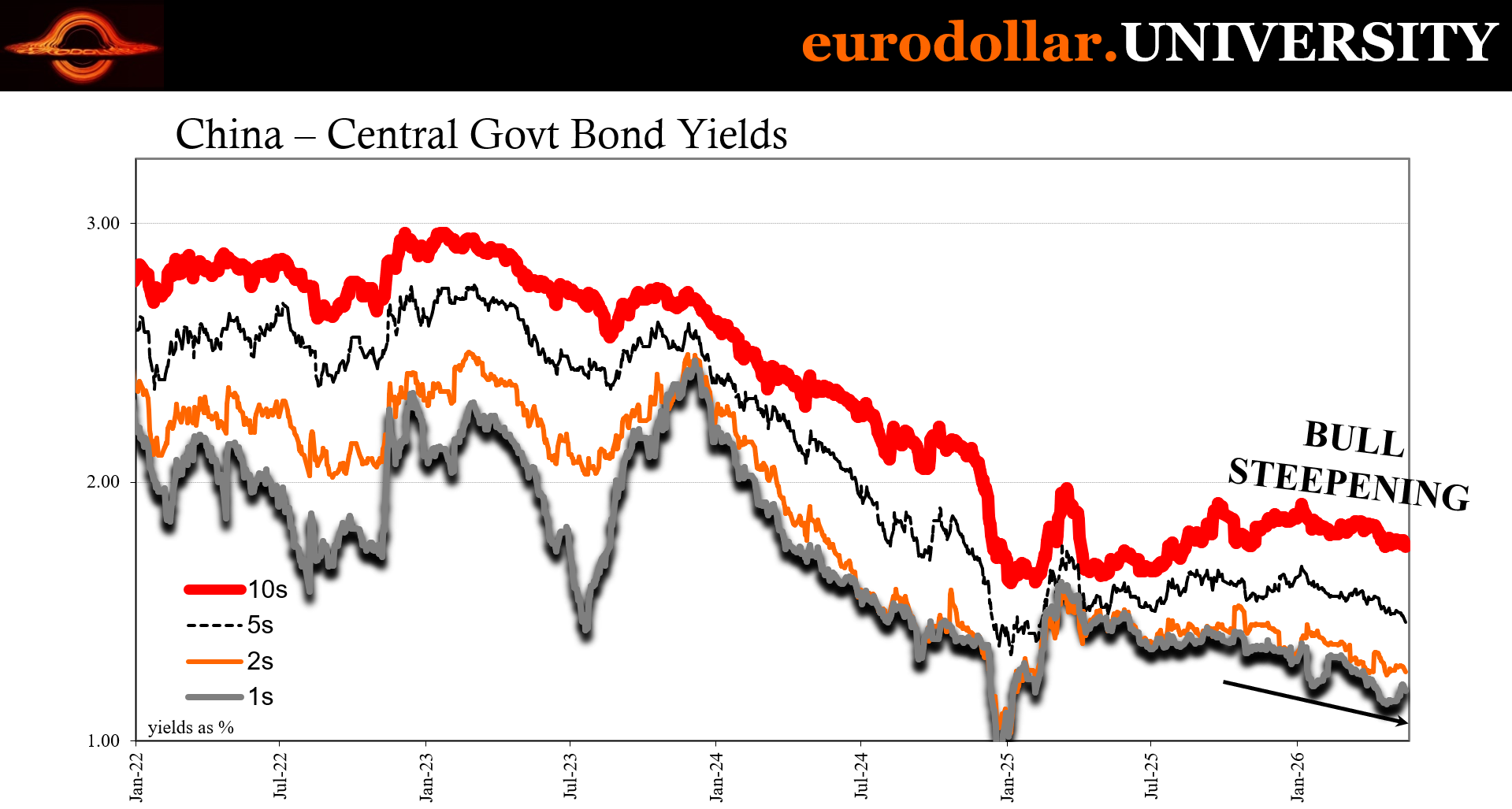

Yield the bull

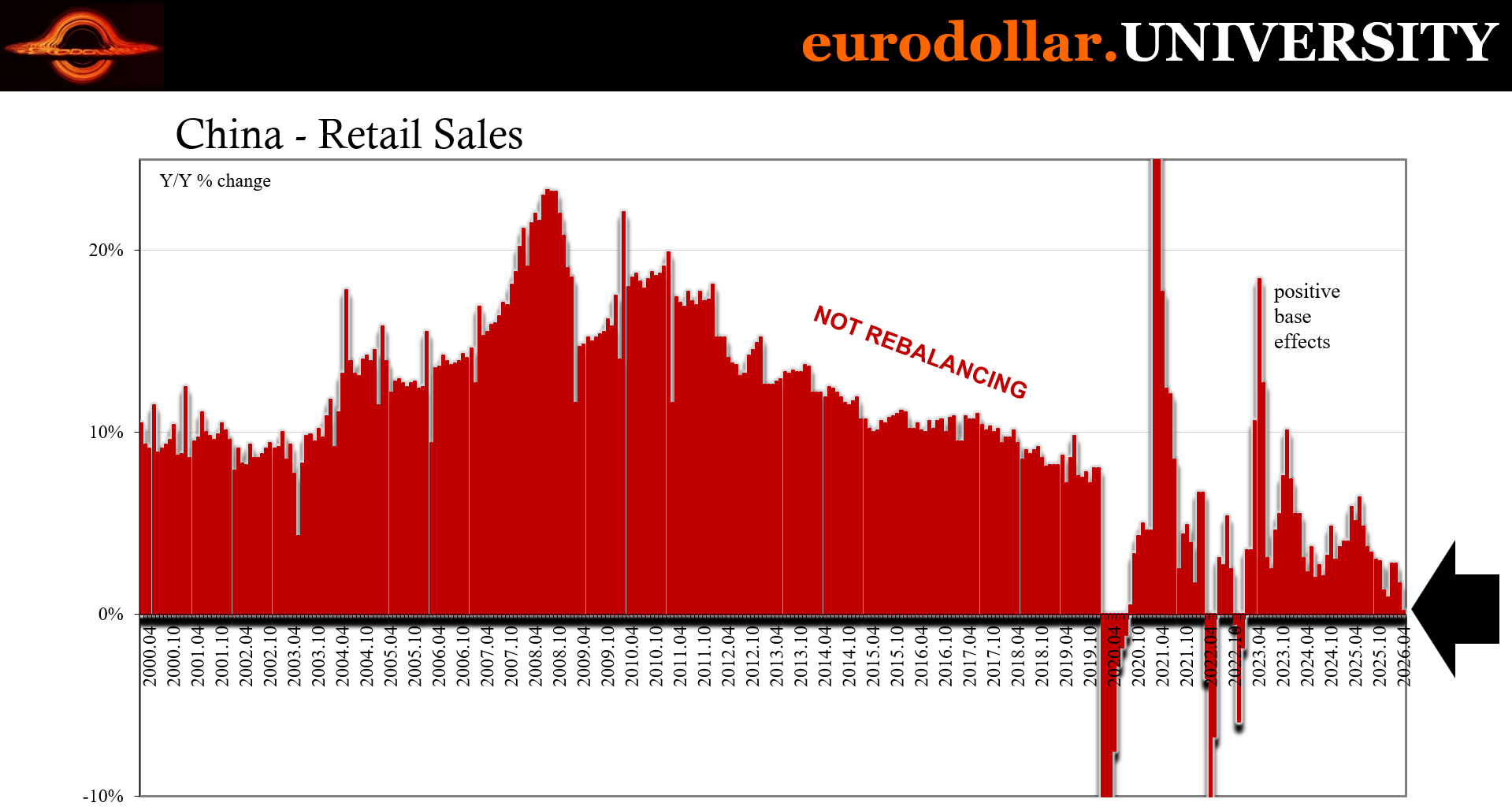

There is simply no other way to say it: Chinese consumer spending crashed in April. That was after a small drop in March. Before the past few years, outside of Zero-COVID a single negative month would have been considered unthinkable let alone two in a row. With last month’s big drop now in the books, retail sales have contracted in four out of the last six.

At least now that the downtrend has been restored in the data.

The reason for it remains the same straightforward flat Beveridge implication; though, it should be pointed out, the official unemployment rate did decline after reversing trend and rising in March when seasonality would have had it dropping. There may not be widespread layoffs, but there are the same familiar signs of globally synchronized no-hiring increasingly hard to miss.

Retail spending is one of those.

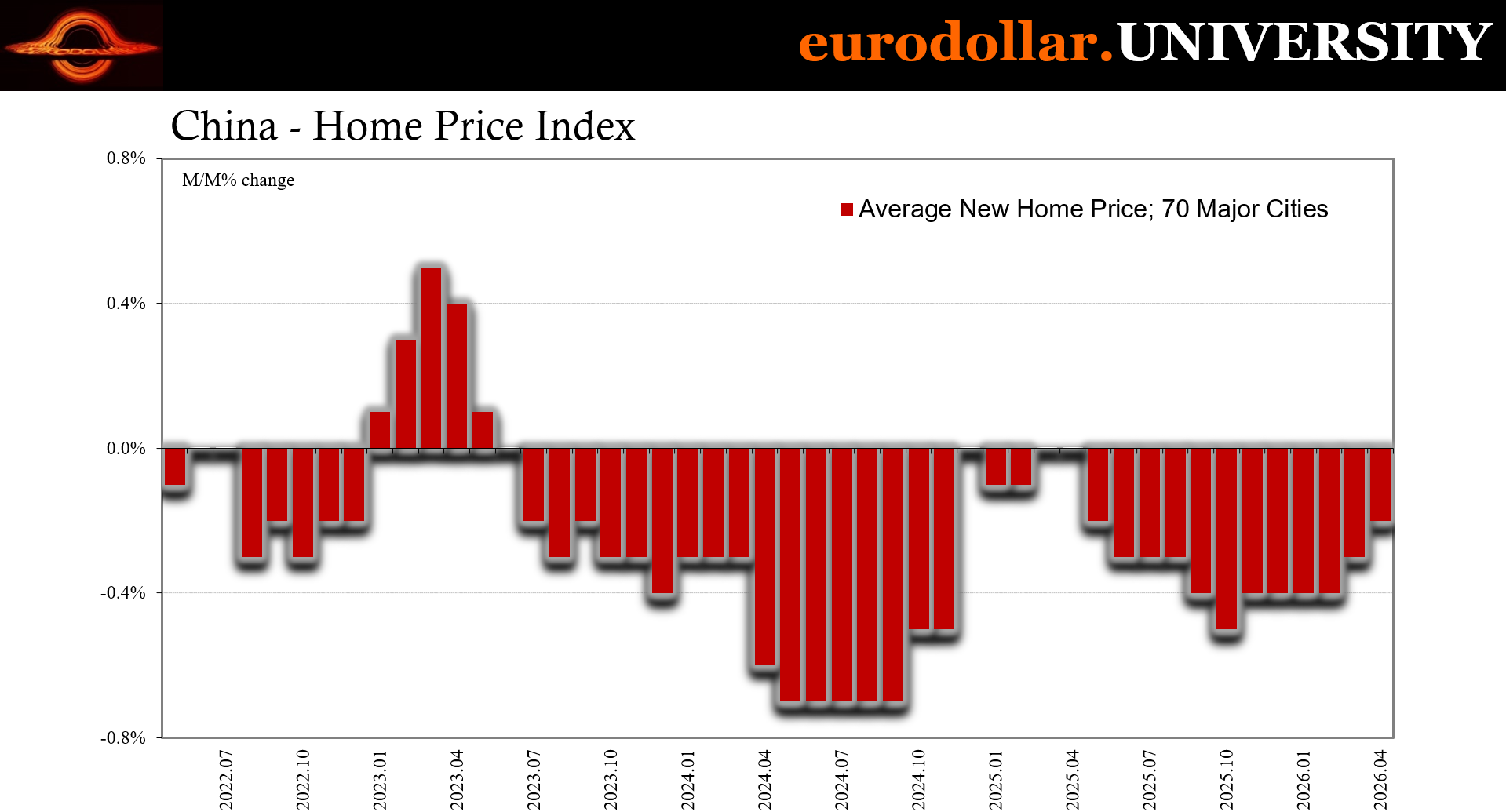

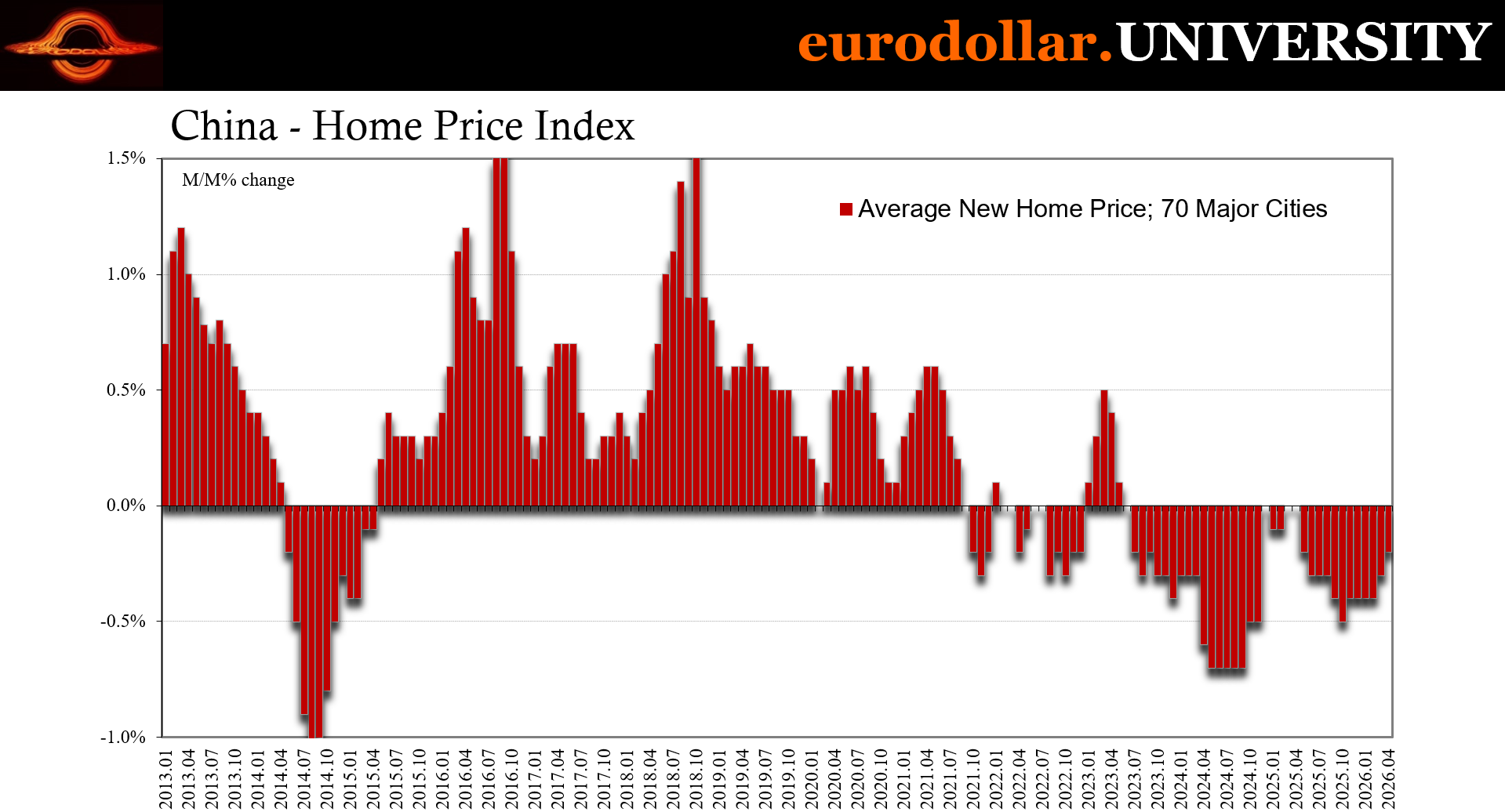

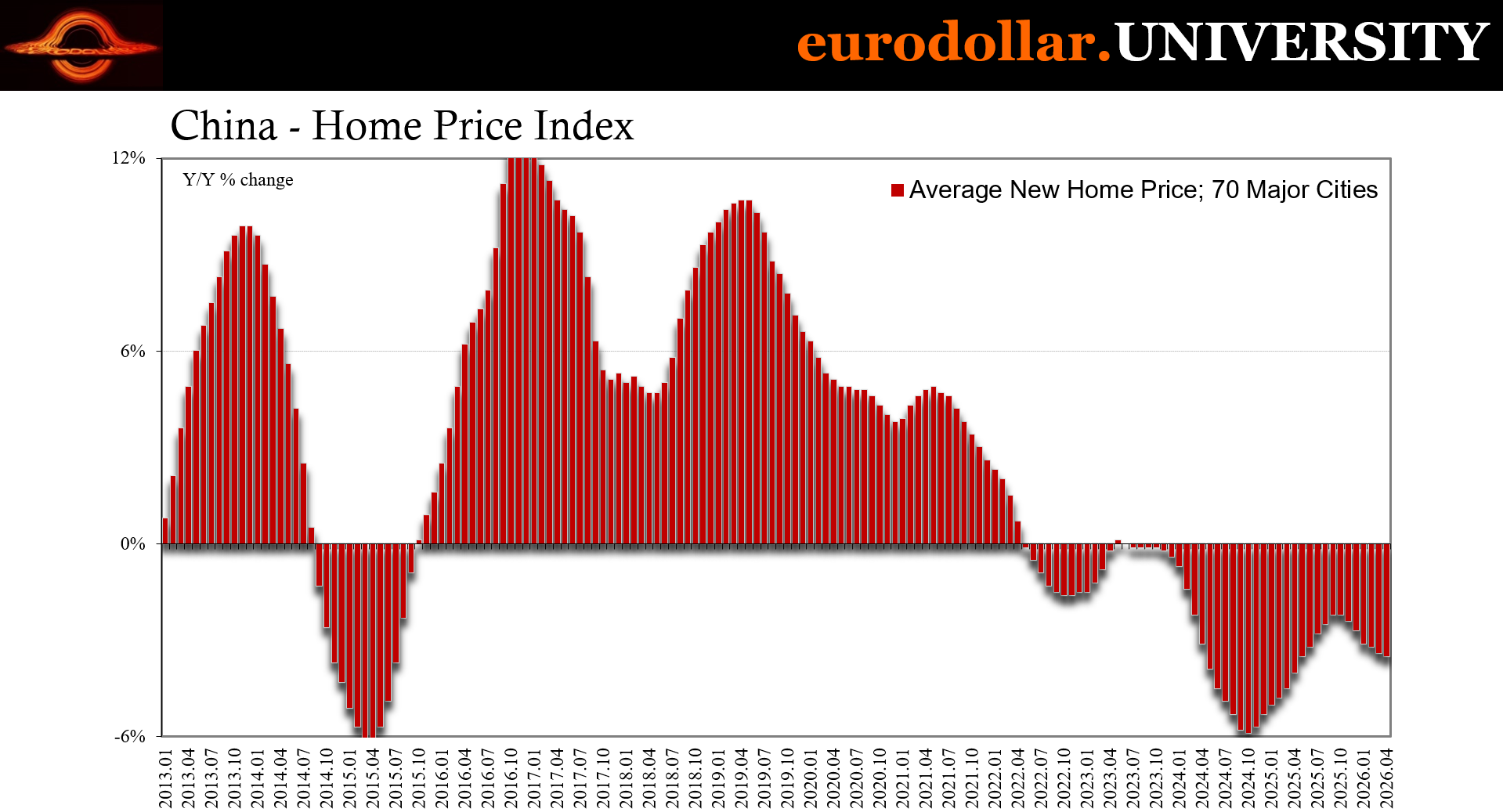

Chinese households see their employment under threat at the same time all the bazookas in the country aimed at fixing the real estate bust continue to come up short of any tangible product. Home prices fell – again – across most cities in China. The 70-city average declined another 0.2% on the month, the twelfth straight monthly drop.

In fact, the index hasn’t been positive since May 2023, experiencing only four months of zero change to count for “improvement” out of the thirty-five months since reopening fell flat. During those almost three years of constant “stimulus”, bailouts, and rescues, average home values have sunk by a whopping 11.3%.

Since most of China’s household wealth is tied up in real estate, it doesn’t take much more than common sense to see the problem. Even Economists do, too, however they believe the government – any government – possesses enormously powerful tools capable of fixing whatever it wants. Most times, we’re led to believe the only element lacking is the will to use them.

That’s why downturns are looked on favorably because if they get “bad enough” it will convince officials to dig a little deeper into their toolkit.

China’s CCP most of all, given its authoritarian makeup and therefore fewer impediments standing in the way of doing the “right thing.” All it allegedly lacks is the proper justification.

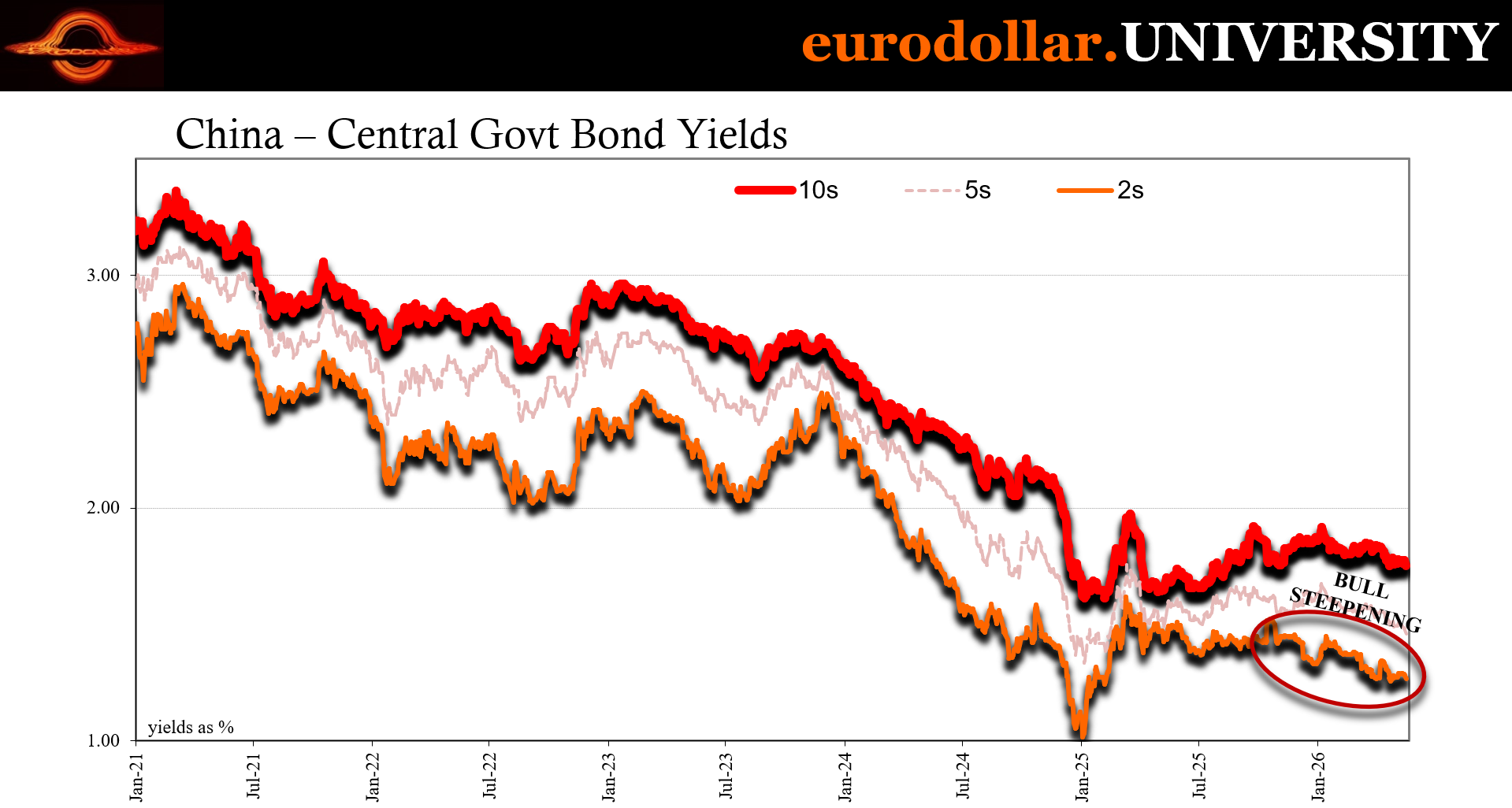

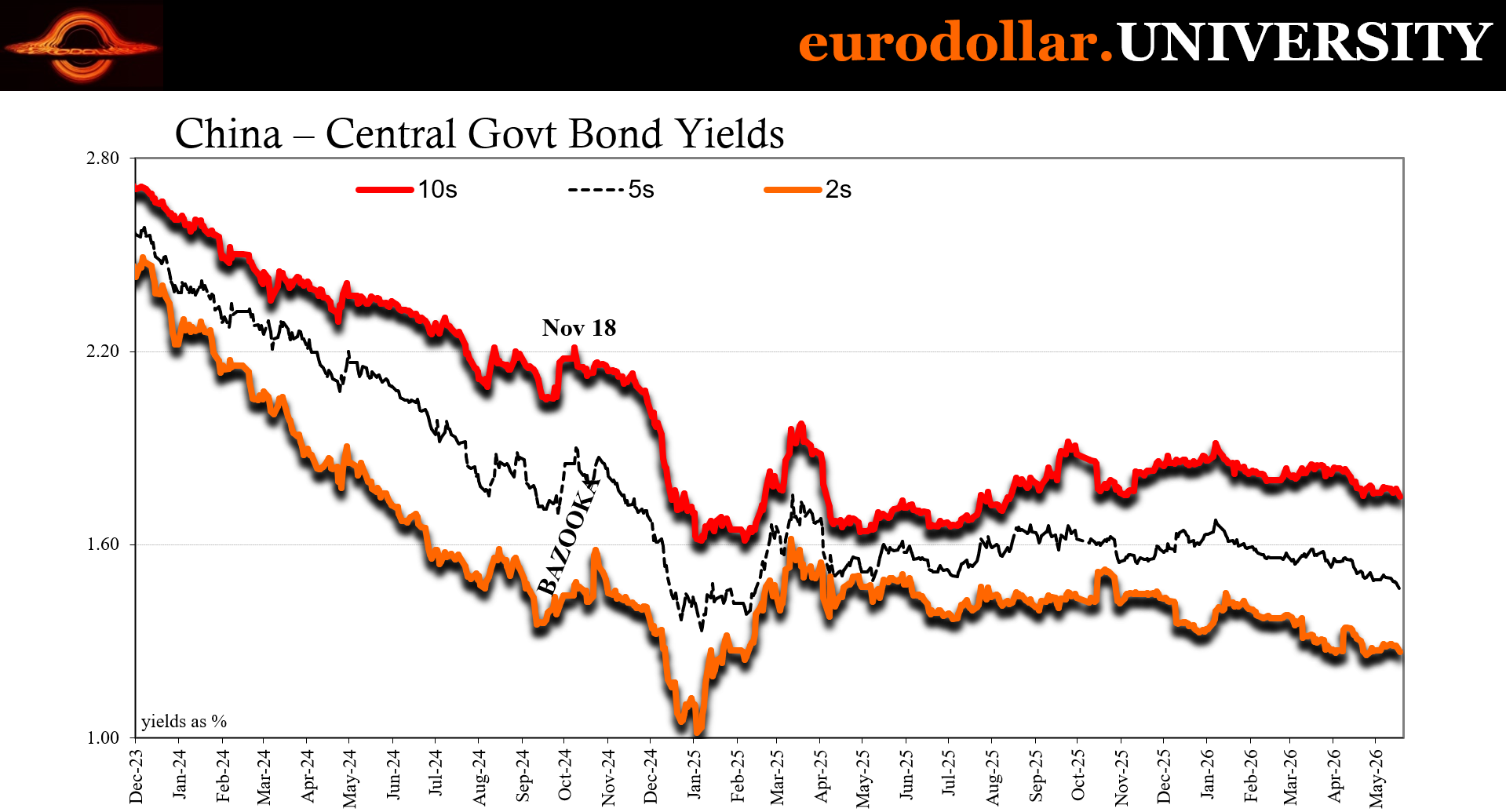

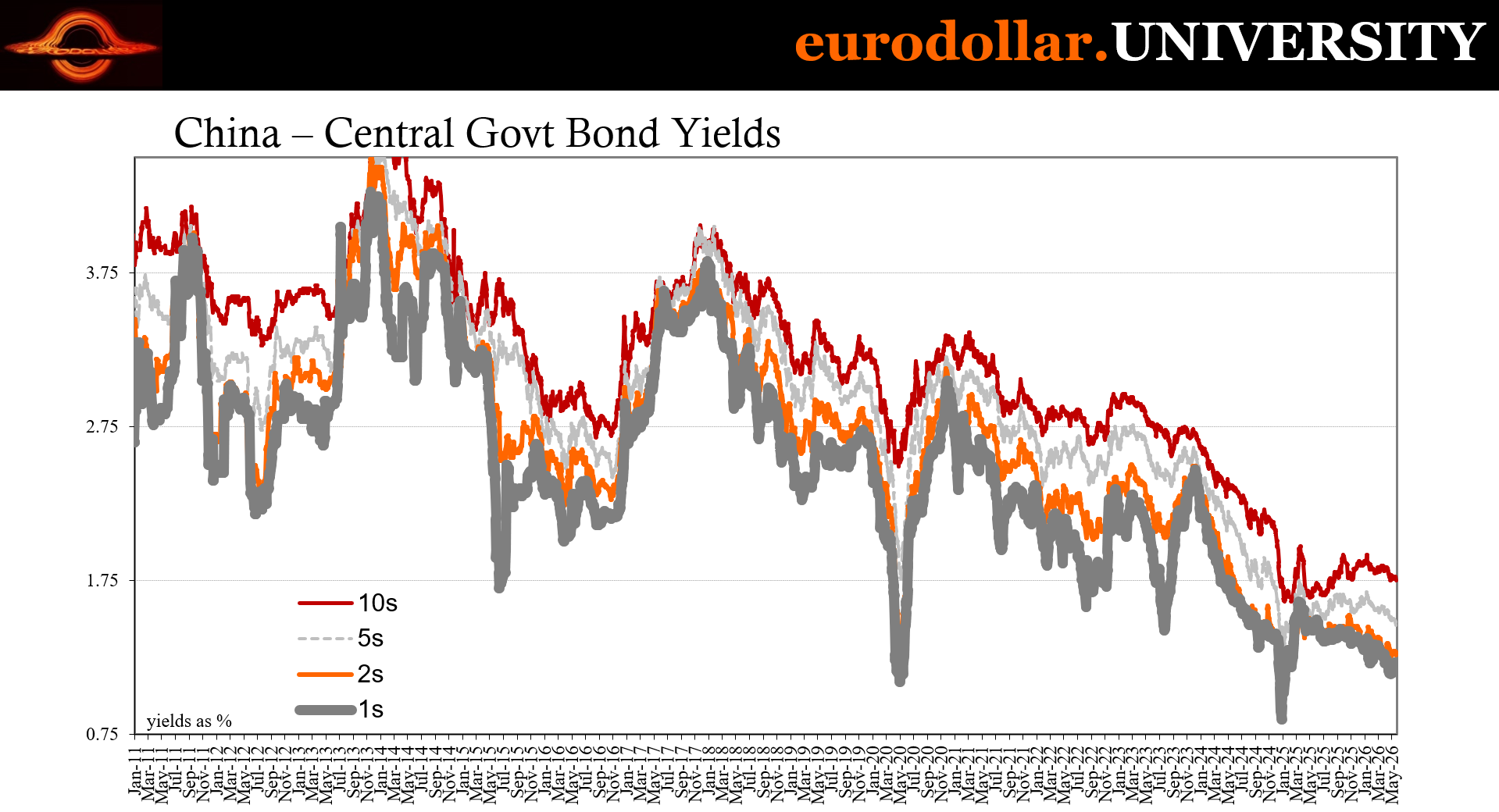

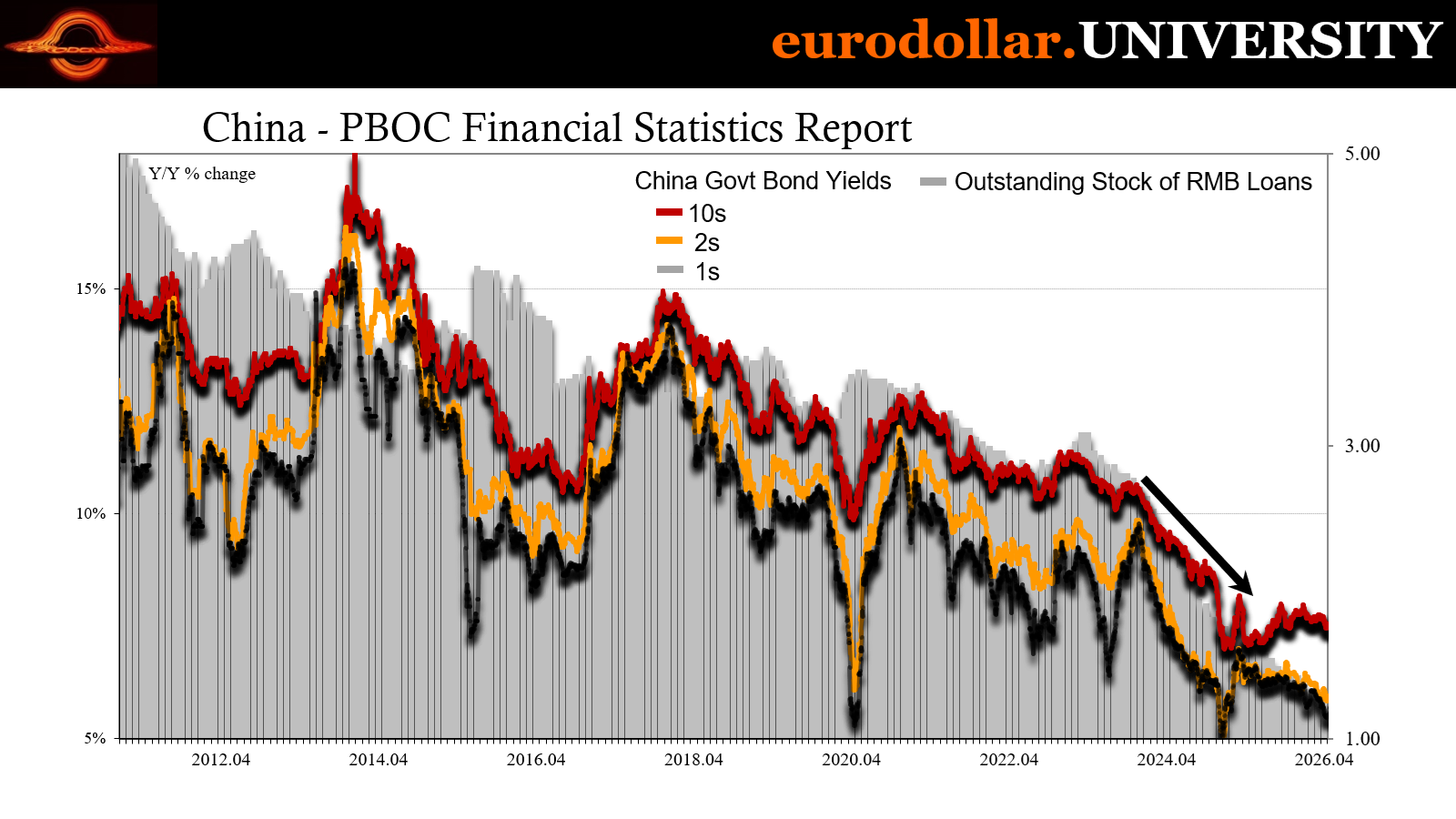

What authorities are truly missing is a grasp of basic economics, starting with using markets as sources of information. China’s bond yields, as we’ve documented the entire time, told the world not to expect success or even some organic turnaround. Rates continued to fall reaching ultra-low territory some time ago, a key signal relating to the full arrival of depression economics.

More recently, the Chinese curve has been bull steepening again to where ST rates were down at similar obscene lows comparable to late 2024 and early 2025. This was a warning that the acceleration in the downturn which began in the middle of last year had accelerated once more, taking on more concerning properties and yielding further alarming potential.

And that latest short run steepening began before the energy shock, too.

Thus, the April economic data, like the month’s bank stats, are just confirming what the bond market curves have been forewarning. China took a turn for the worse and here it is.

No one saw it coming?

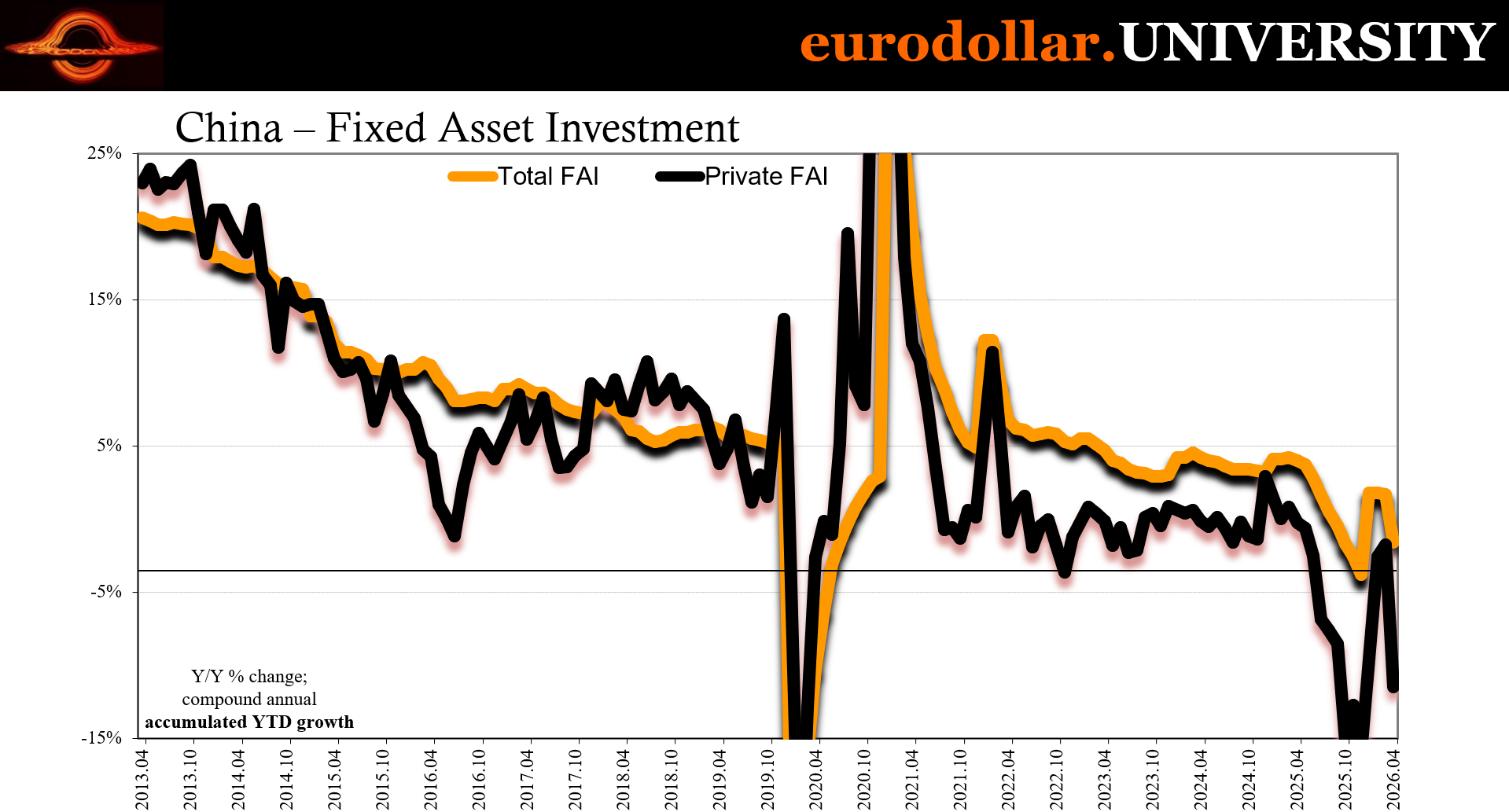

According to Bloomberg, this was completely out of left field. The decline in retail sales for April, which pulled the annual rate down to almost zero, somehow wholly “unexpected.” These are already lockdown-like results. Fixed Asset Investment, that had been crashing to end last year only to rebound at the start of this one, crashed all over again.

Now industry is being starved of fuel – literally.

Yet, we’re told this:

Not a single economist surveyed by Bloomberg had predicted as pessimistic a reading for industry, retail sales and investment. The disappointing performance of the world’s second-biggest economy last month is a reminder of its domestic vulnerabilities, after a global artificial intelligence investment boom sent trade soaring.

And that’s the warning for everyone else outside China. Analysts like central bankers are all thinking resilient economy therefore oil will be inflationary (that’s not how it works anyway), so fragility wasn’t in any of their models and forecasts. This goes well beyond “disappointing performance.”

SURE, NOTHING THE NEXT FAILED 'STIMULUS’ CAN’T FIX…

Categorically incorrect, and not just where it comes to the Chinese predicament.

It wasn’t unexpected because bond bull steepening reflected the basic economics of common sense, one which completely discounts “stimulus” whereas mainstream commentary can’t ever get away from it. This is one of the stupidest aspects to Economics (capital “E”) demonstrating how it is ideology not a true scientific discipline.

The data “should keep PBOC easing – RRR and even rate cuts – firmly on the table, while fiscal top-up may come later,” Societe Generale economists including Wei Yao wrote in a note.

No matter how many times we’re told stimulus stimulates and then empirically the results always prove it didn’t, they line up to extol the virtues of the next stimulus and how it will stimulate somehow anyway. There is no falsification for Economists, only ever tomorrow’s next great idea.

They all went crazy over the bazooka. China is coming up on two years since then and absolutely nothing to show for it. Instead, what was supposed to be the biggest thing since 2009 has been completely written out of recent history. It’s like it never happened even though, in practice, the whole thing ended up being yet another datapoint proving very little of Economics is valid.

You do have to wonder how much higher authorities in China might know this. Again, thinking back to the retail sales revisions from a couple months ago, as we pointed out at the time and then a month later when everything was changed back, there didn’t seem to be any obvious reason why the NBS would just outright fake the numbers.

Though that part is clear; they absolutely did fake them.

The timing was the only real clue, meaning just in time for the National Peoples’ Congress (NPC). It was the same gathering when top Communist officials were debating the next Five-Year Plan for China’s economy. It was also when authorities came out of it (sounding) confident about the situation in 2026, despite still lowering their official GDP target to a range of 4.5% to 5.0%.

Fake retail sales data along with what sure appears to have been artificial activity in industry and spending for January and February propped up the real economy (to a degree) and the data so as to make it seem such goals were easily achievable. With those short run results, the situation didn’t look to have deteriorated as extremely as it had been leaning during the months leading up to this fiasco.

The question then is, why?

Are lower-level bureaucrats and Party officials covering up the degree of downside in order to avoid repercussions, starting with maybe Xi’s purge-y wrath? If so, that raises even more questions about what the very top of the Party might really believe as far as what the true picture of China’s economy really is. Does this imply a rift, maybe a big one, in the government?

We don’t have any answers, only intriguing – perhaps worrisome - implications. There aren’t many other ways to interpret what appears to have been a concerted effort to fake stability on at least two fronts timed for only the NPC. That is yet another factor to keep in mind for the remainder of this year, as well as considering fragility with the bulk of the energy shock still coming.

Investments, too

One of the more extreme results during China’s difficult second half to 2025 was the abrupt crash in fixed investment. Given the data, yes, crash does apply. Total FAI was modestly positive earlier last year, then began to fall off a cliff by summer. Economists were, as usual, perplexed yet confident despite having no answers (as usual) for what was going on.

Without any basis for it, they all assumed it was just a blip. After all, the rest of the world was picking up; or so they all thought.

By December, FAI was falling at nearly a 4% rate with private investment down at more than 6% (accumulated). Looking at the monthly rather than YTD statistics, private FAI in the second half of the year was crashing at rates comparable to only 2020.

It turned around – not all the way – in January and February, spilling over to an extent in March. As of April, the complete wipeout returned as if the short run burst of spending from mainly the state-owned sector was only intended to be just that. It was just enough to reverse the sharp crash seemingly in time for the NPC.

Once the Party gathering was wrapped up, the numbers have gone straight back to ultra-ugly again. For April, total FAI flipped from an accumulated +1.7% through March to -1.6%. That’s a huge – suspicious - reversal.

Private FAI on a monthly basis, which was still down in the first few months of 2026 though at low single-digit rates, just utterly collapsed last month. It reversed by 11.5% year-over-year in April, seemingly a stunning turnaround if you believed in January and February while paying no mind to bulls in bonds.

Or banks.

We do have to consider the energy shock itself, though not necessarily purely the price of petroleum, not for the Chinese. The government has been demanding cutbacks on various goods, starting with refined petrol products. More recently, it isn’t even Beijing; with Hormuz still effectively shuttered, inventories being wound down, and emergency workarounds reaching their limits, feedstock is getting low.

That means literal demand destruction in this case:

Plunging crude imports forced Chinese oil processors to sharply reduce output last month, with runs in the state-owned sector dropping to multiyear lows.

Refiners are feeling the pinch after the near-halt to shipments through the Strait of Hormuz choked a vital channel for crude. The country processed 54.65 million tons of oil in April, 11% less than March and 5.8% lower than the previous year, the statistics bureau said on Monday.

Is that enough to account for the awful FAI numbers in April? Most likely no, but it might have had some initially negative effect. More relevant is what it means looking ahead. In other words, April was bad on its own in terms of re-establishing pre-conflict fragility and then here in May that puts everything together with demand destruction wrought by the shock, and not only of the direct variety.

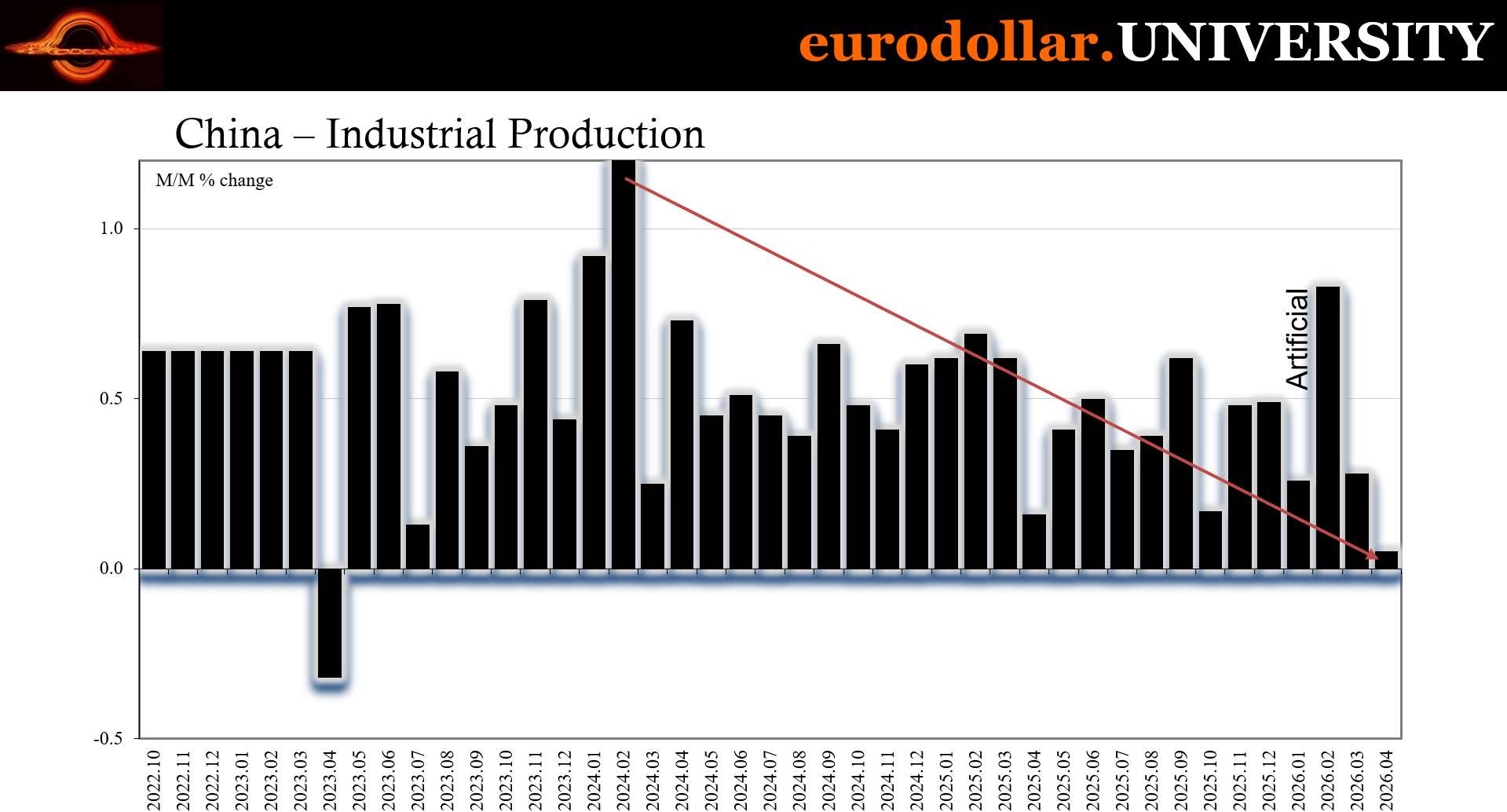

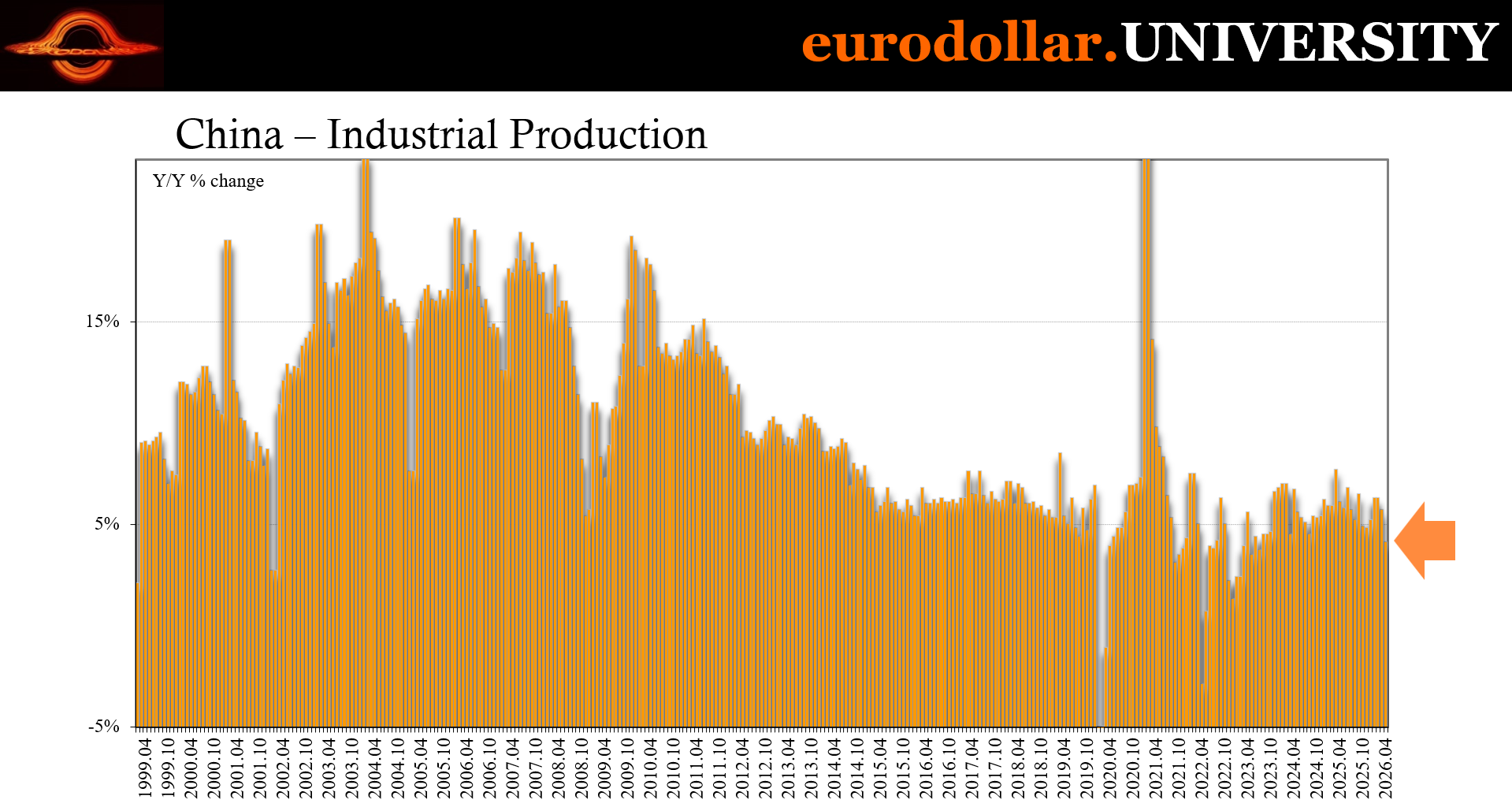

Even Chinese industry nearly took a full step back last month. Industrial production produced the final “surprise” for Economists because it had been the one sector where activity wasn’t a complete disaster. IP had remained relatively steady even as the internal economy tailed off sharply, owing to the government’s strategy of flooding the world with all the excess production China could sell.

IP was nearly flat for April, having slowed already in March from February’s (questionable?) torrid pace. With the latest stumble, the yearly rate dipped to 4.1%, down from 5.7% previously now at the lowest since the middle of 2023; though, admittedly, there isn’t much difference between April 2026 and some of the other months in the low 4s along the way.

Either way, Chinese industry also took a hit last month, a major drop off in the one area that was functionally closer to working than all the rest of China’s dissembling parts.

And we’re supposed to be assured by the prospects for even more “stimulus” from a government which may not fully appreciate the downside therefore the danger the economy is already facing before getting to energy shortages and a full global fallout from Iran.

Economists do hold to a very strange religion, with all its various superstitions.

You can see why bull steepening has come back in a big way, not that it really went anywhere last year to begin with. The curve had been more the same steepening as the rest of the world’s government debt curves in 2025, where LT rates were modestly higher though never meaningfully so. During the final quarter of last year, the bulls came back and then fully charged into the market by mid-January.

What has come up since is nothing more than confirming why that had been.

When the PBOC tried to get banks and financial firms out of bonds in 2024, the market completely ignored authorities. Now in full view of the bazooka which soon followed and did nothing, you can see why.

And that matters every bit as 2026 displays the increasing fragility in China as elsewhere. Now that difficult situation becomes worse as oil shortages begin to plague industry just as much as weak fundamentals have. Chinese households, already normalized to seeing their savings decline with every downtick in the 70-city average, cut back that much more reasonably worried about jobs and incomes.

Banks really did not want to lend in April. We once again see clearly why.

But all that has happened recently with banks and within bonds, it’s not entirely or all that much about just April. It’s where everything goes once oil and fragility collide.