SAHM IN PLAIN SIGHT

EDU DDA May 8, 2026

Summary: Payrolls for April are in and they are entirely too familiar. Because this isn’t about payrolls in April, it’s jobs, data, credit bust, Japanese trades and US consumers steadily since Sahm’s summer of ‘24. There has been a hidden recession hiding in plain sight covered up by a single number. Just one. Its corruption has allowed misdirection to go unchallenged at least in the mainstream. However, whether they know it individually or not, Americans (and Canadians) weren’t fooled. They aren’t now about where all this is still going.

Whirlpool said earlier this week that the appliance industry is already experiencing contraction on a scale equal to 2008 and 2009, over and above what had been seen during more typical recession. The CEO of Heinz said of consumers:

They’re literally running out of money at the end of the month. We’re seeing negative cash flows in the lower-income brackets where they’re dipping into savings.

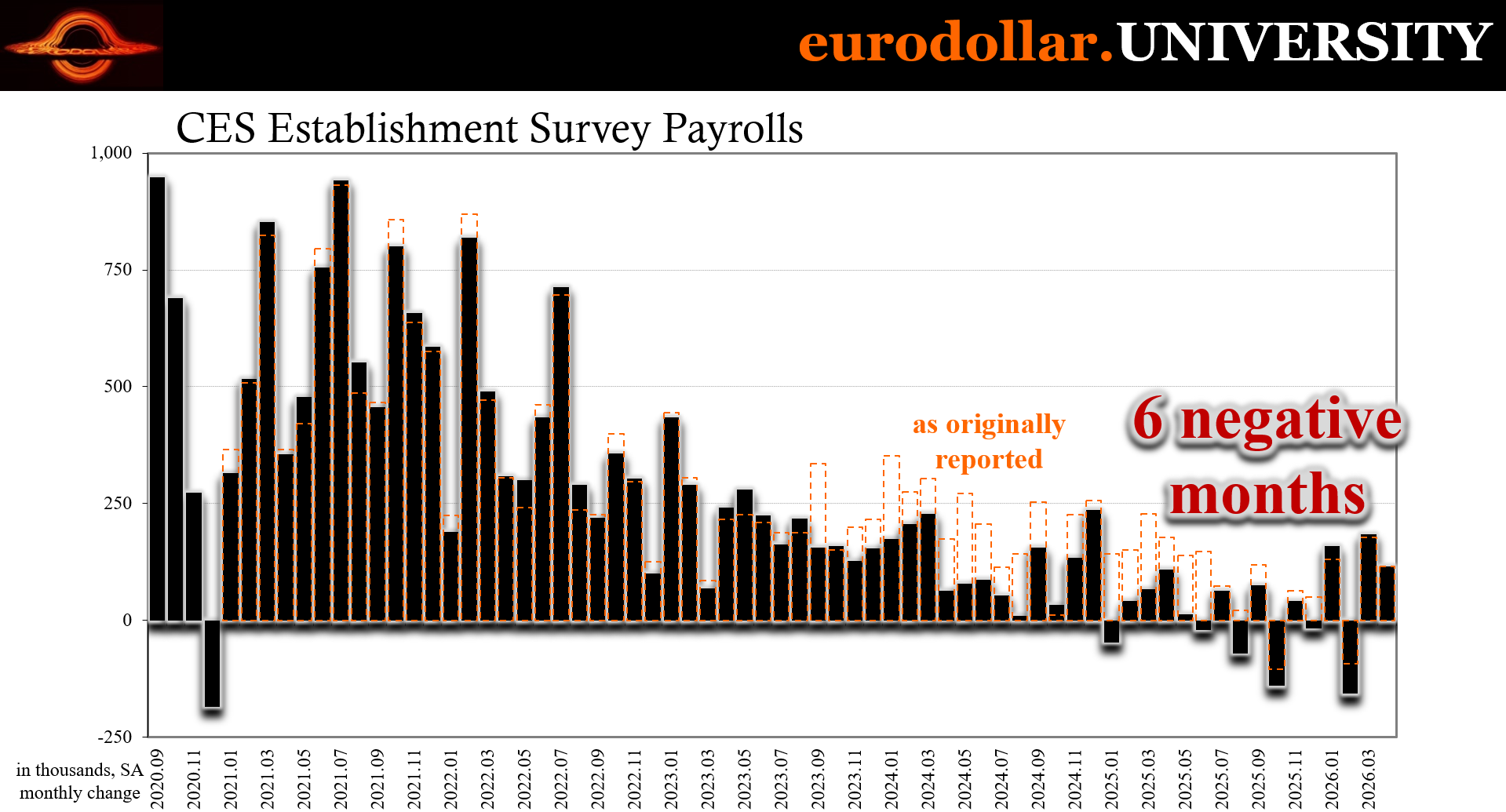

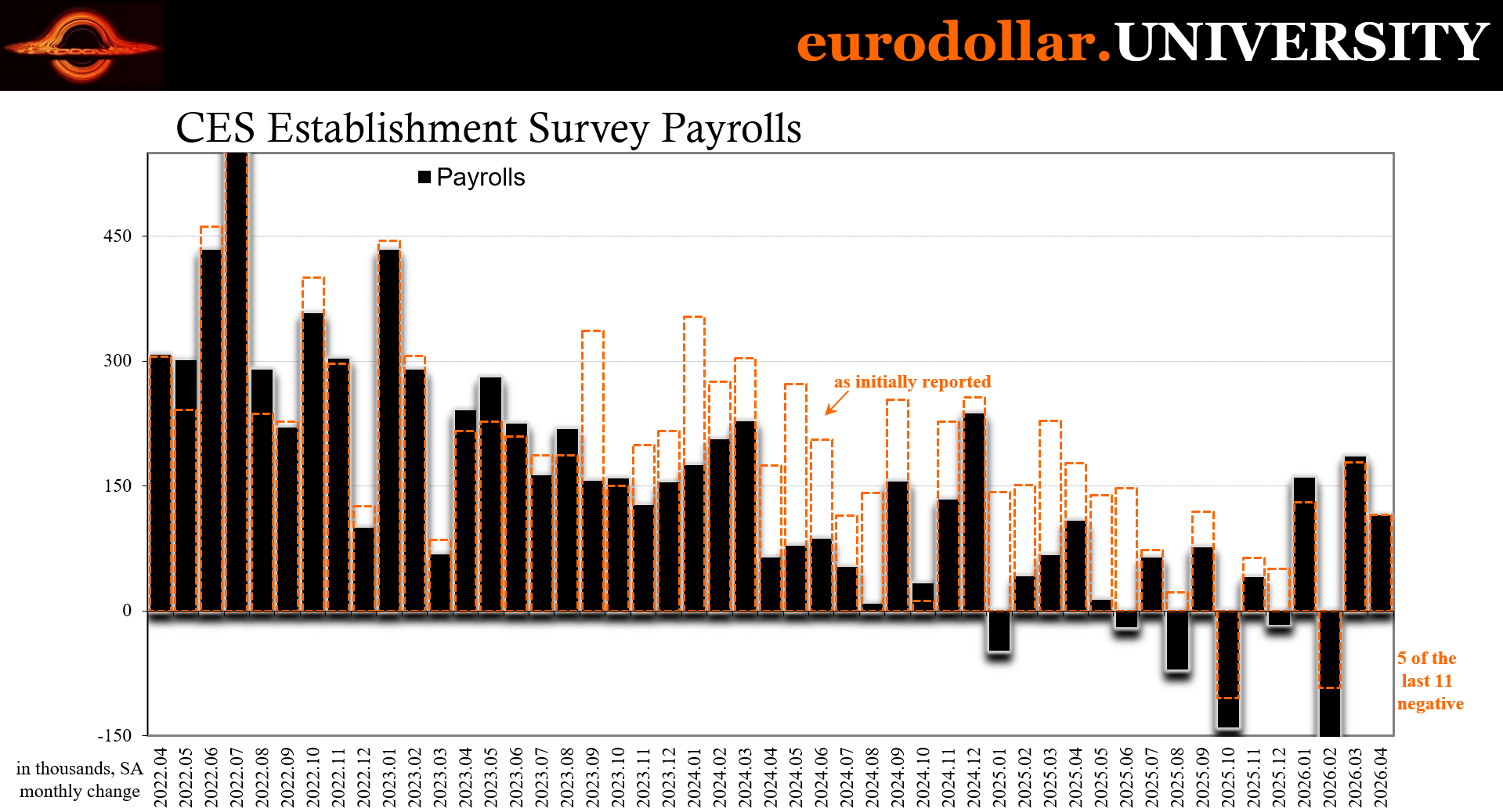

As they grapple with looming $5 gasoline, the job market is doing them no favors. Yes, the headline Establishment Survey for April did what the headline Establishment Survey has been doing for years now. Its latest figure handily beat expectations, but even so 115,000 isn’t something to celebrate. The fact it is being lauded (especially within stock indexes) shows just how much everyone has been normalized to flat Beveridge.

Or haven’t realized that’s where we all are.

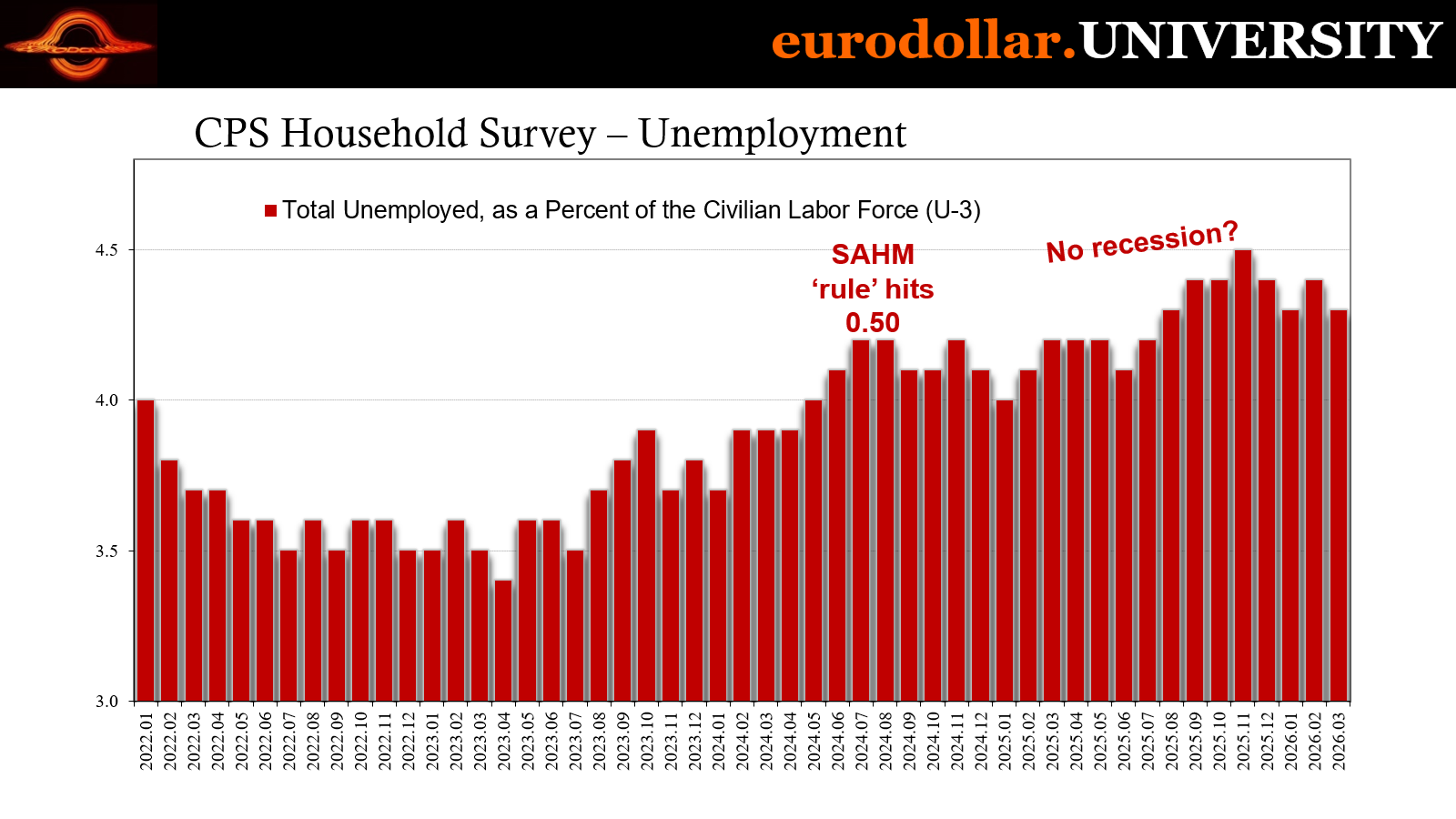

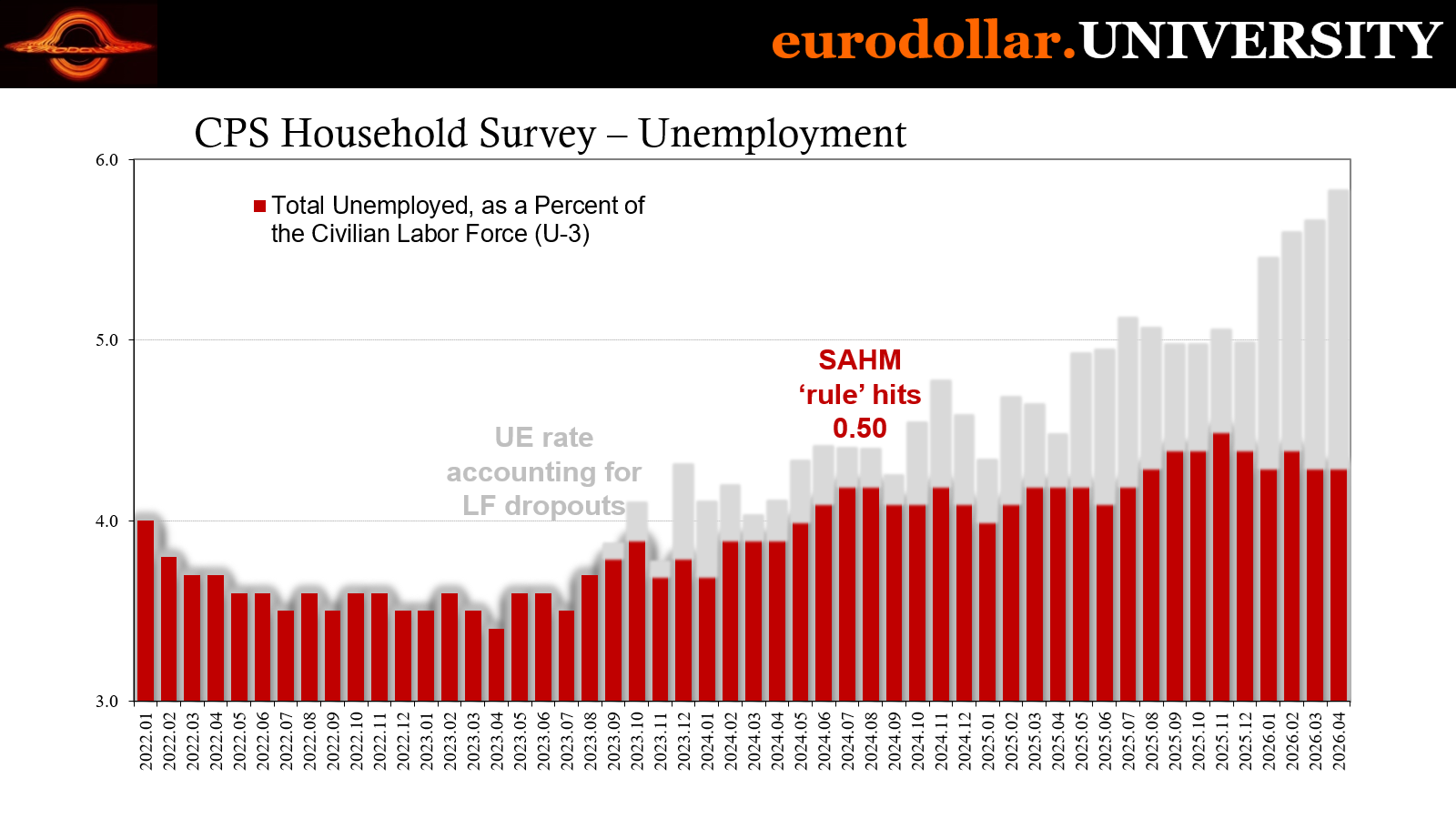

Another all-too-common occurrence, the Household Survey looks very different from the CES side. Employment dropped yet again, third straight month, as more former workers slipped right out of the labor force. It allowed the official unemployment rate to steady at 4.3%, but when accounting for dropouts the “true” rate is more like 5.8%.

IF THE JOB MARKET IS PICKING UP EVEN MODESTLY AS THE EST SURVEY MIGHT MAKE IT SEEM, WHY ARE LABOR FORCE DROPOUTS SURGING AGAIN IN 2026? WHICH ONE IS MORE ACCURATE AND MORE CONSISTENT WITH ALL THE OTHER EVIDENCE?

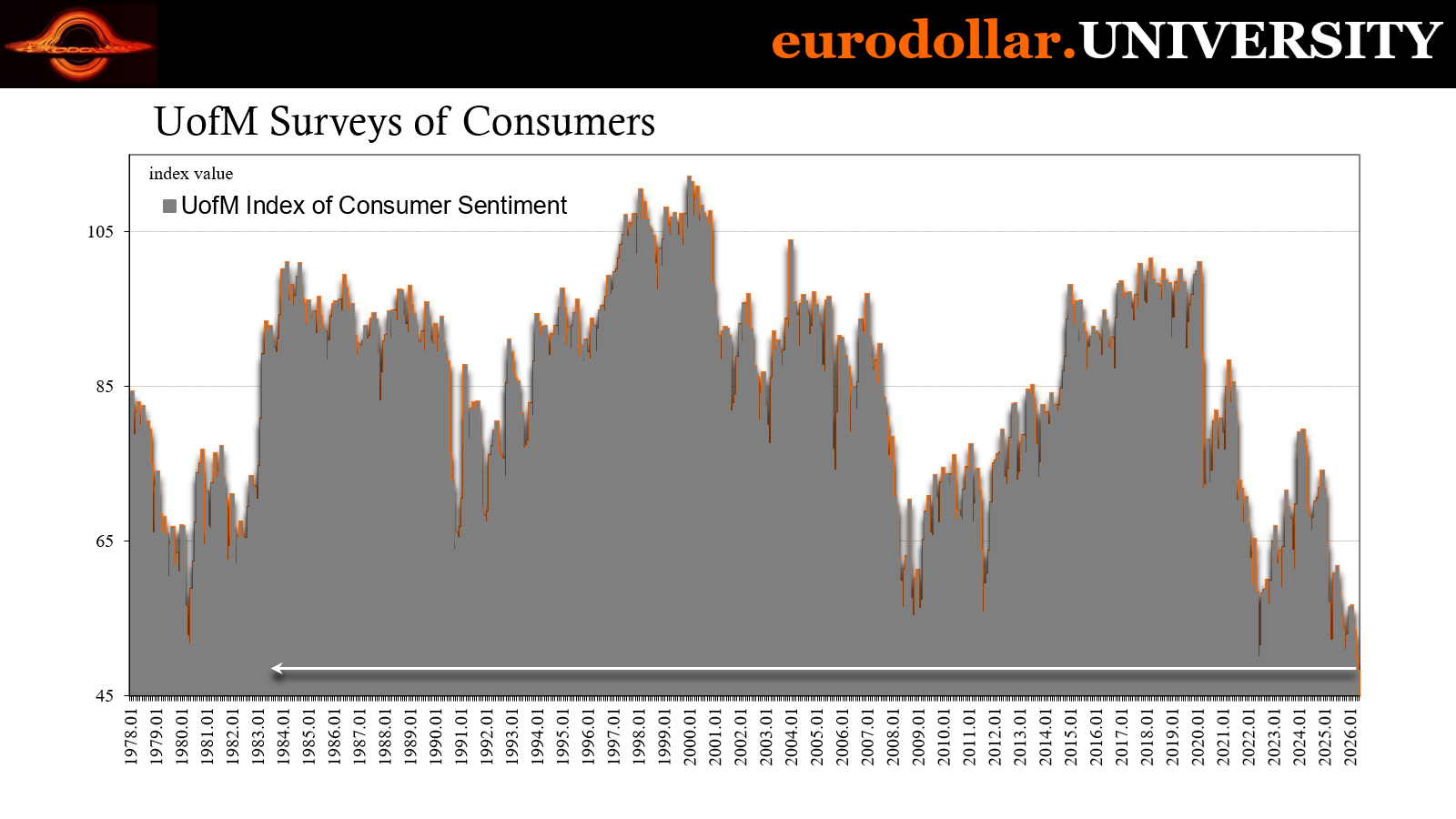

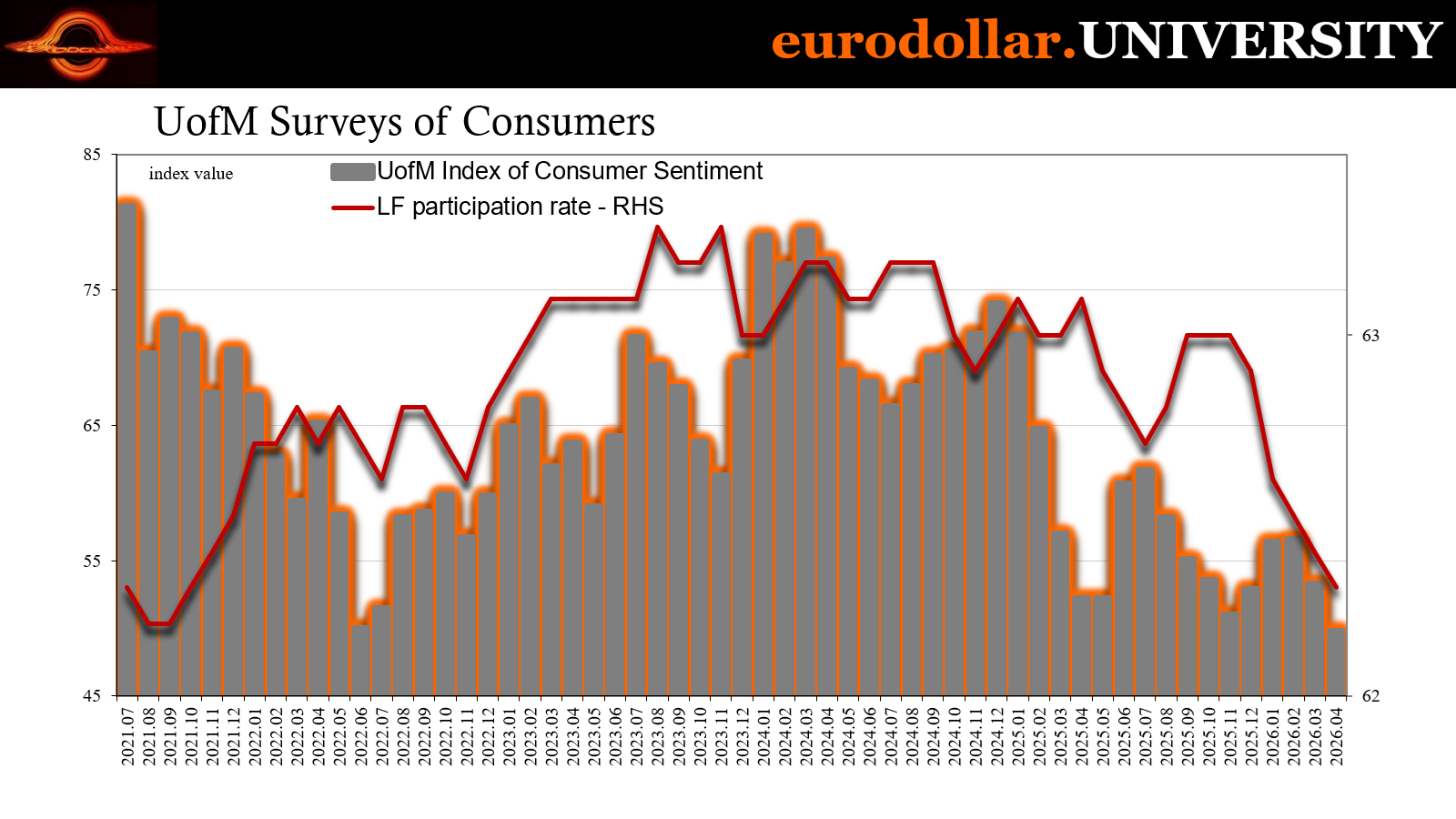

That five point eight plus five buck gas is exactly why the University of Michigan’s consumer confidence estimate set another new record low. Yes, this series is at an extreme compared to others in its classification, however all of them are only in disagreement as to just how pessimistic consumers have become. It’s differences of degree not category.

Moreover, the trends in consumer sentiment align closely with the labor data and leave us where Heinz is – watching people literally run out of money. It is exactly what consumers have been saying is keeping them up at nights, so with nowhere to turn for jobs and incomes once again regular Americans have been far better at economics (small “e”) than all the Economists who continue to dismiss not only their concerns but also the wider implications.

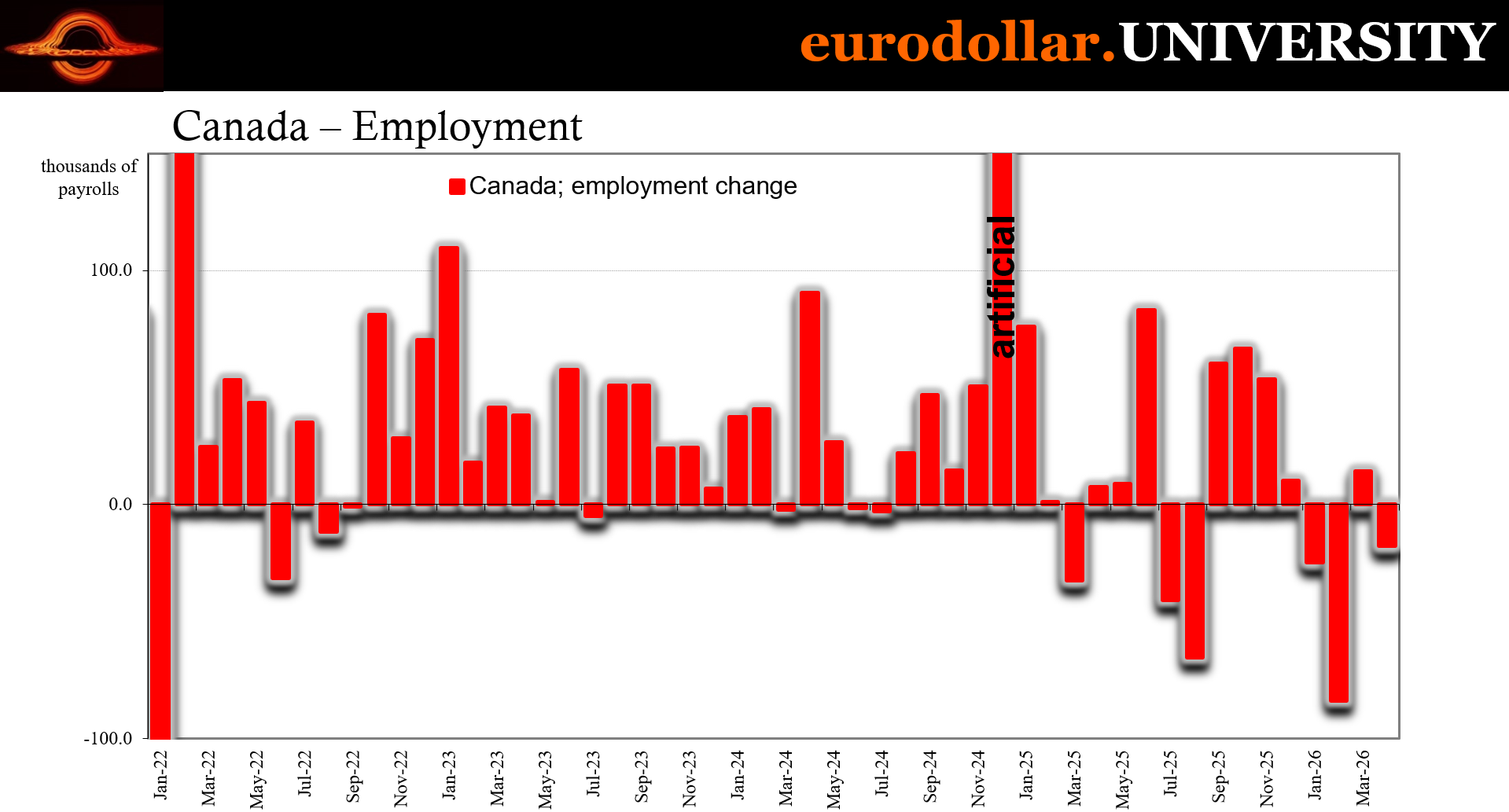

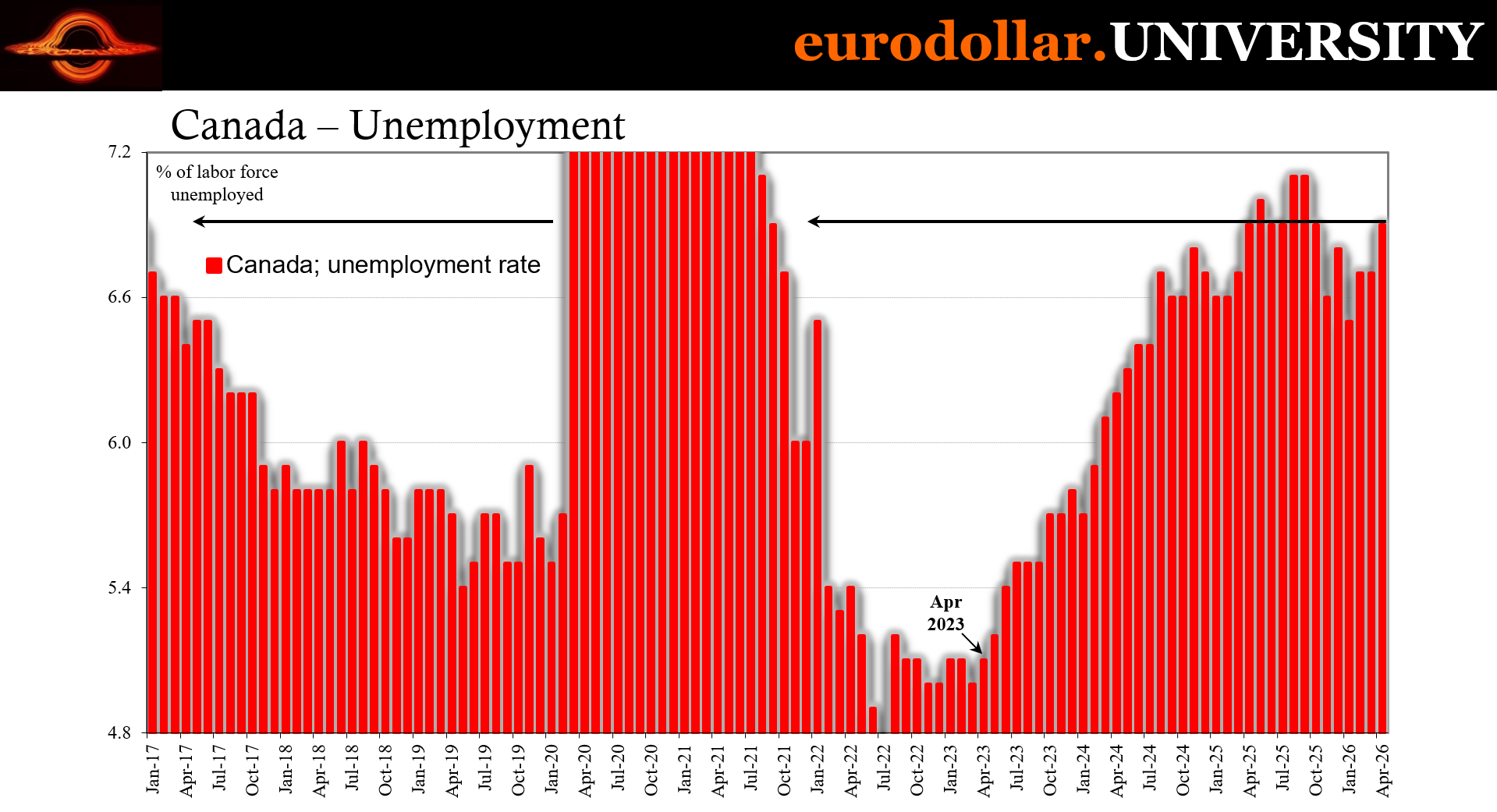

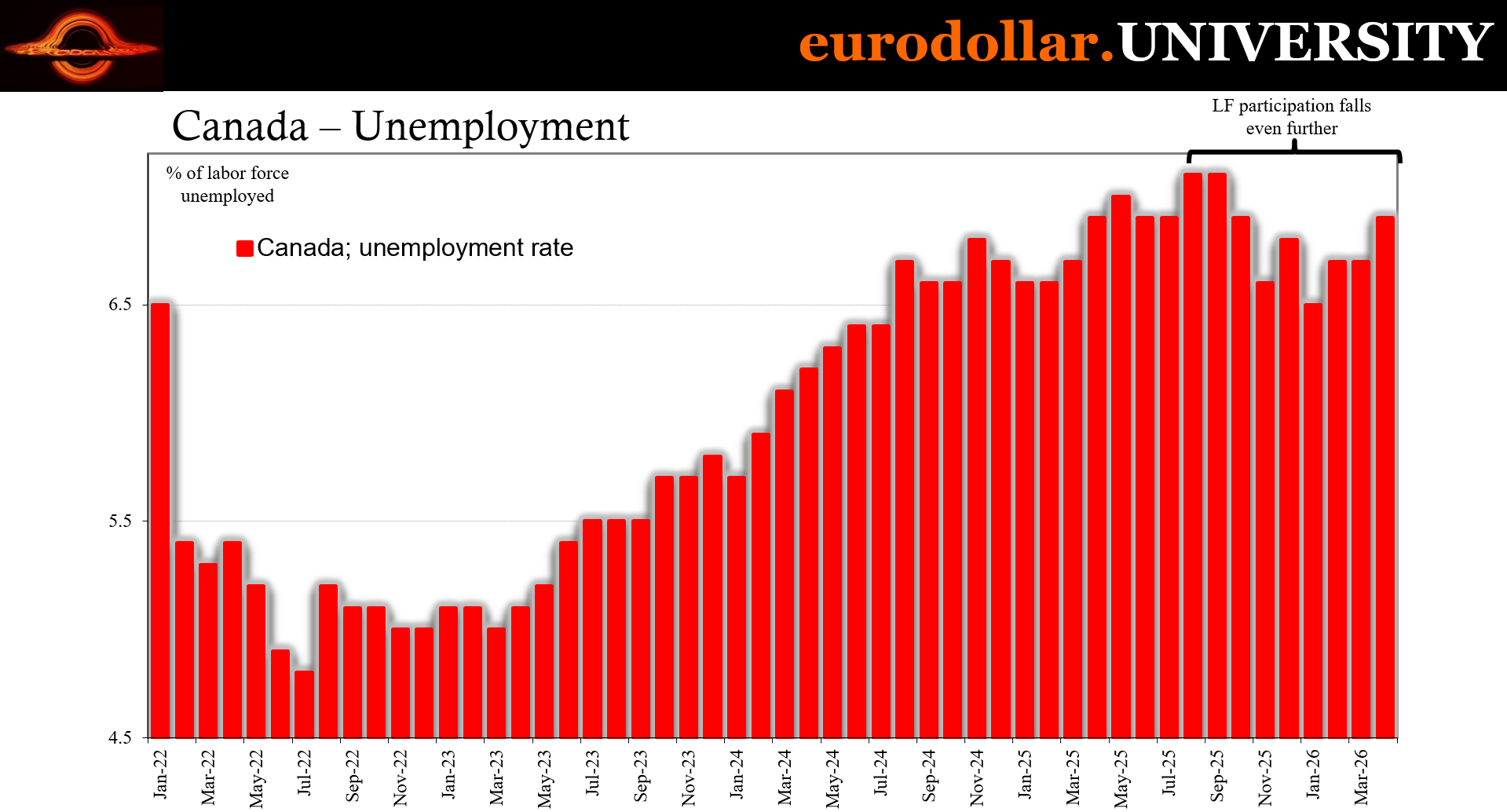

We are getting those from Canada, too, where April saw another “unexpected” decline in payrolls and rise in official unemployment. This further establishes (pun intended) global flat Beveridge getting flatter the farther we go in 2026 rather than stabilizing or rebounding.

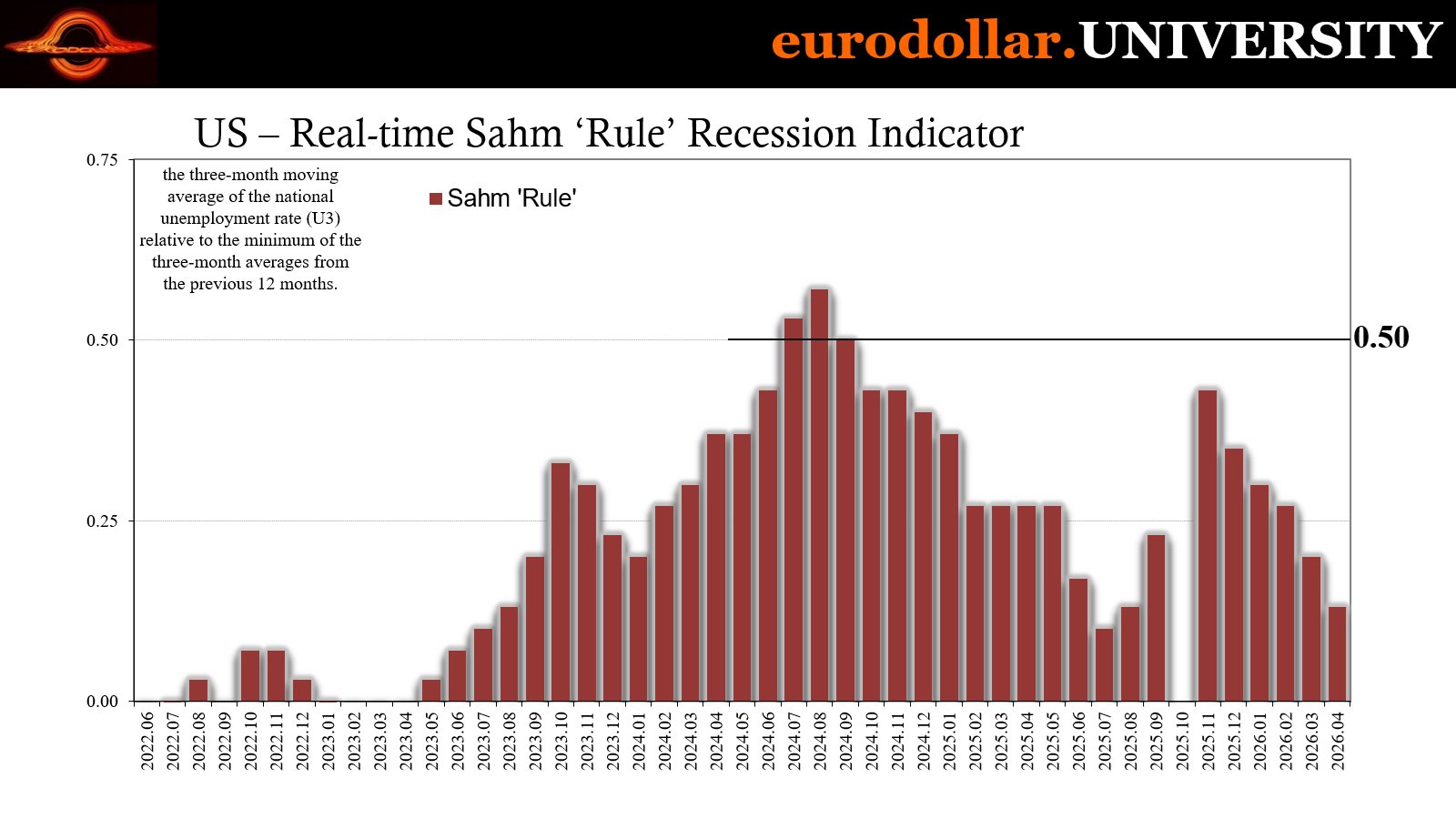

It is the hidden recession Claudia Sahm’s “rule” had signaled way back in the middle of 2024 alongside the Japanese carry traders, one that continues to hide in plain sight behind a single questionable statistic no one dares question even as the evidence against the thing piles up as high as Canada’s unemployment rate and the unofficial one in the US.

Sahm this

For a few months in the spring and summer of 2024, former Fed researcher Claudia Sahm was everywhere. The “rule” which bears her name (taken from other earlier researchers and changed only slightly) was inching closer to triggering a recession warning. In the past, once it had reached 0.50 that meant outright, NBER-will-say-so business cycle.

Basically, the “rule” looks at the momentum in the official unemployment rate. When it begins to rise quickly, once that indicates job market momentum has shifted too far in the wrong direction unemployment tends to keep building into full-blown contraction.

But that couldn’t be. Jay Powell at the time was far more concerned about economic resilience and sticky inflation. No, the Fed said the unemployment rate wasn’t signaling trouble, rather normalization. After all, following the “red hot recovery” in 2021-22, the labor market was just coming back into better balance all thanks to the skillful application of rate hikes.

Ms. Sahm herself agreed with Powell, the FOMC and the mainstream, spending much of her 15 minutes downplaying the signal coming from a number with her own name on it.

The Japanese obviously disagreed, which is why they erupted late in July and early August 2024 – the two months with the highest Sahm readings - afraid of both a deteriorating employment situation and what that would do exposing the massive and unwise reaching for yield bubble behavior which had gone unchecked for years in the riskiest corners of the credit market.

Give them their credit, they nailed that one right down to the timing.

But the official unemployment rate obscured all this. Even worse, it has been used to justify last year’s job losses and worse, which did extend into this year even if the last two months for the CES side were positive (CPS employment continues to be negative). Because the U-3 metric basically flatlined ever since Summer 2024 and peak Sahm, it appears as though both Sahm and Powell were correct.

This is how the mainstream has been able to dismiss job losses in 2025. Normally, negative payrolls would have central bankers searching for their stash of Pringles. Instead, like 2024, they were all-in on inflation again, the tariff variety this time around. Officials reasoned those negative jobs must’ve been insignificant otherwise if the labor market had truly been in trouble then U-3 would have gone much higher to confirm as much.

So, another few narratives were born, starting by blaming last year’s negatives on a population downshift owing to immigration enforcement. Not recession, politics. If there was any macroeconomic content in those minus months, that was also dismissed as “tariff uncertainty” and even more politics.

With U-3 stable, even the negative payrolls were turned into even more nothing-to-see-here.

Americans themselves disagreed at least as an aggregated interpretation. Consumer (and business) pessimism erupted at the same time Sahm showed up. So, which was it? Sahm and Powell on the one side arguing a constant stream of coincidences, first normalization then tariffs and finally immigrants. Or, on the other, US consumers, Japanese carry traders, negative payrolls, millions of dropouts not to mention the cockroaches and various very blue Blue Owls?

Rhetorical question, obviously

When Sahm hits 0.50, what everyone expected to happen if it was a “true” recession sign, was that the U-3 would continue to climb. As we know, it didn’t. However, that wasn’t the all-clear everyone said it was, instead the labor market conditions underlying everything unleashed a repeat of depression behavior we’ve seen before.

In the aftermath of 2008, for the first time in modern history the labor force itself began to shrink. It wasn’t due to Trump retconning his policies into the early 2010s, rather beginning October 2008 when stocks began to fully meltdown American workers started to drop out of the labor force in droves. It was a response previously unheard of, one thought be Economists to be impossible. Those pour souls had been let go of their previous jobs and understood only too well the Fed’s symbolic “rescues” were nowhere near likely to rescue the labor market.

They stopped looking for work straight away because why bother doing so when everyone outside the FOMC and financial media knows no one has any jobs to hire. And because they dropped out, the BLS stopped counting them in the official labor force therefore dropped them right out of the official U-3 unemployment rate, too. Hardly anyone noticed at the time because the number did what the Sahm rule expected it would, rising sharply from thereon.

But even that understated the true scale of the devastation. Though the U-3 rate peaked at 10% exactly in October 2009, when accounting for lower LF participation the rate would have been roughly two points higher. Yes, the contraction was worse than it was made to seem, a fact which would become all-too real over the years ahead with the lack of recovery.

Once those former workers left the LF they never went back. Of the few who did, more who never had a chance to enter in the first place stayed on the outside looking in. The devastating depression would linger onward into the middle 2010s before the economy finally reached a bottom. It started to move forward again but never close to recovering.

Silent Depression.

Something very similar happened in the middle of 2024, though not to that extent only repeating the pattern of behavior. As the Sahm rule showed downside labor market momentum was reaching that critical threshold, once again Americans responded to it by dropping out of the labor force. The recession did happen, and we can see both it and its effects, but the contraction didn’t show up in the official stat because of how U-3 specifically is defined.

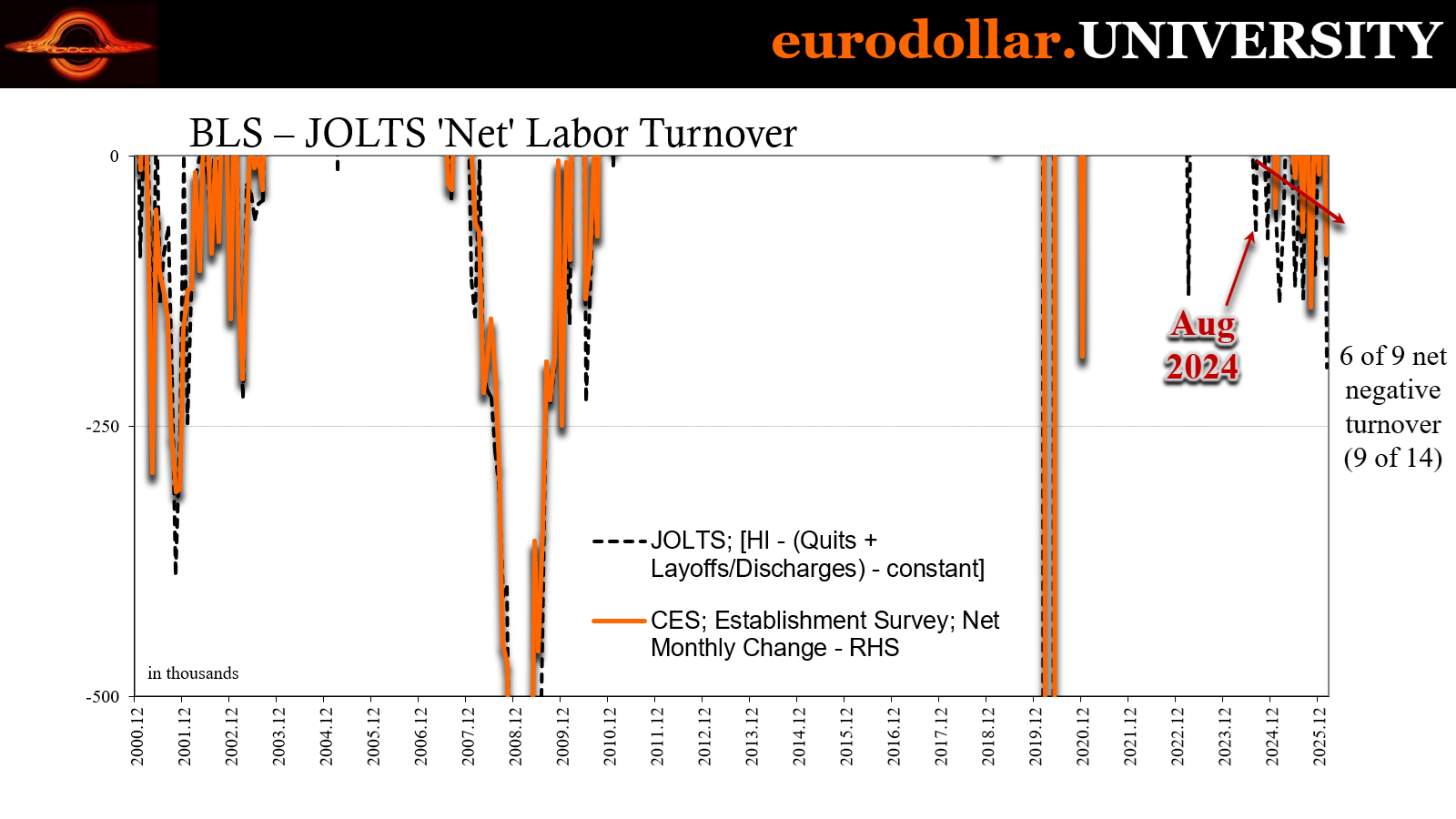

The Sahm rule was correct, only everyone missed the confirmation because they assumed confirmation would be found in the same U-3 rate. Yet, it was there in all three BLS surveys, CES (belatedly), CPS plus, don’t forget, JOLTS where the last of those began to produce negative labor turnover in August 2024.

The same month as the carry trade blowup and also the max for Sahm above the 0.50 threshold. Are we really supposed to believe this is just pure coincidence? Bad things were happening in the labor market and convincing Americans to exit it. Bad things have continued to happen consistently since then.

You can’t handle the truth

I haven’t yet mentioned market signals, particularly curves which had warned about these probabilities from well before they showed up in Sahm’s face. The global bond rally which began in October 2023 was a warning the outlook was darkening. Though hardly any of them knew it, consumers agreed as sentiment soon soured.

In reality, labor participation began to soften long before the middle of 2024. After all, Sahm’s rule is about momentum which means bad things were building steam prior to that summer. For the official numbers, participation pivoted late in 2023 along with market interest rates, all while the Fed was on “sticky inflation” watch due to their sticky view of a “strong and resilient” economy.

I’ve covered before how subsequent benchmark revisions to the Establishment Survey (thanks to QCEW) have established this same inflection point. What had been a monster payroll gain in September 2023, for example, initially figured to have been a whopping +336,000 has since been revised in half to +156,000. From there, years of revisions have chopped down those seemingly favorable first-time estimates to something which would fit the Sahm rule rising toward its threshold within months of 2024 beginning.

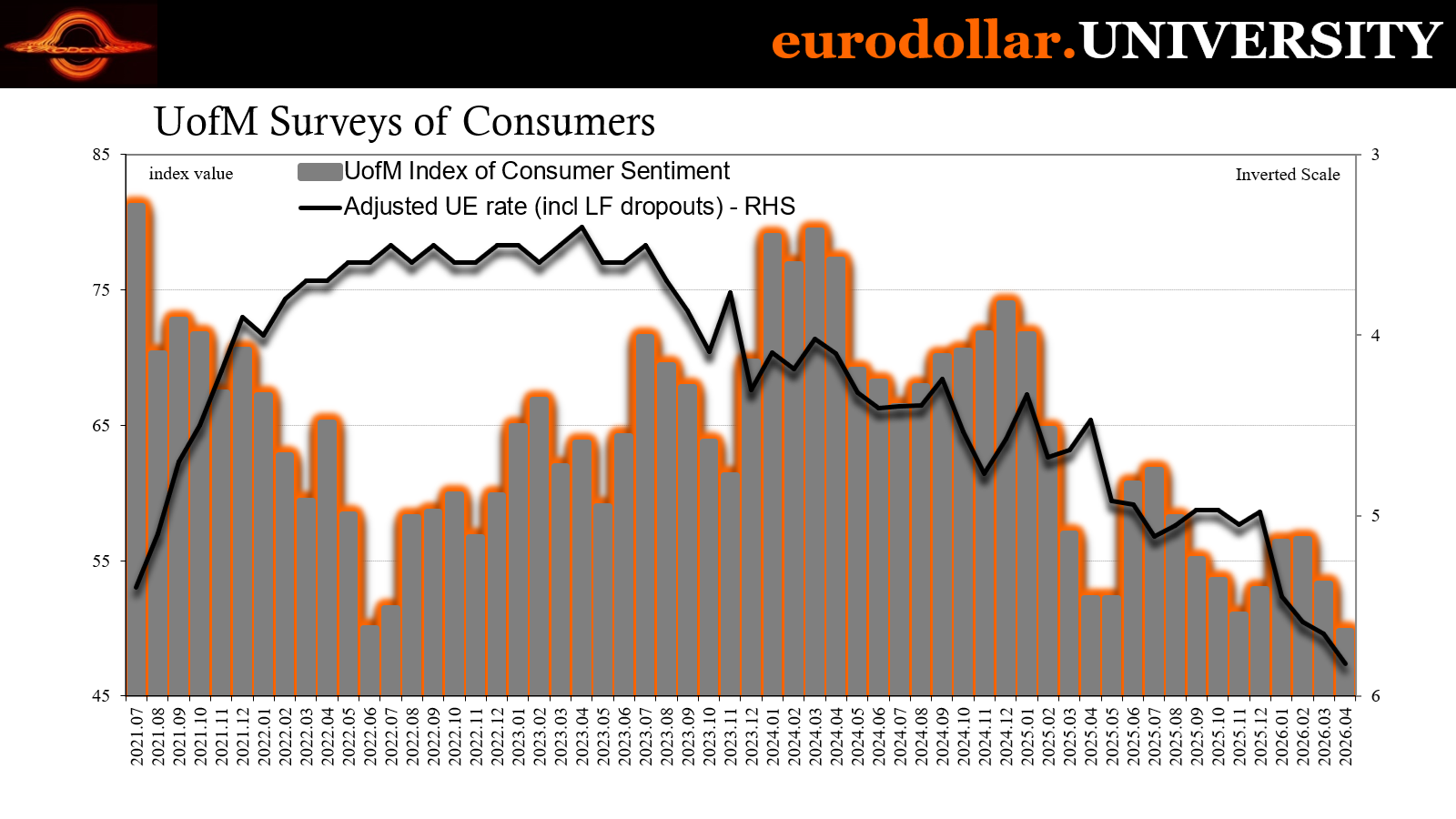

As all that was taking place, labor participation was reversing, meaning the dropouts were starting to drop out in significant numbers repeating the post-October 2008 response to a downturn. This is where my adjusted unemployment rate comes in, beginning to pick up on a meaningful difference with the official number.

But look at where the adjusted rate, meaning lower participation, meaning accelerating labor dropouts, really starts to diverge:

Just after the Sahm peak.

My unofficial unemployment rate pointed to the hidden recession the Sahm rule had itself uncovered. Americans reacted to the labor market contraction – in reality – largely the same way they had in 2008 and after. They couldn’t find jobs and so stopped looking unlike previous recessions when those laid off never stopped looking for work because they dependably looked forward to legit recovery. When Sahm got triggered in those earlier cycles, the U-3 rate wasn’t distorted and so it appeared consistent from start to finish.

In ‘24, it looks like the contraction was somehow interrupted before completing the full cycle; or, it allowed that benign interpretation favoring “normalization” to appear plausible. But the latter requires also explaining 2025’s results and not just in macro data (Blue Owl).

This is one of those situations where Occam’s Razor truly applies: what is more likely? That the process of what appeared to be a looming recession suddenly stopped for no given reason, and then other factors, problems which coincidentally kept showing up one after another producing outcomes consistent with recession, benignly explain as something else everything looking like a continuous recession that had followed these numerous clear recession signals?

Or, the unemployment rate is simply flawed and therefore gave misleading directions the whole time because it doesn’t account for cyclical dropping out which is now seemingly a durable post-2008 feature of the real economy. Sahm’s rule said recession by Summer 2024 and everything from that point onward, save Sahm and U-3, validates the trigger.

Including cockroaches and owls, as forewarned by the Japanese.

The consumer connection

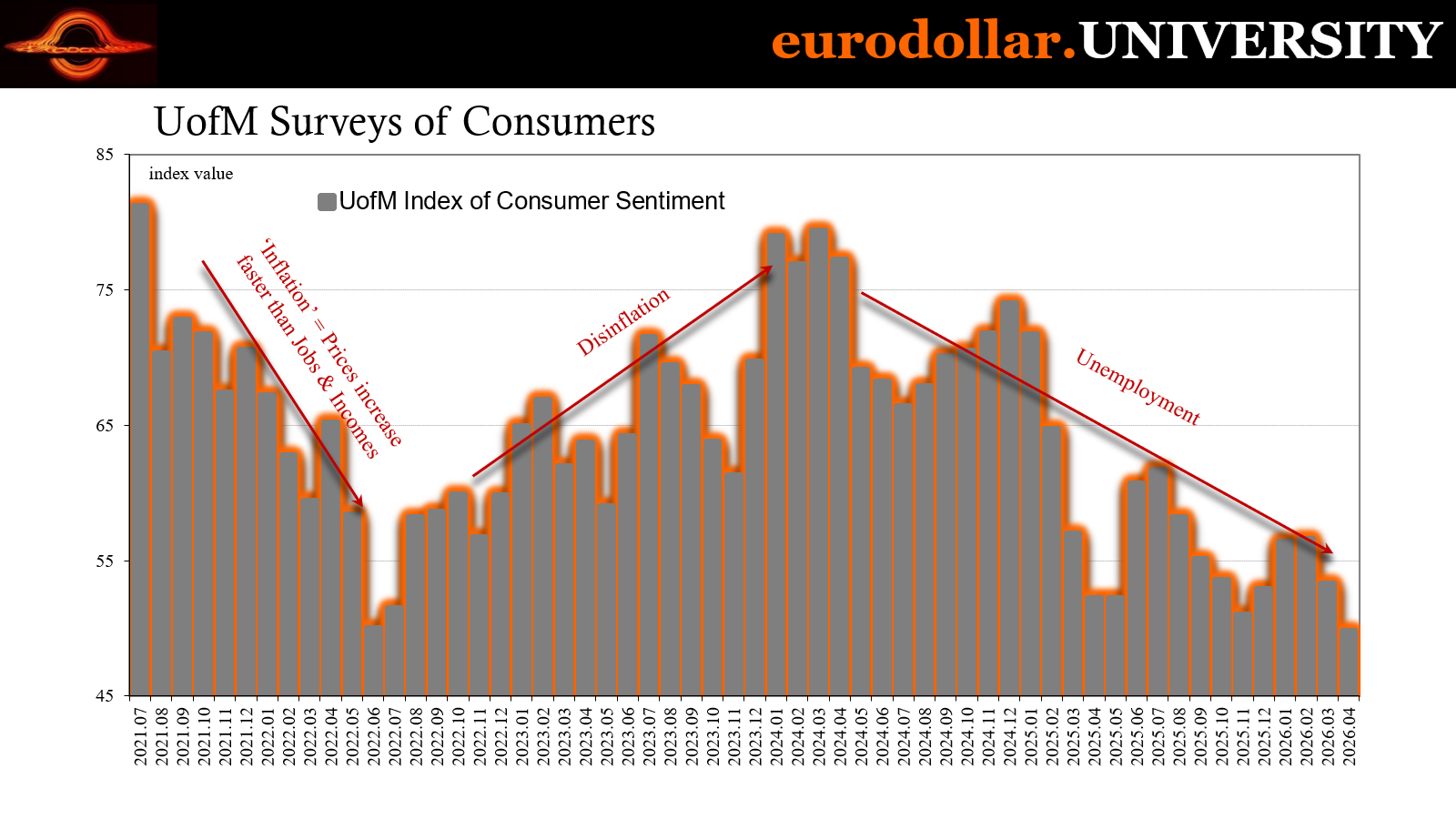

The thing is, Americans themselves have been saying exactly that this entire time. Set aside the extremity of the University of Michigan and its record lows here in 2026. Instead, focus on the trends before coming back to the intensity.

Consumer sentiment follows unmistakable paths. It originally tanked in 2022 and early 2023 because prices throughout the economy (“inflation”) were rebounding far more quickly than incomes and jobs did. No surprise, consumers got to be very pessimistic (and angry) about the situation, particularly since they were repeatedly told the economy was booming (LABOR SHORTAGE!!!) even as if left them further and further behind.

What followed by the middle of 2023 was disinflation, where price pressures began to cool off while the labor market was still undergoing positive momentum (not recovery). Sentiment rebounded, rising throughout 2023 into 2024.

But it was already being undermined by what we just reviewed. It took sentiment a few months to catch up to this, but once it became clear “something” was truly amiss consumer pessimism returned. For the UofM index, it peaked in March 2024 and began to reverse significantly two months later.

May. Right into full Sahm. That’s not coincidence.

Americans were telling Michigan surveyors they didn’t like gas prices rising again, sure, but also that something was going wrong with jobs right as labor force dropouts started to pick up and the Sahm rule climbing into its trigger. Higher energy costs combined with a deteriorating jobs market was obviously going to create anxiety and negativity.

I mean, just look at the correlations between those labor numbers which do take into account dropouts, first the participation rate and then our adjusted unemployment ratio:

Ever since Sahm and Summer 2024, consumer sentiment has been falling sharply. Not in a straight line, some back and forth, typical fluctuations and short run variations, yet the trend is unmistakable. This also means, like the labor data itself, there wasn’t something new hitting the economy in 2025 (and 2026 prior to March), it was just the continuation of the same Sahm trend completely missed by the official U-3 metric because it was left out of its definition.

Confidence sank as effective unemployment kept rising. The hidden recession was hiding in plain sight the entire time and Americans kept trying to tell the clueless mainstream media and Fed officials about it the whole way, only to be rejected as overreactions to tariffs or whatever other excuses.

Either the economy and labor market normalized nicely but just happened to be met with repeated one-offs one after another producing recession-like results all over the economy and markets, or a recession that looks like one in every way other than this one just is what it is.

The implications were already profound even before the energy shock, as we’ve seen only too well in the junk debt markets and everything surrounding them. After all, those perpetuating the bubble were doing so thinking U-3, Powell and Claudia Sahm herself were on sound ground, so they kept lending into the growing storm.

How else do we get to a place where the CEO of Heinz is alarmed by negative cash flow and consumers running out of money? Expensive gasoline is only one part of the equation, the hidden recession being the other. That’s Whirlpool. And private credit.

But this thing is not limited to the US. For even more confirmation, look no further than Canada and its jobs data. They match the US experience very closely and from the official unemployment rate, too (even though participation up there has been falling, as well, which means as bad as the jobless rate already appears joblessness is much worse).

Everyone had been expecting to see a recovery in Canada this year, one starting with a labor market turnaround when instead negative jobs have continued almost without letup. The only positive of the four months thus far in 2026 was barely on the plus side.

The global economy stumbled badly from 2023 into 2024 (why that was is another story, one of tangled causes including, yep, the 2023 banking crisis aftermath; just look at global bonds for proof of that one) and by all accounts, save just the one, from consumers to Canadians the downtrend has been ongoing ever since.

Slowly, but outside America’s U-3 almost unmistakably.

Put that kind of weak economy in front of $5 gasoline and it is a recipe for…inflation?

Of course not. But when an entire recession has been allowed to be completely covered up by a single, defective number, nothing should be surprising anymore.