THE PRINGLES CYCLE

EDU DDA Feb. 17, 2026

Summary: The idea of a global end to the rate cutting cycle has taken a huge hit recently - to the point, one of the few actually hiking is now closer to turning around and cutting than any of the other rate cutters other than RBA are to begin hiking. From commodities to north North American CPIs, bond yields in USTs, Canada, Switzerland even JGBs, recessions in Japan plus, yes, Switzerland. Reflation 2026 never stood a chance.

The Pringles cycle was supposed to have come to an end. Maybe a few stragglers might make a few final rate cuts, but by and large the mainstream spun hard for hiking. When the Reserve Bank of Australia did it two weeks ago, the rhetoric shot up but the narrative elsewhere was already falling apart.

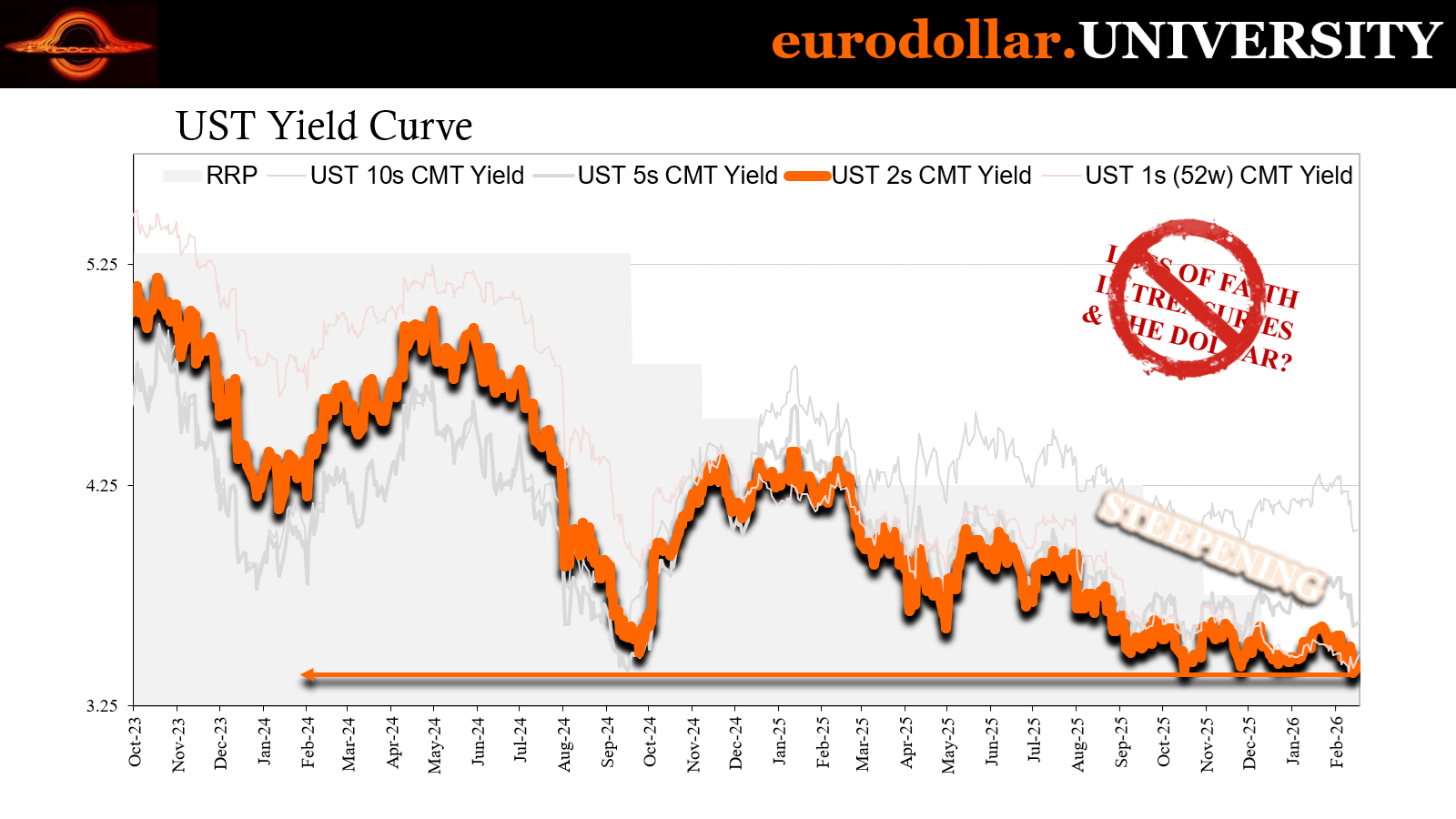

Bond yields globally have seen a renewed lower leg, starting with Treasuries but not limited to them. Even JGBs have rallied, alongside Brits and Swissies, Maples, too.

It may be tempting to explain each one using purely local factors, however globally synchronized prevents any such idea from leaving our imagination. There is a common theme emerging from all these different financial curve threads, one that is coming through in a large amount of macro data.

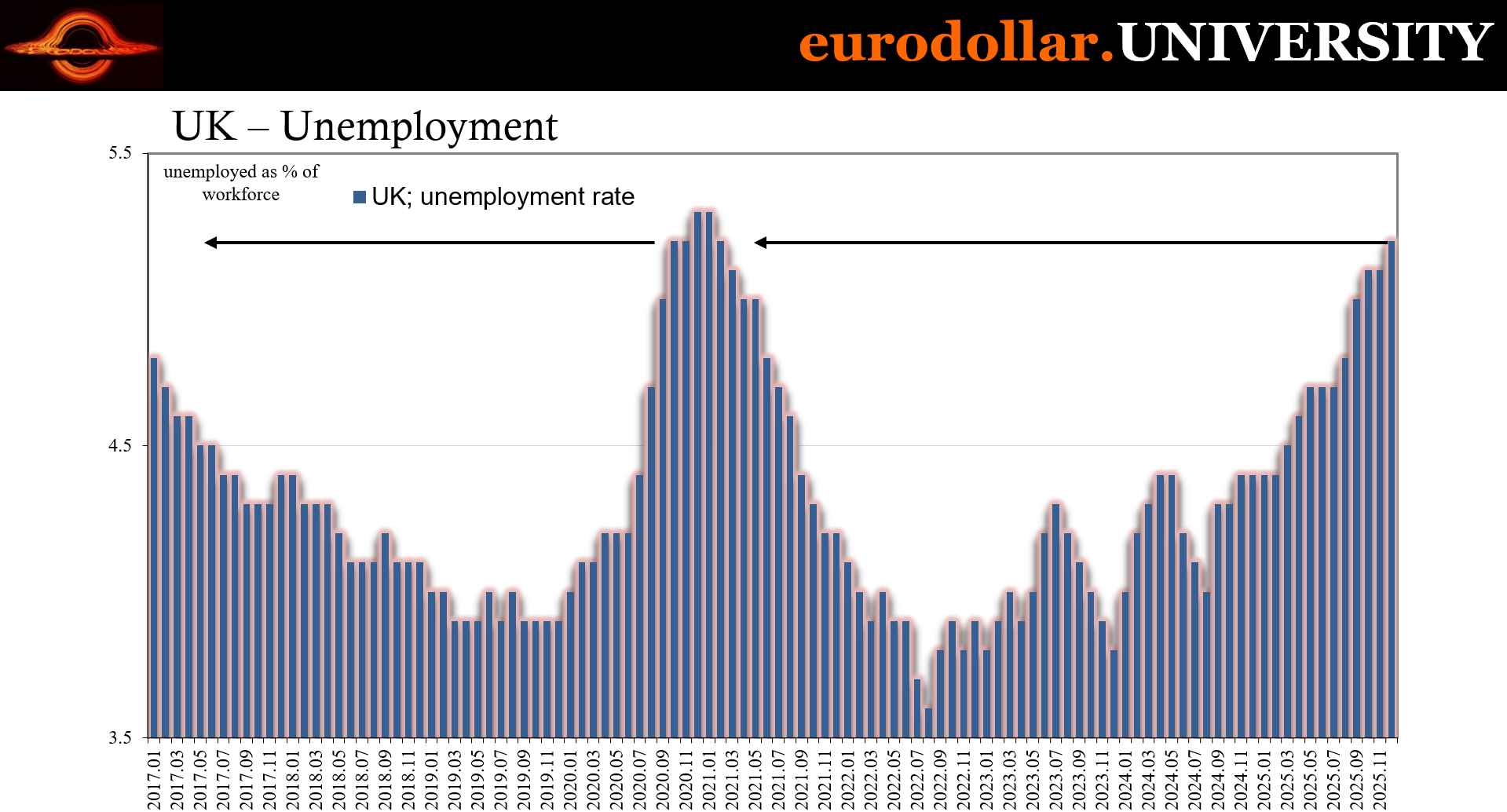

We could include the Chinese and its woeful bank lending start to the new year (I covered this on YT) or the UK’s latest new high for unemployment, but we’ll stick to North American CPIs (US & Canada), Switzerland’s plus its unemployment and bonds, finally the Japanese situation where yields are lower not because of Takaichi’s victory rather what just came out in GDP.

Yes, another unofficial recession in the supposedly inflation hotbed of Japan.

That tone was supposed to be reflationary. Yes, I know, it is each and every year going back to 2021. However, 2026’s iteration took on an extra element of confidence for a variety of reasons. That confidence had been built out of little if not nothing and the confirmation for it just arrived in bunches.

Commodity down

One of the primary reasons stated for the coming global rate hiking was commodity-led inflation. As we know only too well, metals – some of them – have been on fire which, traditional thinking, it must mean a flood of investors into real assets fleeing from the reflationary perhaps inflationary future.

Copper is a big one along those lines and when considered in isolation, like gold it at first seems to validate the interpretation. There’s always that blind spot, a tendency to zoom in on a single market signal and then make it say what it is “supposed to.” Recent copper behavior must have meant a boom on the way.

One only ever needed to compare it to gold to be immediately disabused of the notion. When put together, it was only ever a deeply deflationary signal, one that is revisiting deeper into its bad side now that copper can’t even hang on its own narrative.

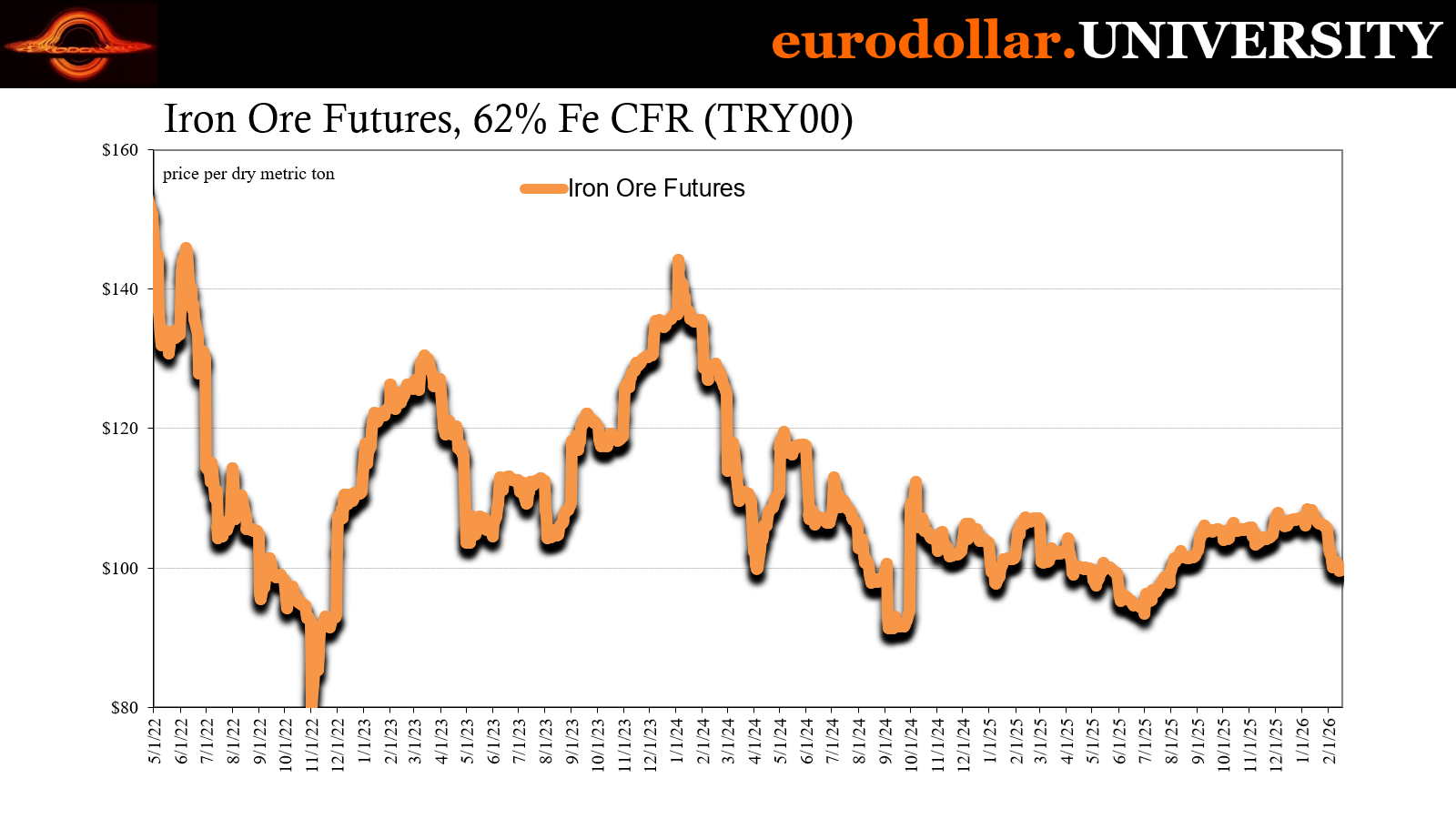

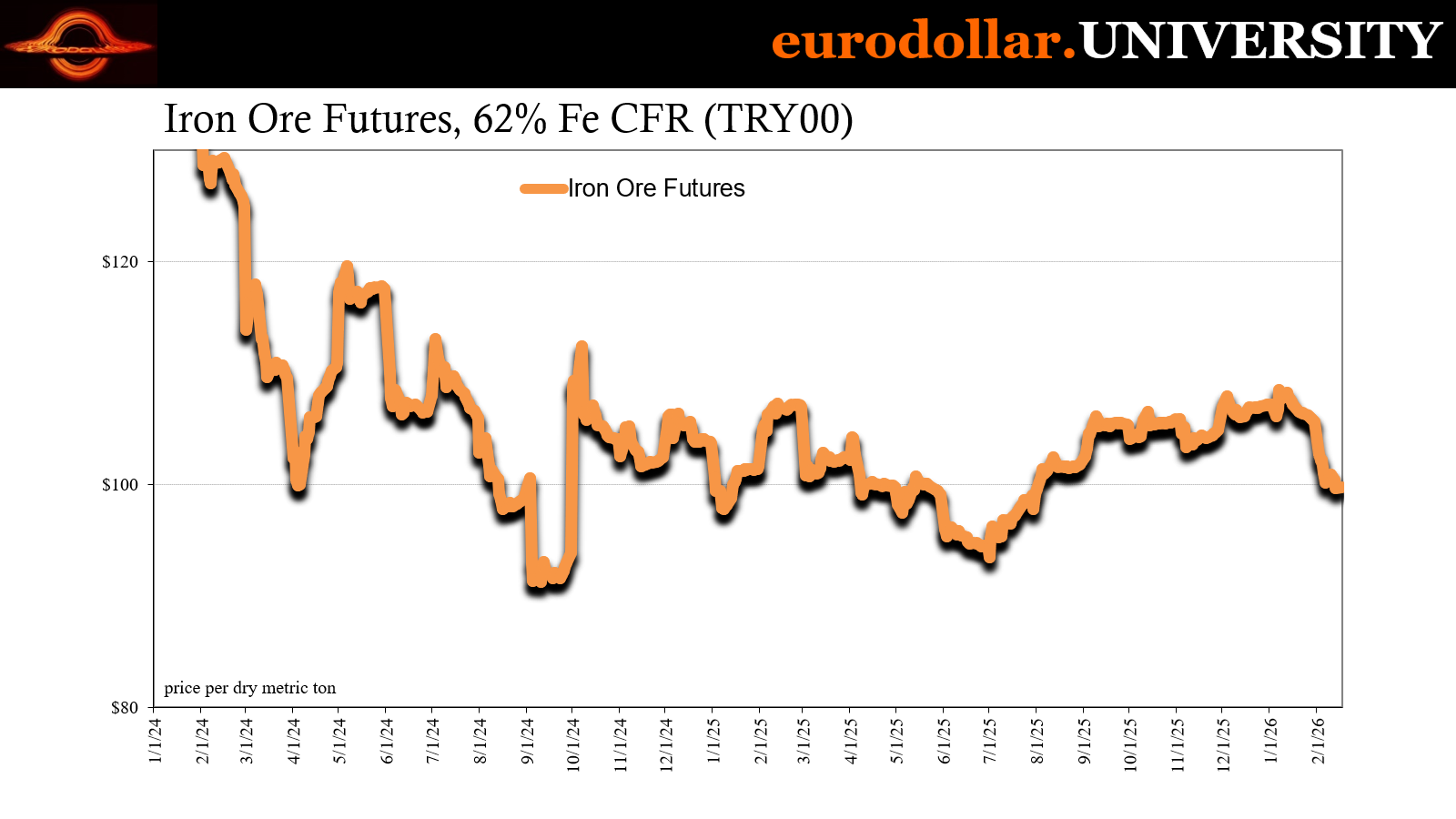

Iron is a little different, importantly having avoided the supply mania spiking silver and copper. Even so, there was a bit of a bump in iron ore, tracing back to the summertime. The upward move was barely upward, yet in grasping for straws iron at least provided one, if a very thin example.

Like copper, that’s now over. As of this week, US$ iron ore has slunk back underneath $100. If there was any improving industrial demand from either copper or iron, it’s disappearing again as bond yields dip undertaking a broader market survey and more easily rejecting the perception of reflation and rate hikes, no takers for the end of global Pringles.

Those upsides never appeared in any consumer price data, either. Not that we – or anyone – should have expected as much, but you know how the medias – regular and social – corrupt basic economics (thanks largely to Economics). Even if the rise in copper or precious metals and iron, too, signaled something from investors, either rising demand or inflation hedging, CPIs across the world are actively erasing the thought.

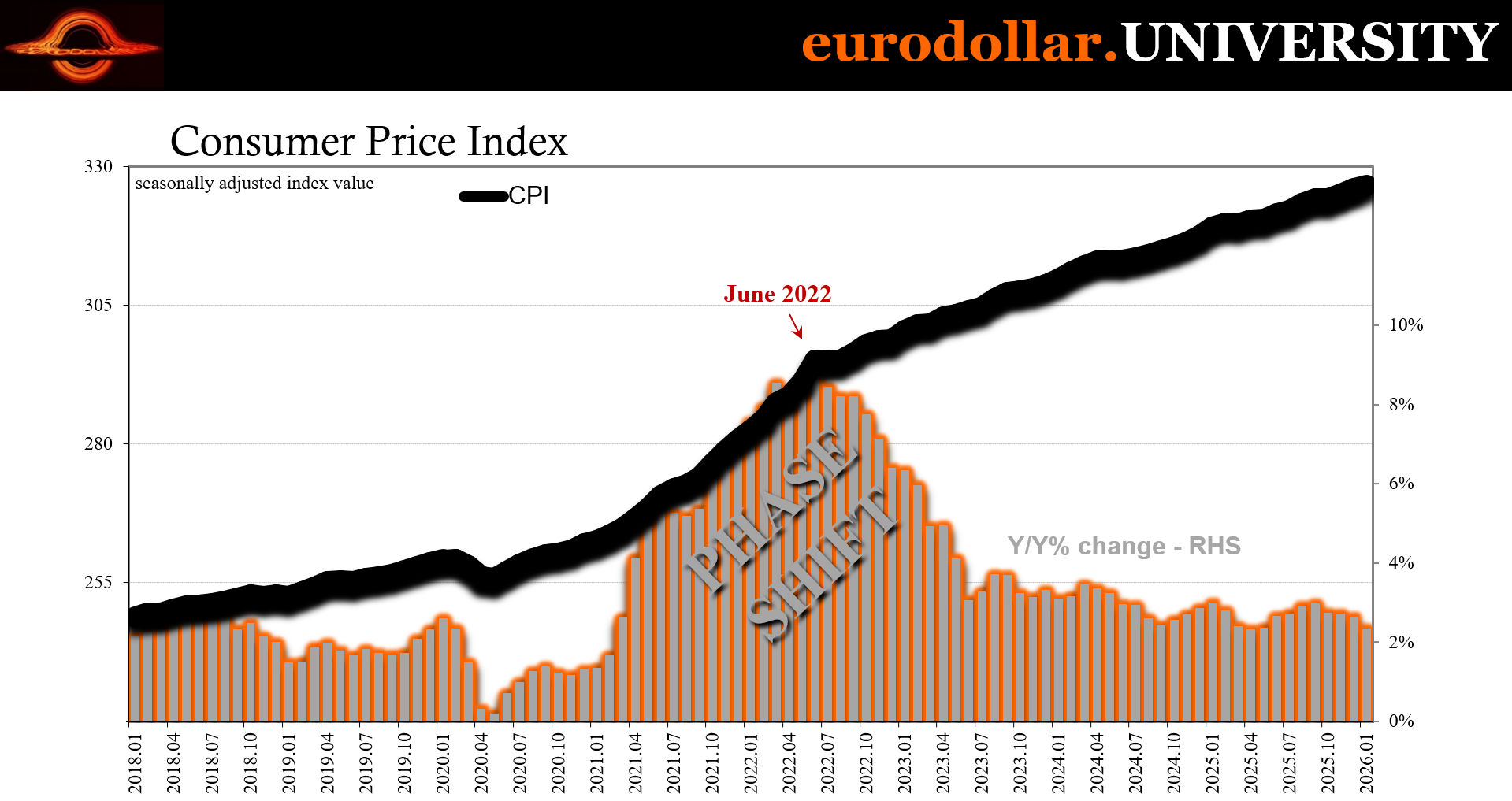

Last Friday, the US CPI came in underwhelming. The numbers were mainly right on expectations, if a little beneath them on a headline index pulled down by gasoline. It was supported especially in the core part of the bucket by another surge in transportation services. Unfortunately, the spike isn’t from Americans boarding airplanes and vacationing early ahead of the boom, rather auto insurance premiums soaring once more which will cost everyone a lot of any of their future leisure.

Like we’ve seen too many times already, the jump in insurance costs will only add more to the misery, take away further from upcoming CPI rates, and generally destroy more consumer demand at the margins. With the core rate down at its smallest year-over-year change since 2021 anyway, you can see why the Treasury market reacted with the lowest 2-year yield falling to its lowest in years.

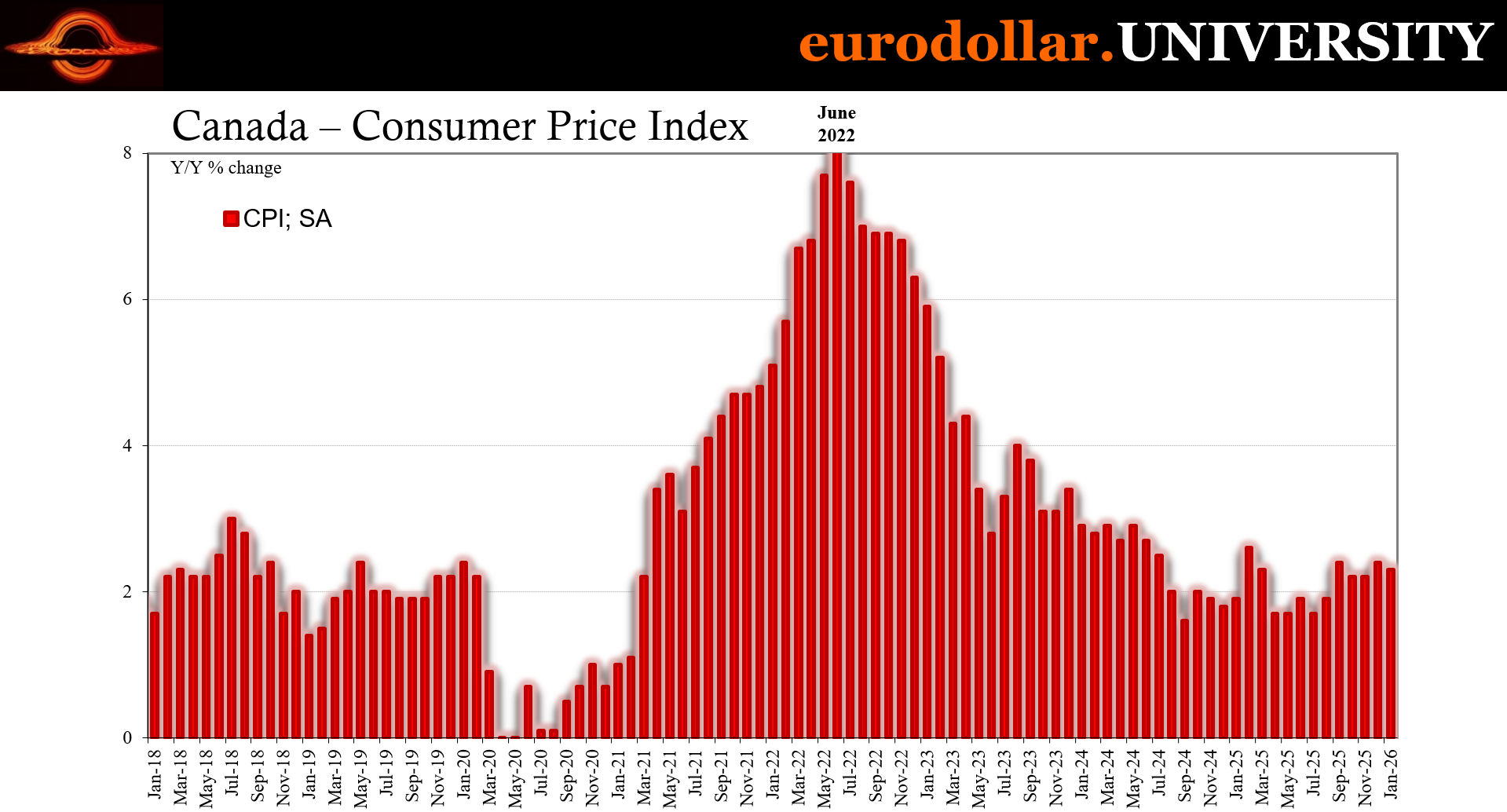

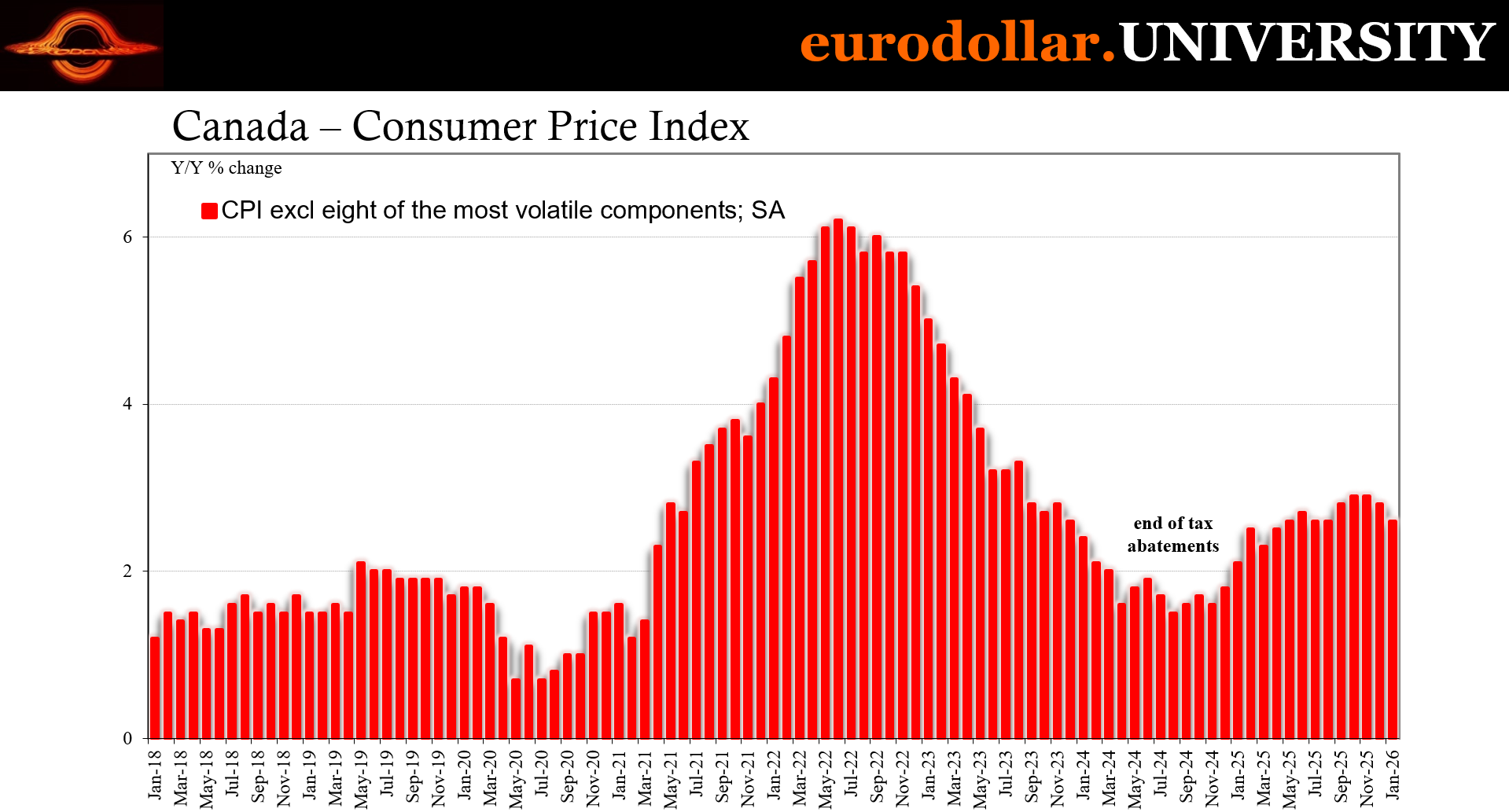

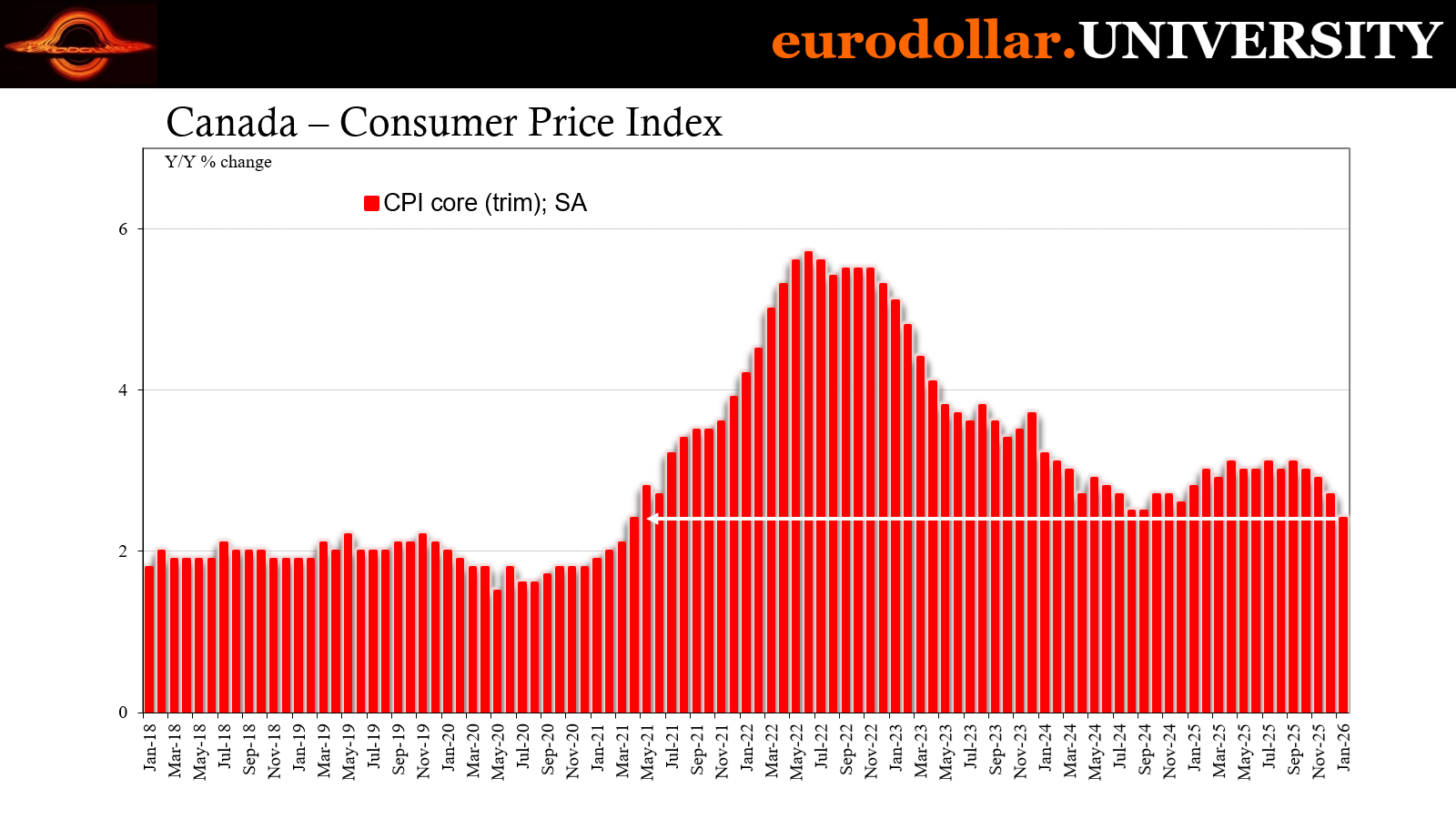

Up in Canada, similar developments in the CPI as well as maple bonds. The headline Canadian rate slipped to 2.3% year-over-year as the core rate (trimmed mean) notched its weakest also since 2021.

As far as the north of North America is concerned, any idea of tariff inflation is dead and buried. It’s been a year now of constant predictions over imminent ignition, with little if anything to show for it. Commodities were bumped by supply restrictions rather than thickening demand (iron), CPIs moved very little rather than aggressively having already rolled back over late in 2025 and at the start of 2026.

Much of that global hawk/reflation expectation centered around the idea of everything picking up to close out last year. If tariffs and really “tariff uncertainty” were to blame, then the fading effect of them would allow the global economy to regain its footing. The fact we see nothing of the kind in any of prices, economy or bonds simply proves tariffs had little to do with the underlying trend around the world.

At most, a small, temporary deviation.

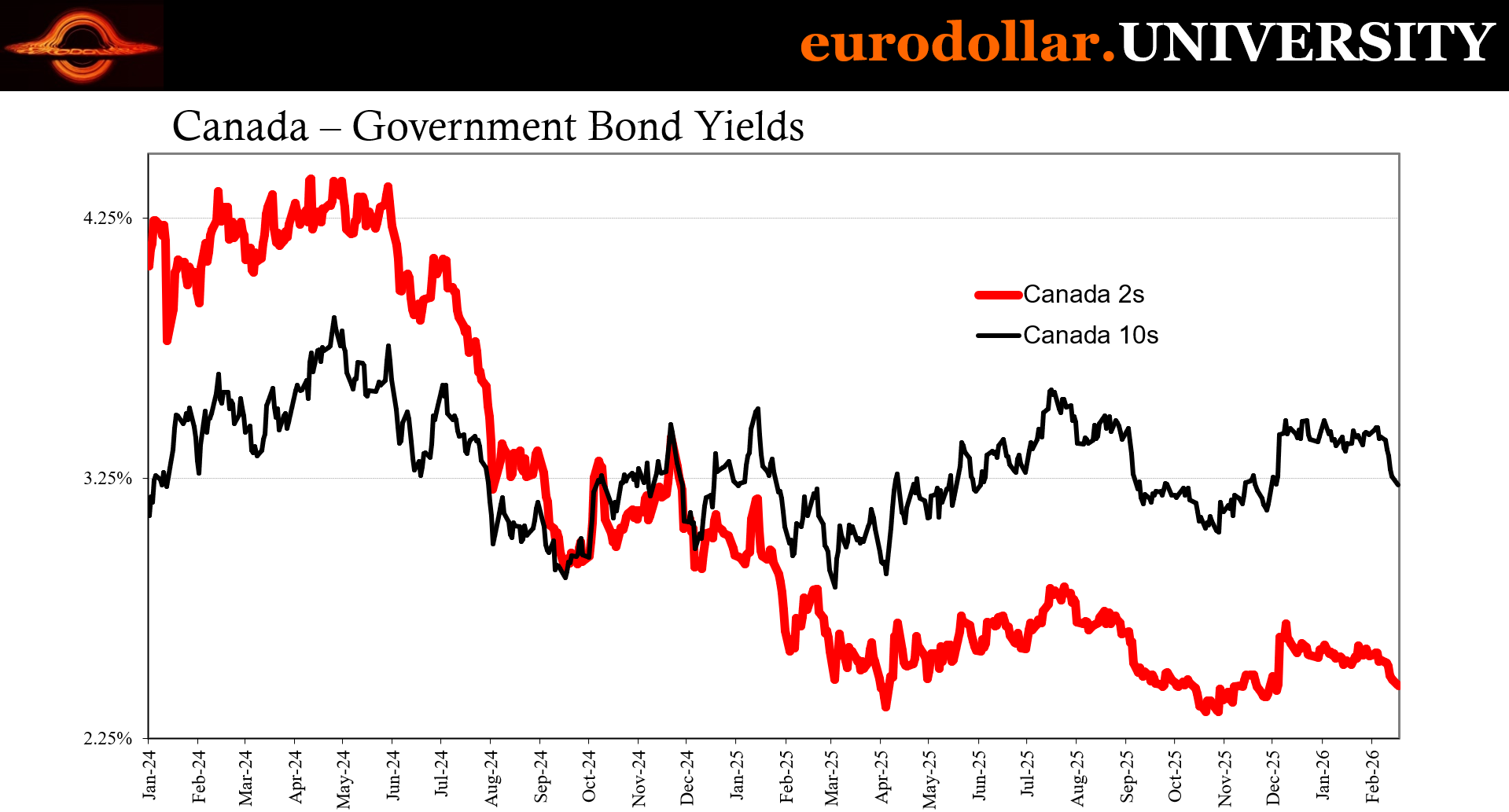

That certainly counts for Canada’s economy where GDP is looking weak in Q4, combined with softer labor data (especially when accounting for massive labor dropouts responsible for the drop in the unemployment rate) which puts the Bank of Canada back closer to rate cuts than hikes. Any brief flirtation with the latter was terminated in the CPI data, with jobs and GDP far more likely to reignite Tiff Macklem’s tickle for Pringles.

It was priced into the front of Canada’s curve, where the maple 2-year slid to 2.45%, lowest since early December back when this rate-hikes-are-coming idea really got going. It didn’t last very long, in Canadian bonds or others, as we’ll see, nor USTs.

The chances of a reflationary reject of rate cutting rested on the thinnest of notions to begin with, never a real possibility by all the various markets (and data) when taken together (as they should be). Now, with rolling over coming across on multiple fronts, the Pringles can is not surprisingly back at the center.

Swissie

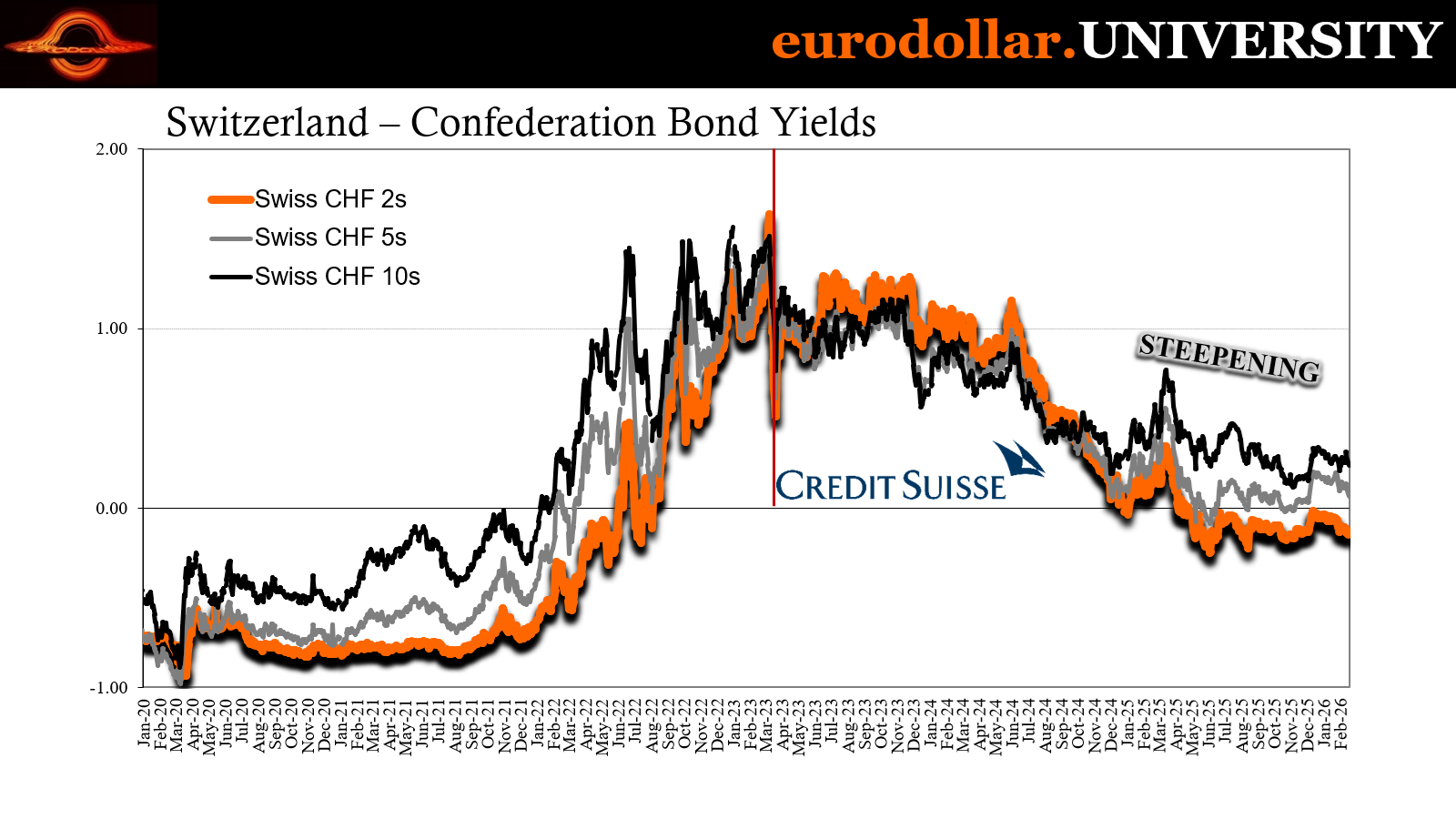

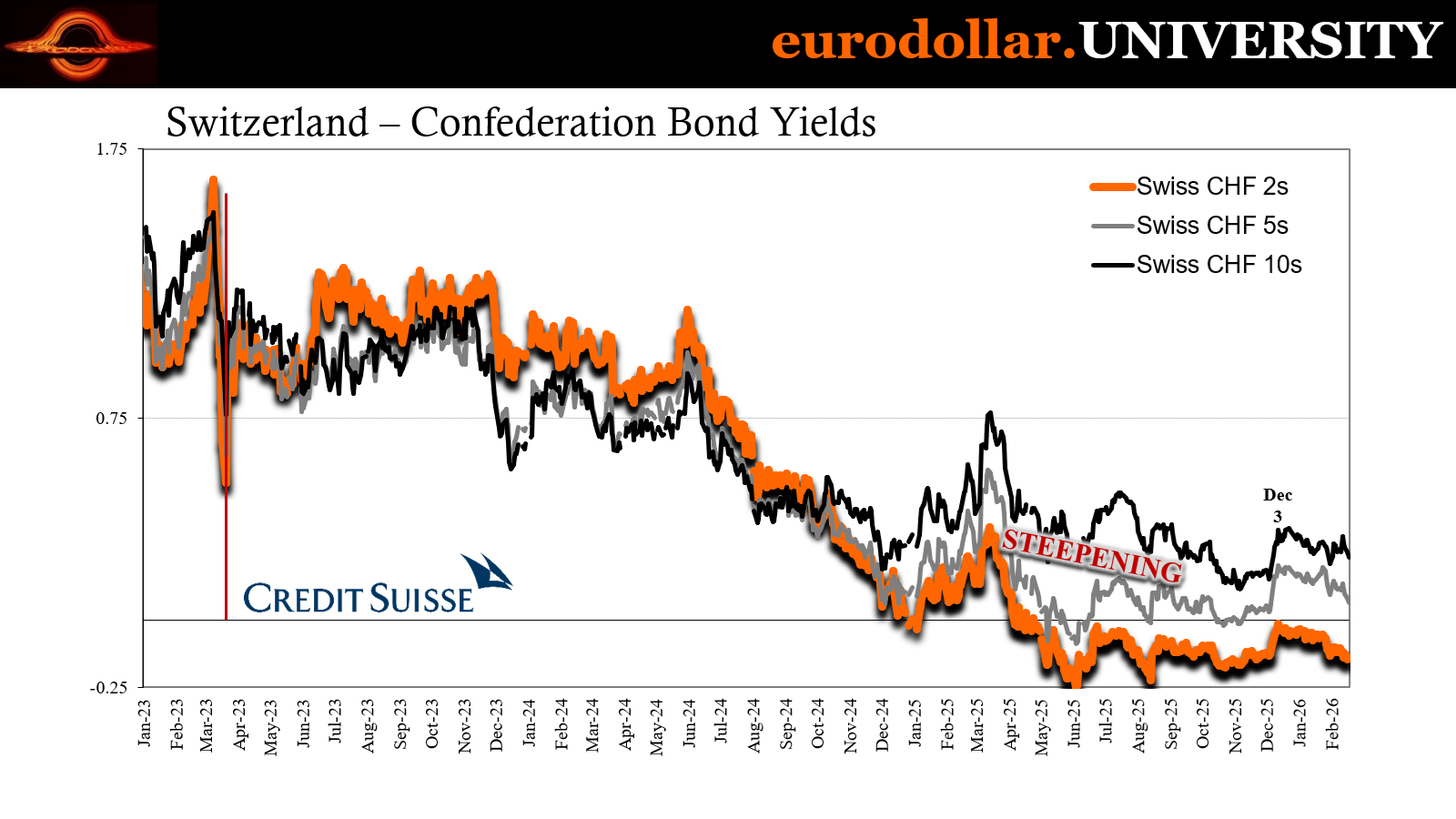

The Swiss certainly contributed some to that view. Swiss bond rates had moved back from the brink of total curve negative in roughly that same window: November to early December. In fact, Switzerland yields jumped just like Canadian rate did and were also equally short-lived on the upside.

By mid-December, they were moving back down all over again.

It was the same story for the Swiss economy. Roughed up by tariffs, a rebound was also widely anticipated. Not just in the real economy, which was believed to be stabilizing by summer, but also a more determined upswing in consumer prices which before had been too regularly flirting with outright deflation.

Like other peers, the SNB all but signaled an end to rate cutting, too, having gotten down to zero policy rates in the middle of last year. While Martin Schlegel, head central banker, kept the door open for negative rates (mainly in relation to a stronger CHF), he constantly reminded everyone there was a very high hurdle to overcome in order to convince officials to go there.

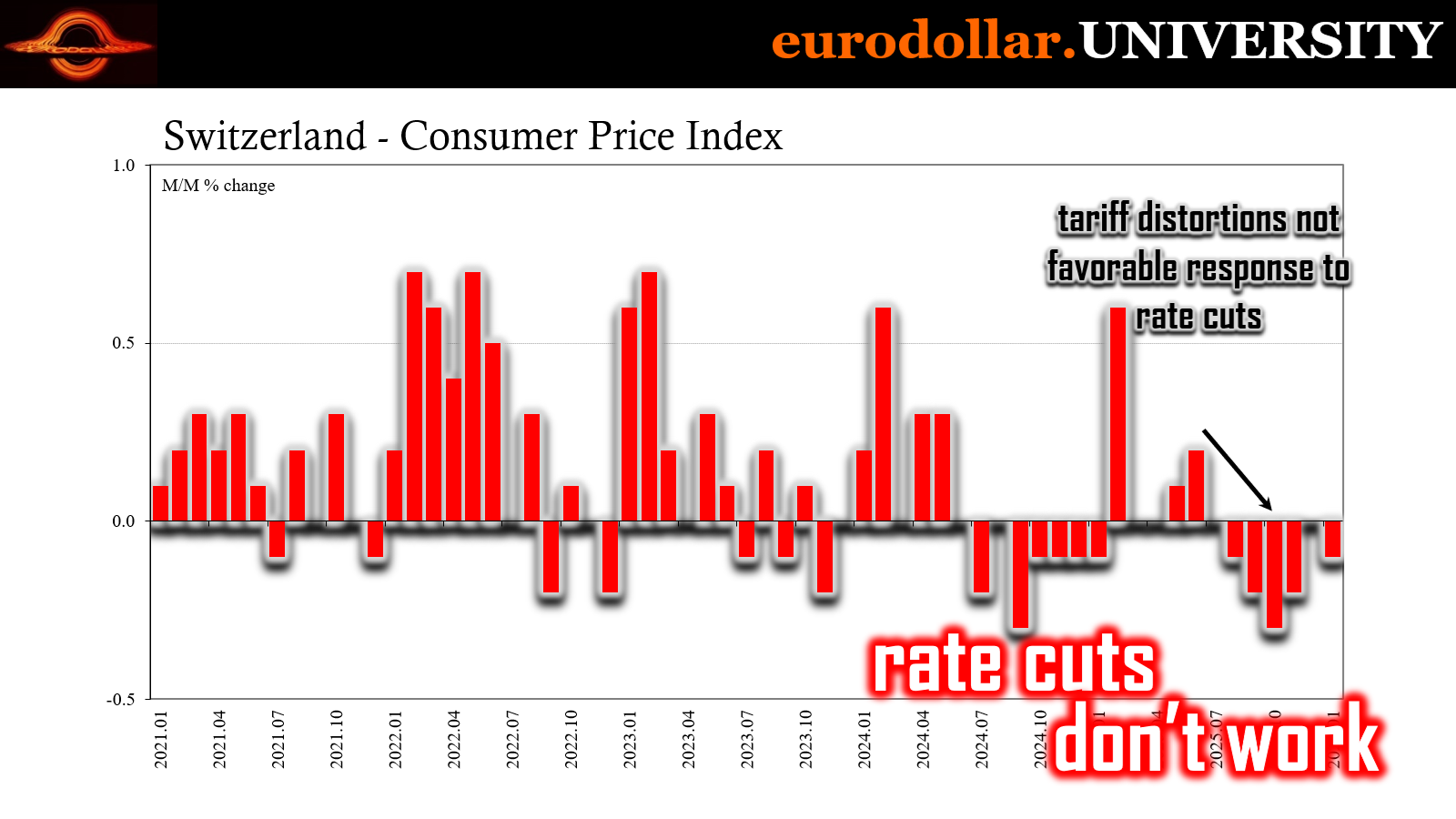

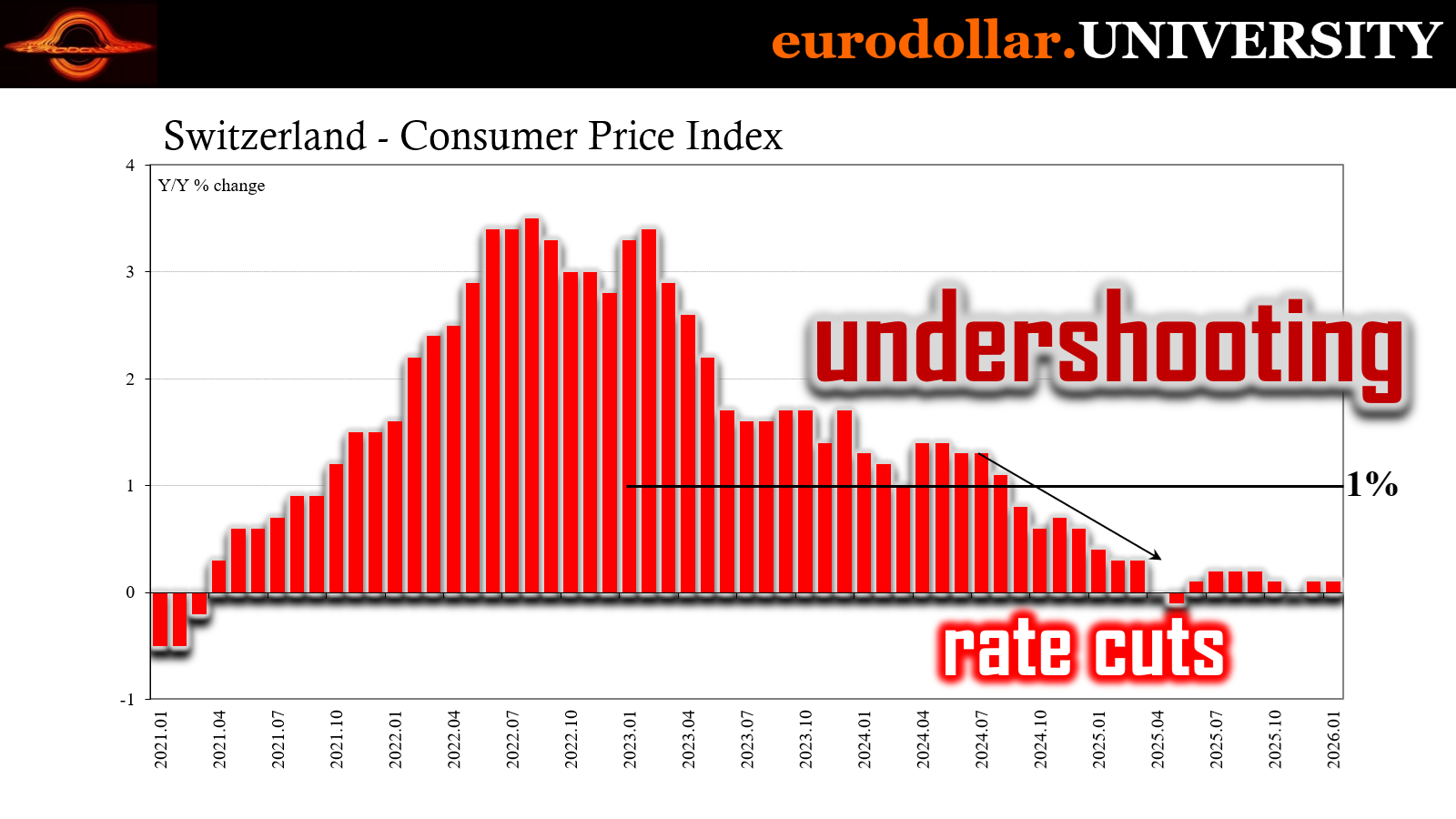

But then consumer prices kept on disappointing. Switzerland’s CPI was, at best, a zero and only in the month of December. January’s latest reading, just released, put it right back into the negative (-0.1% m/m), making five of the last six as such. Not only does that thwart any idea of reflation in pricing, it also further makes a mockery of rate cutting.

CHF continues to be unbothered by the SNB’s policy, at the same time consumer prices have shown no response at all to them, either. The absolute most anyone at the SNB or Economists can claim is that maybe it would have been worse without lower policy rates, the same “jobs saved” nonsense which officials are always forced to fall back on when inevitably rate cuts do nothing more than reflect economic conditions rather than affect them.

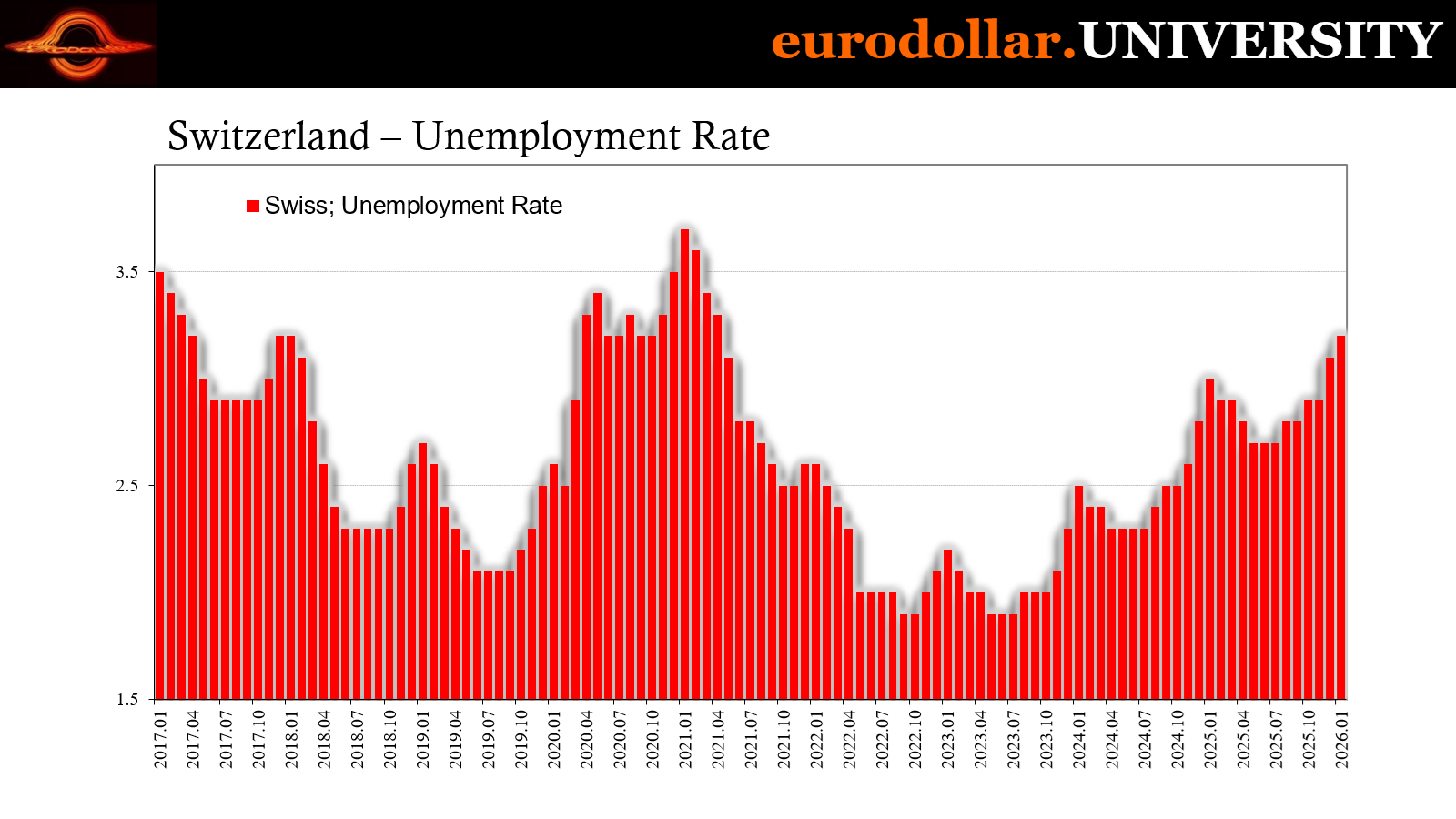

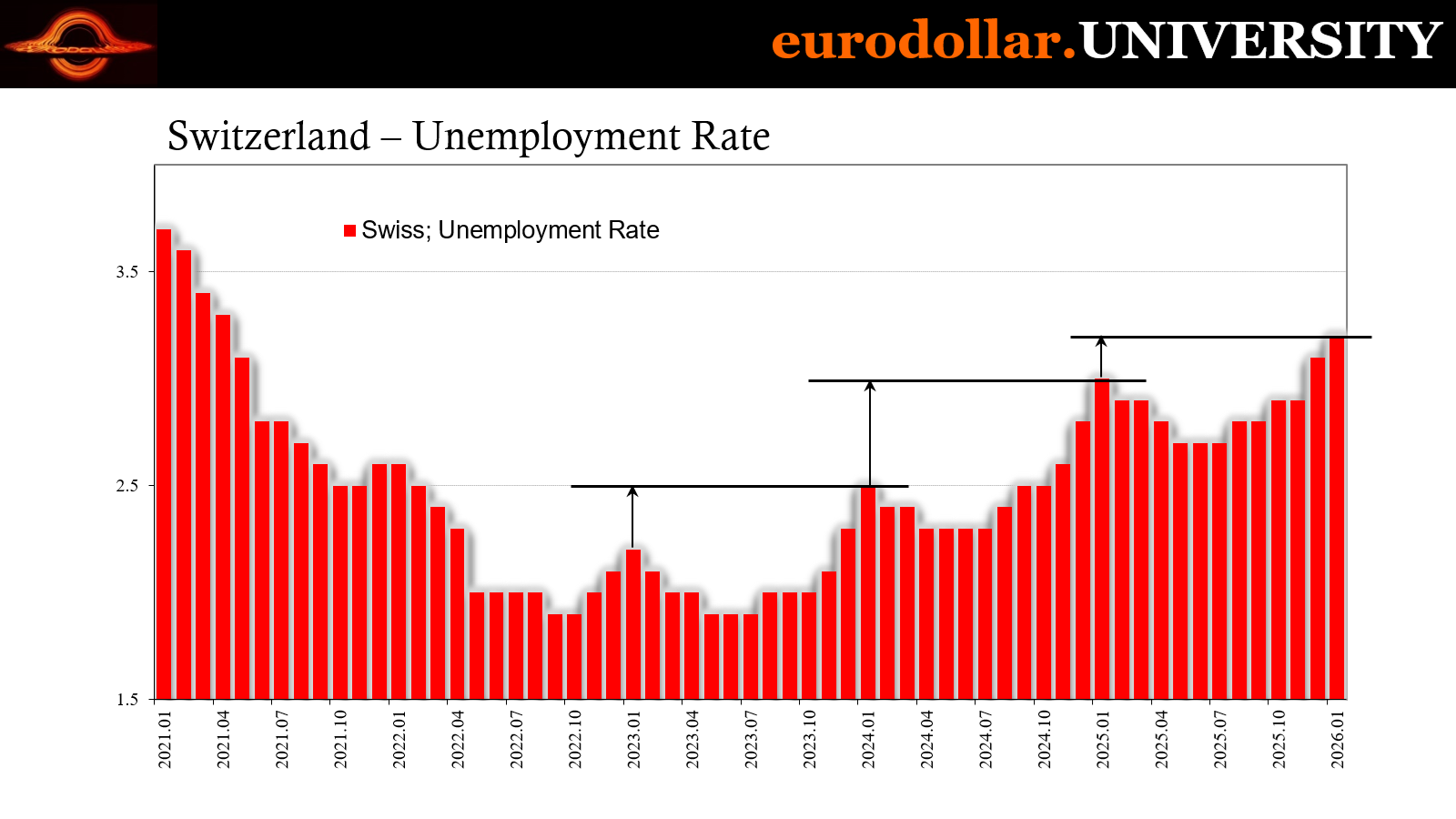

Of greater concern than the Swiss CPI, the country’s unemployment rate also defied expectations by rising yet again in January. Reaching 3.2%, that’s two-tenths higher than January 2025 and seven-tenths more than January 2024. But like the CPI and bond rates, there is no sign of any turnaround. Given that these new figures belong to January 2026, that means last year ended on a sour note which carried over to this year when it wasn’t supposed to.

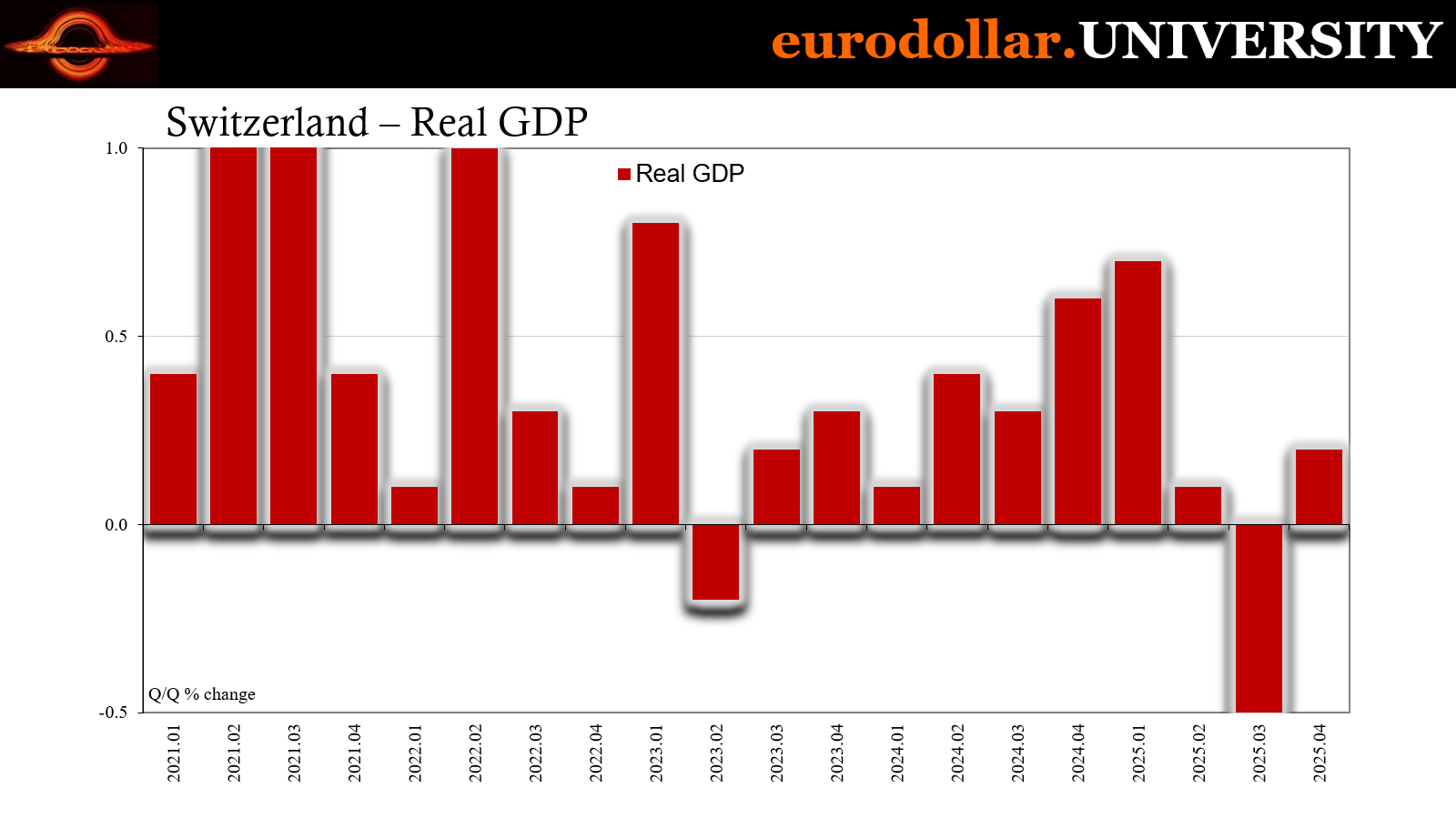

Even Swiss GDP did the same, though it at least managed to come in positive. Having fallen by a sharp half a percent (quarterly not annual rate) in Q3, output was only able to claw back 0.2% in Q4. And with barely any growth in Q2, just 0.1%, it makes three consecutive quarters for what amounts to a Swiss recession.

Unofficial, of course.

No one will dare use the R-word even though unemployment is steadily rising, consumer prices are steadily falling, the currency, a safe haven, is under steady demand, and bonds never truly unsteadied at any point beyond a fluctuation.

As a global bellwether, all those factors and results mean the end of the Pringles cycle took a huge hit.

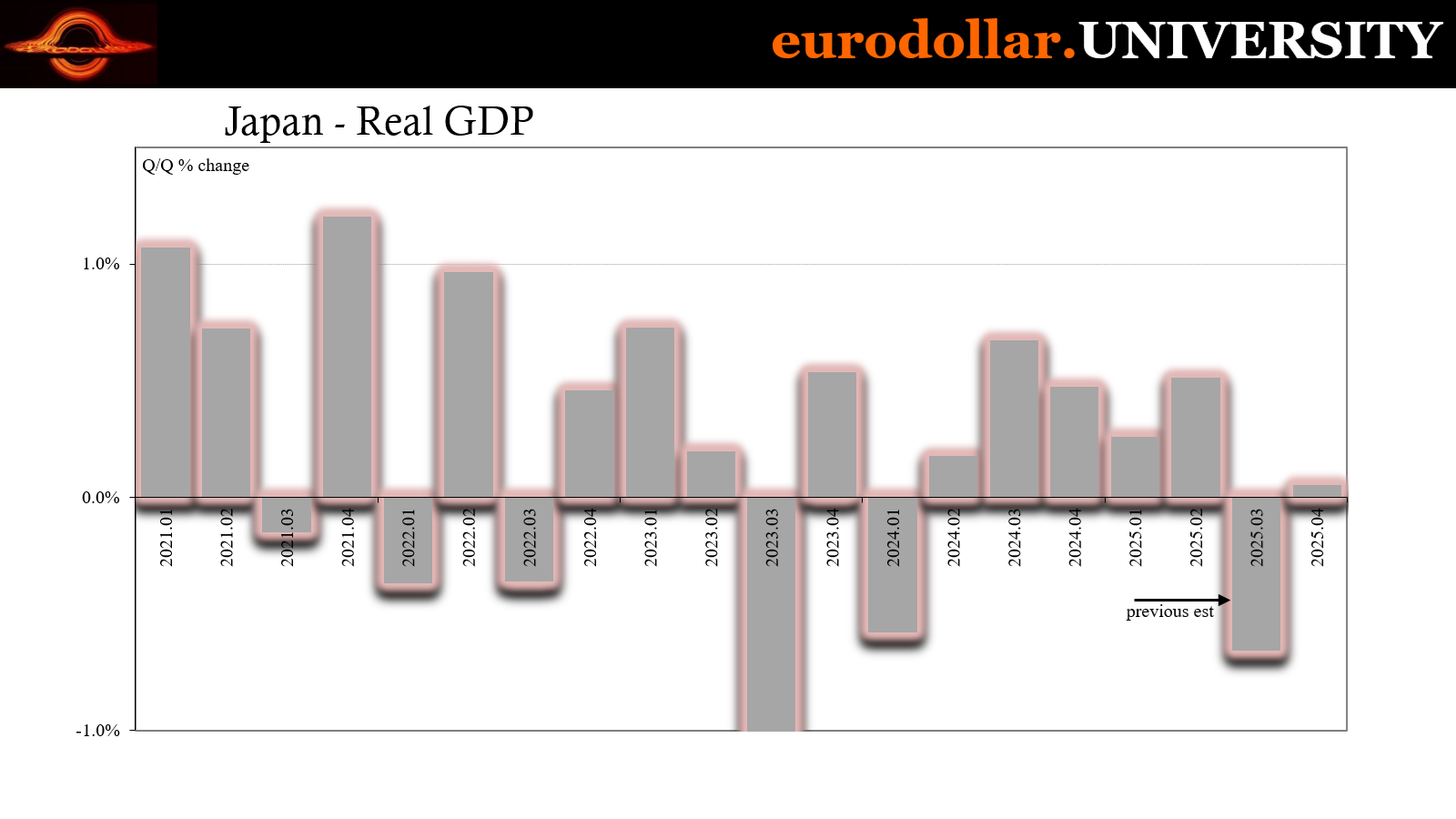

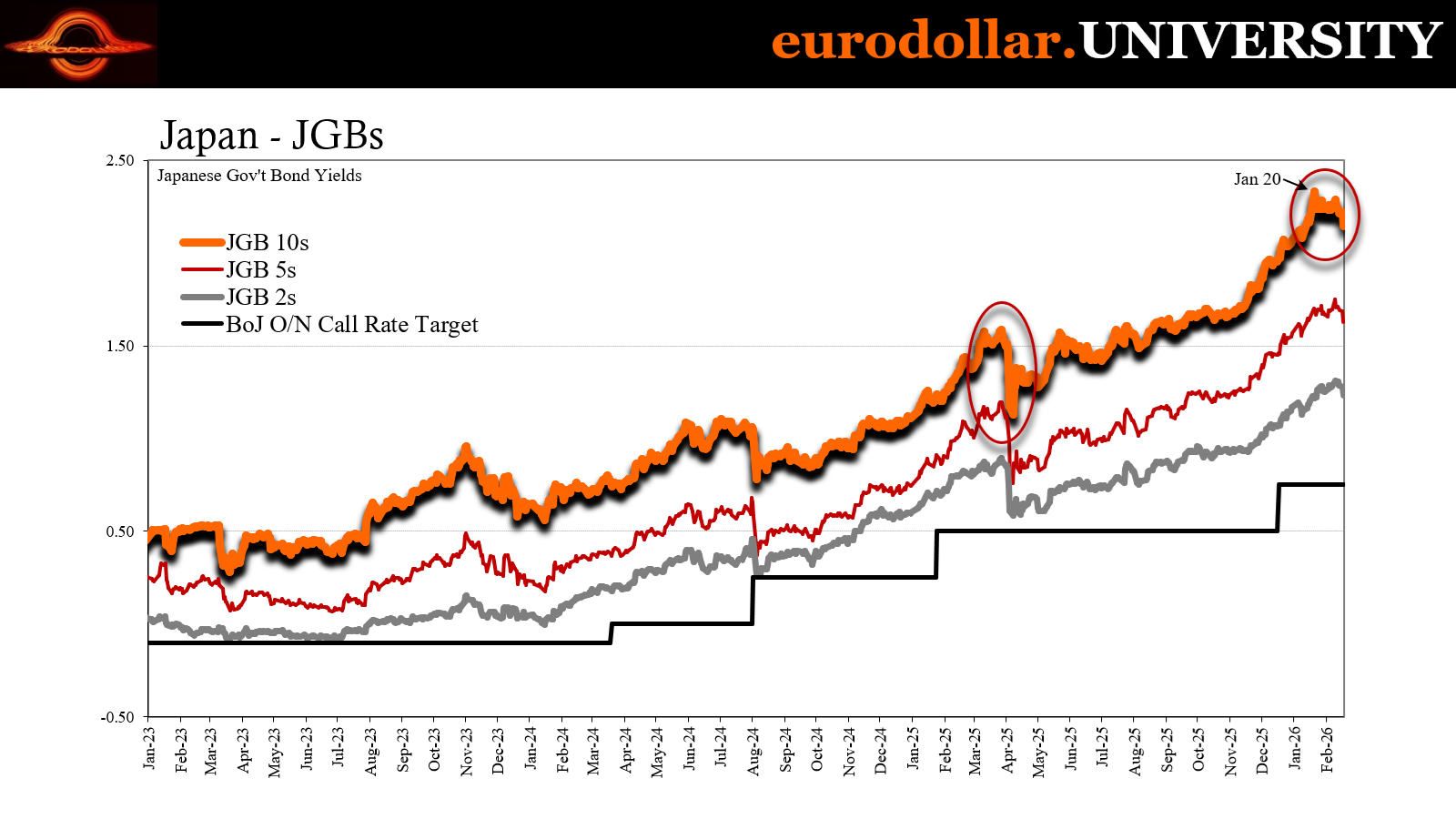

Japan re-re-re-re-re-recession

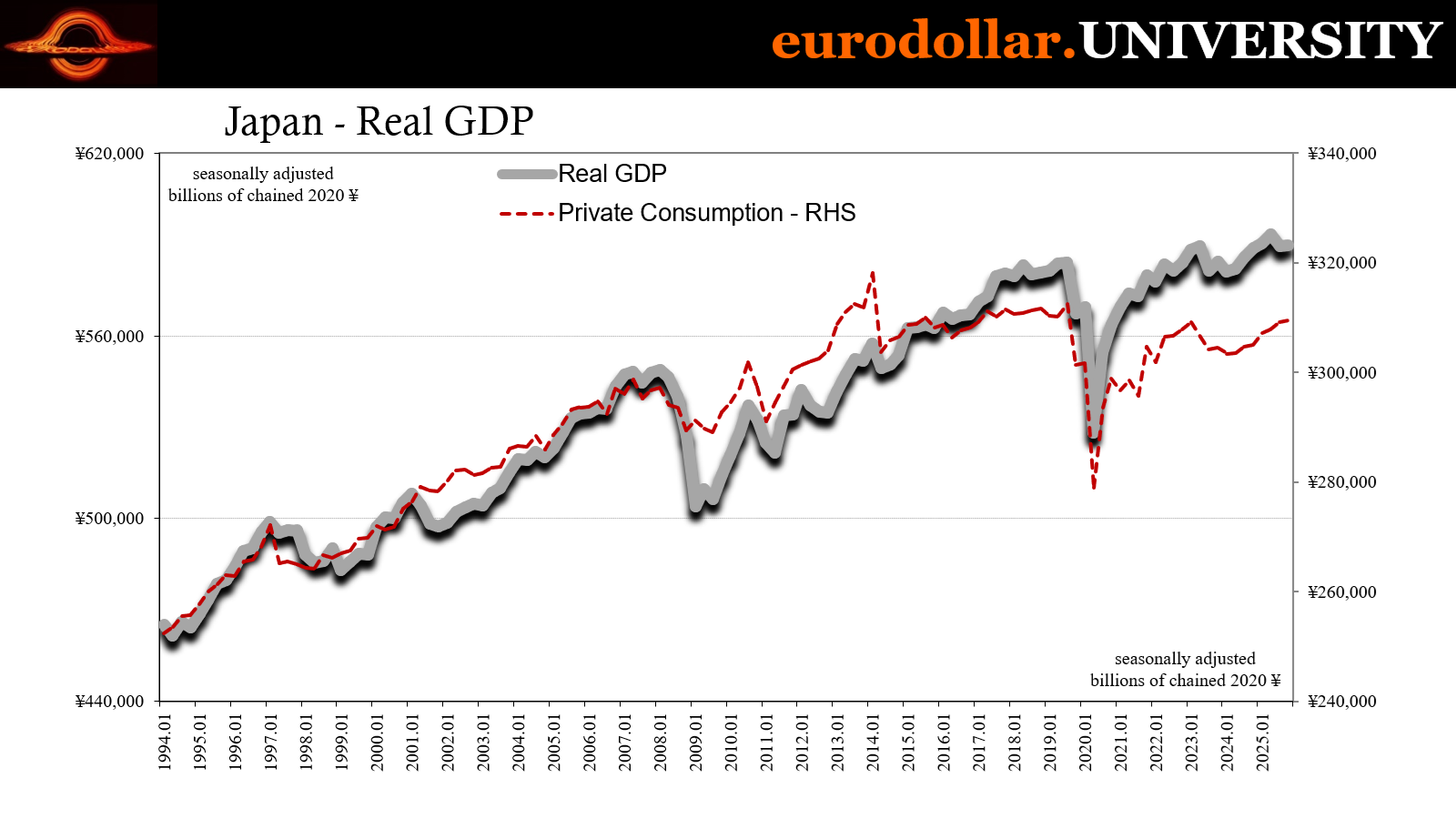

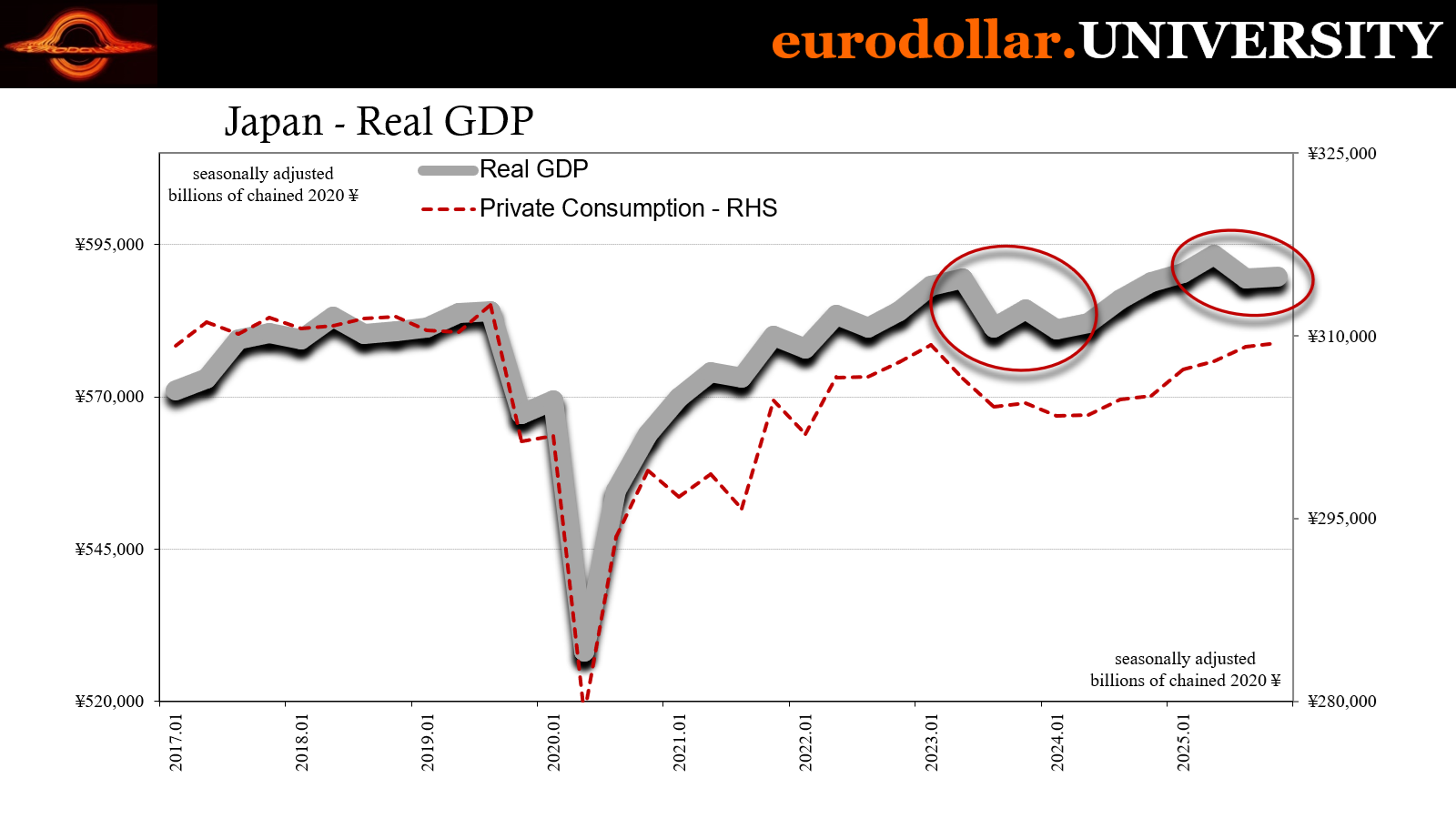

Similar to Switzerland, Japan has for all intents and purposes slid itself into a recession. According to the latest figures from the Japanese government, to start with GDP in Q3 2025 was much worse than originally thought, dropping 0.66% q/q (quarterly not annual rate) rather than the -0.44% q/q initially estimated.

Then Q4’s rebound fizzled almost entirely. While analysts were expecting a nearly equal bounce (+0.4%) to that original -0.44%, instead they got almost nothing (just +0.05% q/q) in the final quarter following the much bigger decline during the one before it. In other words, yep, another non-official recession in the land of household-spending-inflation supposedly right around the corner.

This should not have been a shocking surprise given how Q2’s half percent “growth” was obviously tariff-induced. The payback which has now emerged from it, however, is greater meaning any positive momentum was canceled out and then some by the end of the year.

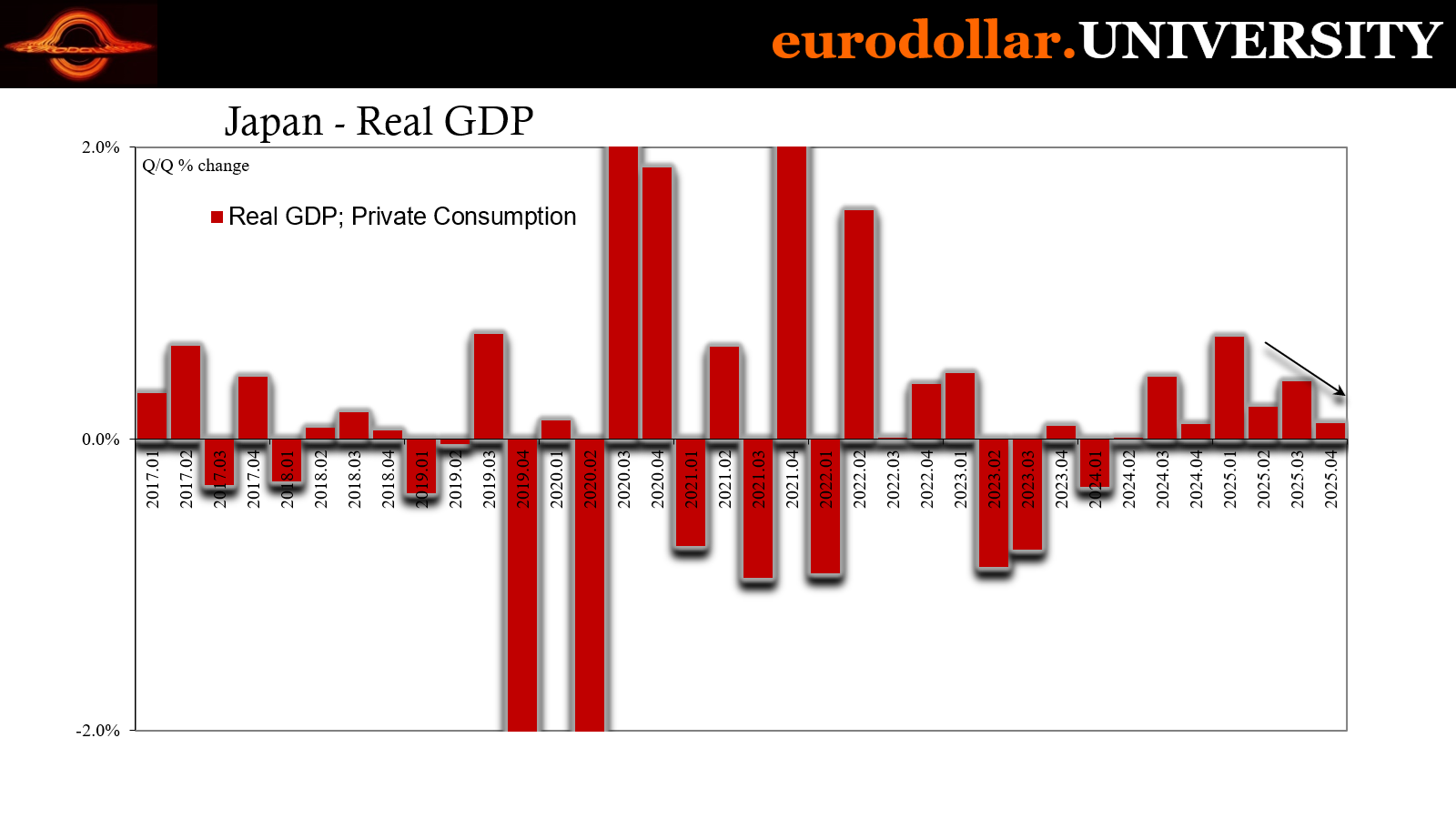

Weakness was led primarily by, as always, Japanese households. Like their American counterparts, spending due to tariff distortions faded into the end of the year right when it was widely expected to be picking up for fundamental purposes – those same ones as why everyone thought copper’s rise was something beyond supply factors.

Plus, with JGB yields soaring, for once correctly interpreting them as higher = reflation, there was at least some consistency in Japan unlike everywhere else, including CPI rates that while coming down aren’t yet coming down enough.

GDP pointing to a second half re-recession, on the other hand, puts some badly needed context behind the Japanese economy. Without any contribution from net exports (both imports and exports declined in Q4 at about the same rate), the only source of growth was business capex but only barely and like headline GDP it wasn’t positive enough to erase the negative from the quarter before.

Since January 20, now Japanese bond rates are coming back down. It’s the largest slide in them since last April. While it is far too early to say whether the buyers’ strike among pension funds and insurance companies might finally be reaching its end, the possibility is now put on the table with recession taking over the second half of 2025.

If Japan’s economy truly does follow through with even more deterioration ahead, eventually it would be enough to stop the rate hiking madness of Kazuo Ueda, allowing the JGB market to settle and buyers return, then, wholly contrary to the entire mainstream idea of rate hiking ahead, actually turn one of the few rate hikers around and put it more so on course to reverse into cuts instead.

Most commentary, of course, attributes Takaichi’s successful election gamble for this skid lower in yields after claiming before that her likely win was going to further disturb the bond market given her budget priorities on stimulating an economy the Bank of Japan is supposedly raising rates to slow down.

BoJ, as we know, is only trying to steady if not strengthen the yen while the government in Tokyo knows only too well how even if officials refuse to concede a recession they better do something about one anyway.

Japan like Switzerland is another critical global example coming up short on both late 2025 and so far of 2026.

Imagine that. Rather than the rest of the world edging closer to the RBA and hiking, one of the few that already are, BoJ, might not be all that far away from flipping into cutting, at least holding. Completely the wrong way for reflation and rebound this year.

Then again, it’s hardly just Japan. Where there was said to be emerging strength we only find instead rolling over. Not just in economic accounts, also in consumer prices, too. Forget tariff inflation, that’s dead, now the bigger and much more realistic trouble comes from the opposite side.

Unlike most mainstream sources, we’re not talking about a single datapoint or lone country. We see it in far more places and markets than not. The balance is shifting, alright, just not in the anticipated direction of travel.

Again, I didn’t even get to UK’s unemployment and CPI, nor China’s ugly banking data for January.

Pringles never went anywhere because, quite simply, the slogan works. Once they popped, they weren’t going to stop because far too much consistently indicated emptying the thing out from the beginning. Narratives change and supply factors fizzle, fundamentally it was what it was.