A FOUR HUNDRED BILLION SOMETHING

EDU DDA Feb. 20, 2026

Summary: Before the latest with Blue Owl, money dealers have been anticipating more with them and others. Basically, thinking ahead to Stage 2 even while most in the mainstream saw chances diminished or eliminated. After all, the repo mess of December appeared to have been successfully eliminated by January. Instead, this week has been a lesson in listening to those dealers. The Fed’s repo window came roaring to life, Blue Owl opened Stage 2, and the macro data (esp. incomes) proved nothing had changed in the “hiring recession” economy. All of it rewards what is a massive FOUR HUNDRED BILLION inventory of UST defensiveness.

DEALERS ARE THE MARKET

Blue Owl brought back the private credit downside seemingly out of nowhere, however there have been a number of broader developments which suggested nothing had really changed around the monetary scene despite the outward calm following December’s volatility.

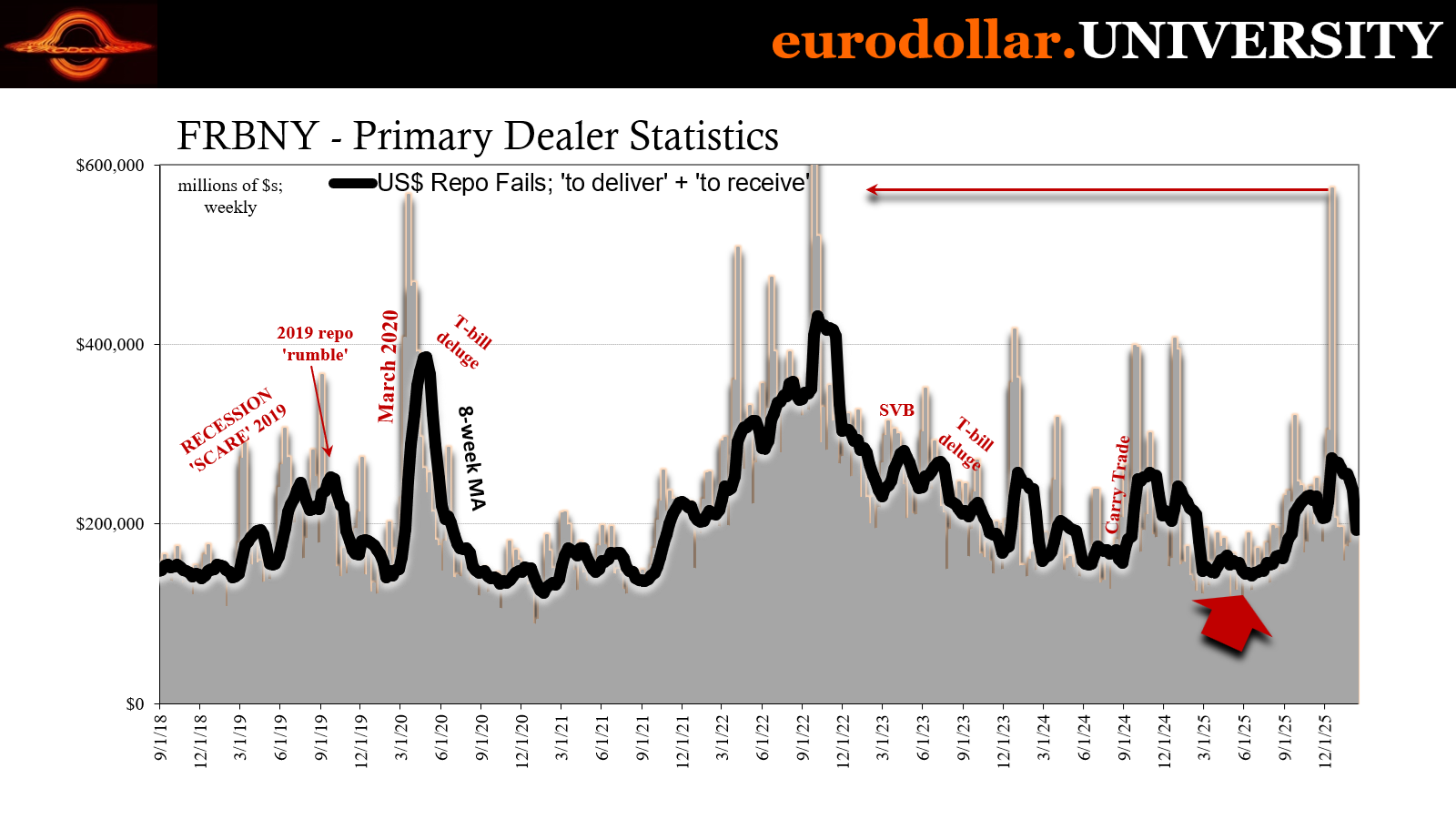

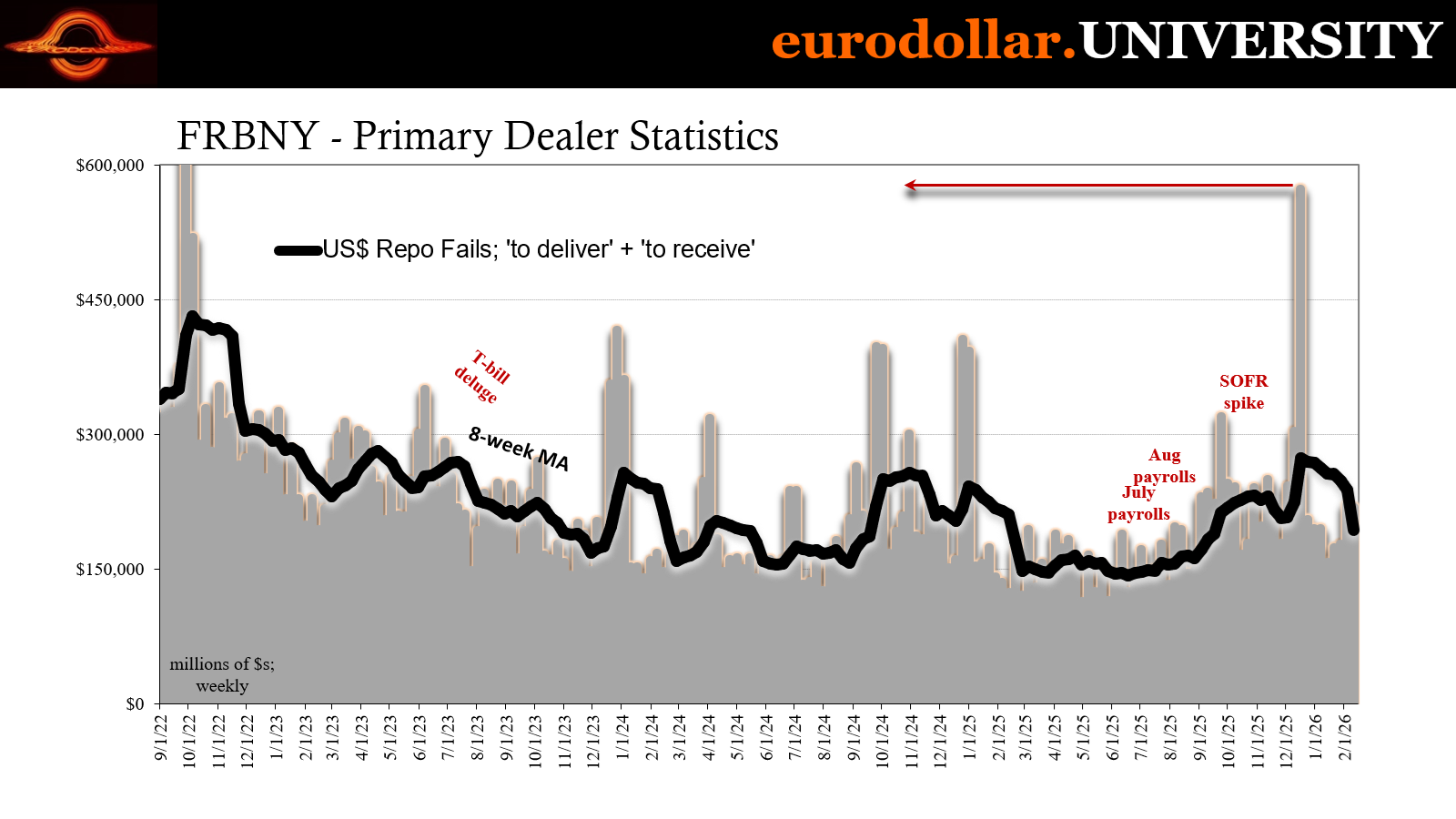

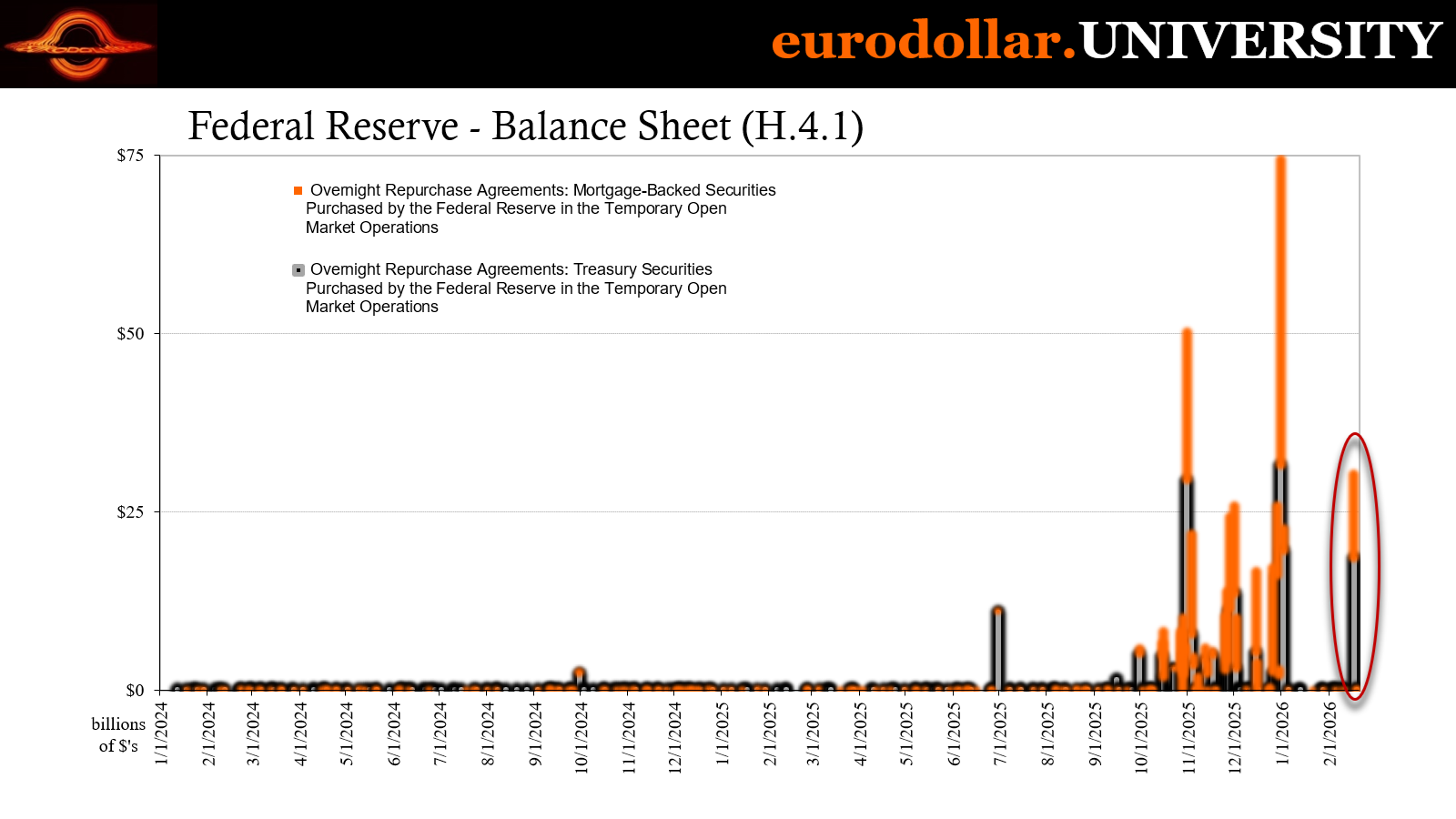

In repo, for example, fails soared then plunged. They are on the rise again (modestly). Repo rates were highly volatile during the fourth quarter, not as much to start this year (until this week). Even the Fed’s repo facility seemed to validate the not-QE of bank reserves before on Tuesday all of a sudden a huge $30 billion takedown from it.

The start of 2026 seemed like the system had turned a page thanks to Jay’s balance sheet, calm on the surface yet building up below there was major anxiety from within expressed in several ways, mainly in the collateral inventories of primary dealers. They began accumulating Treasuries in October, accelerating the trend in early December, and, in spite of everything else suggesting calm, dealers never stopped piling up bonds (and bills).

On the contrary, they went crazy for them.

That means well before this past week and its $30 billion Fed borrowing or Blue Owl’s no-good-very-bad day opening the door to Stage 2, dealers saw this coming and were preparing(ed) for it. At these levels, though, they can’t be satisfied with just those.

In other words, primary dealers are looking for more Stage 2 beyond just the $1.4 billion forced owl selling.

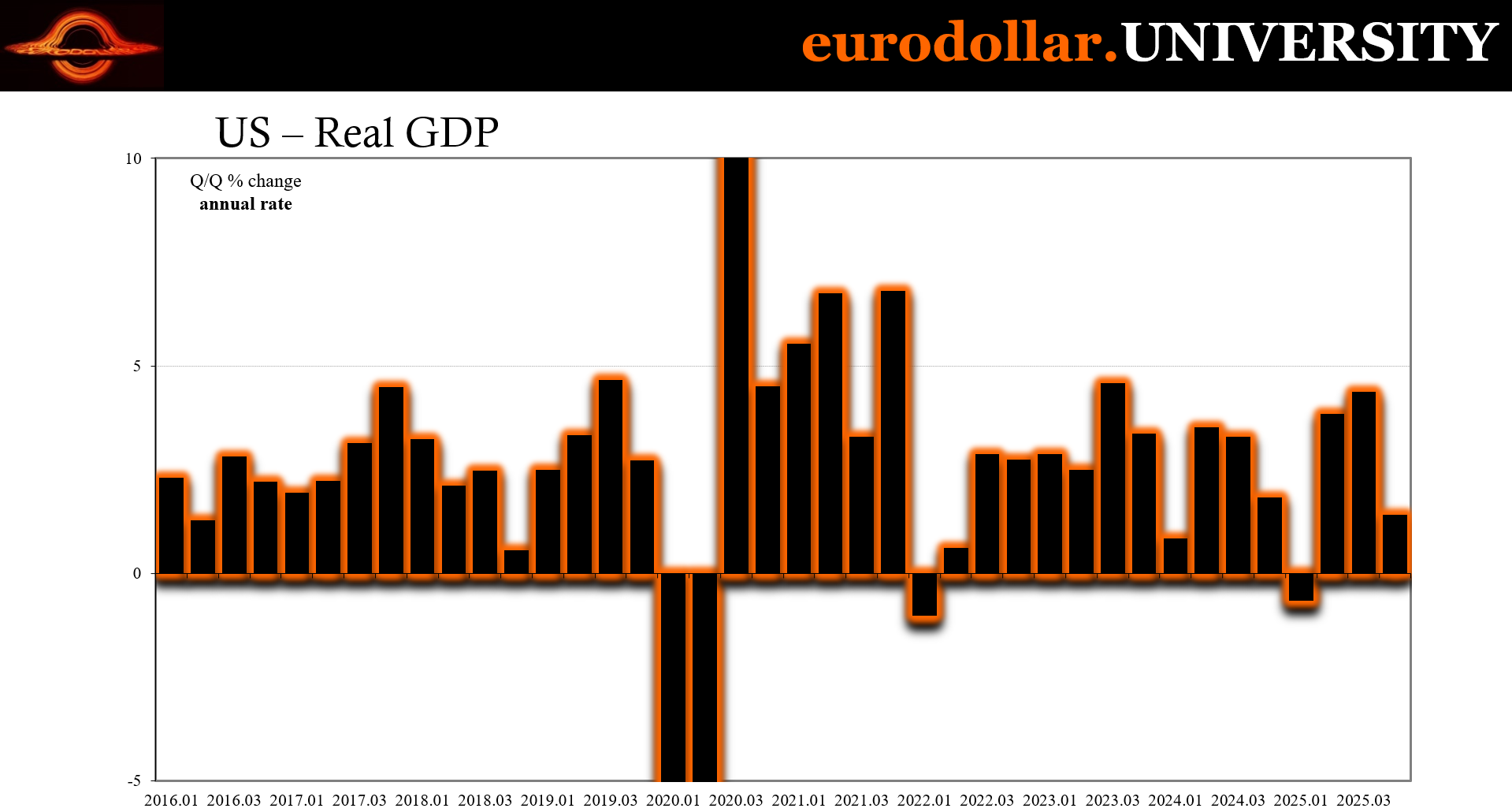

Today’s economic data releases are more good reasons for why that would be. GDP was far below expectations, sure, but it’s the income numbers (therefore personal savings). Going by those, Walmart’s CFO was right to flag the risks ahead from the “hiring recession” which was much more than evident across the income data.

Workers and consumers keep falling behind which easily leads to borrowers (including companies) doing the same on payment obligations; therefore, more Stage 2 behavior than the one documented case we have now.

Dealers aren’t at $413 billion in their Treasury holdings thinking the economy is about to soar and private credit easily cured with just a few more months. It’s the combination of flatter Beveridge and more Blue Owls swirling the downside bubble drain, or really how the former will only lead to the latter.

Never not incomes

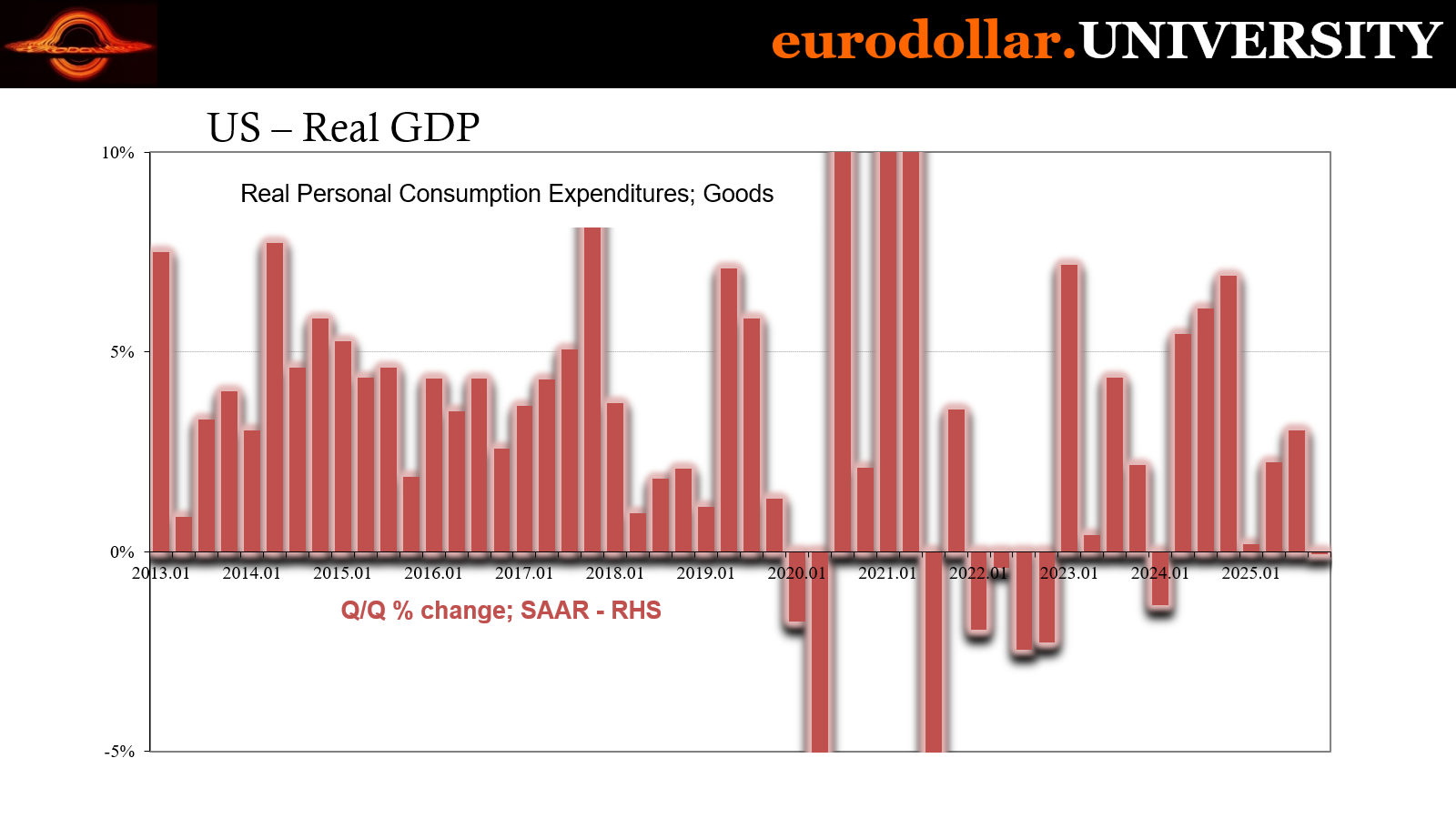

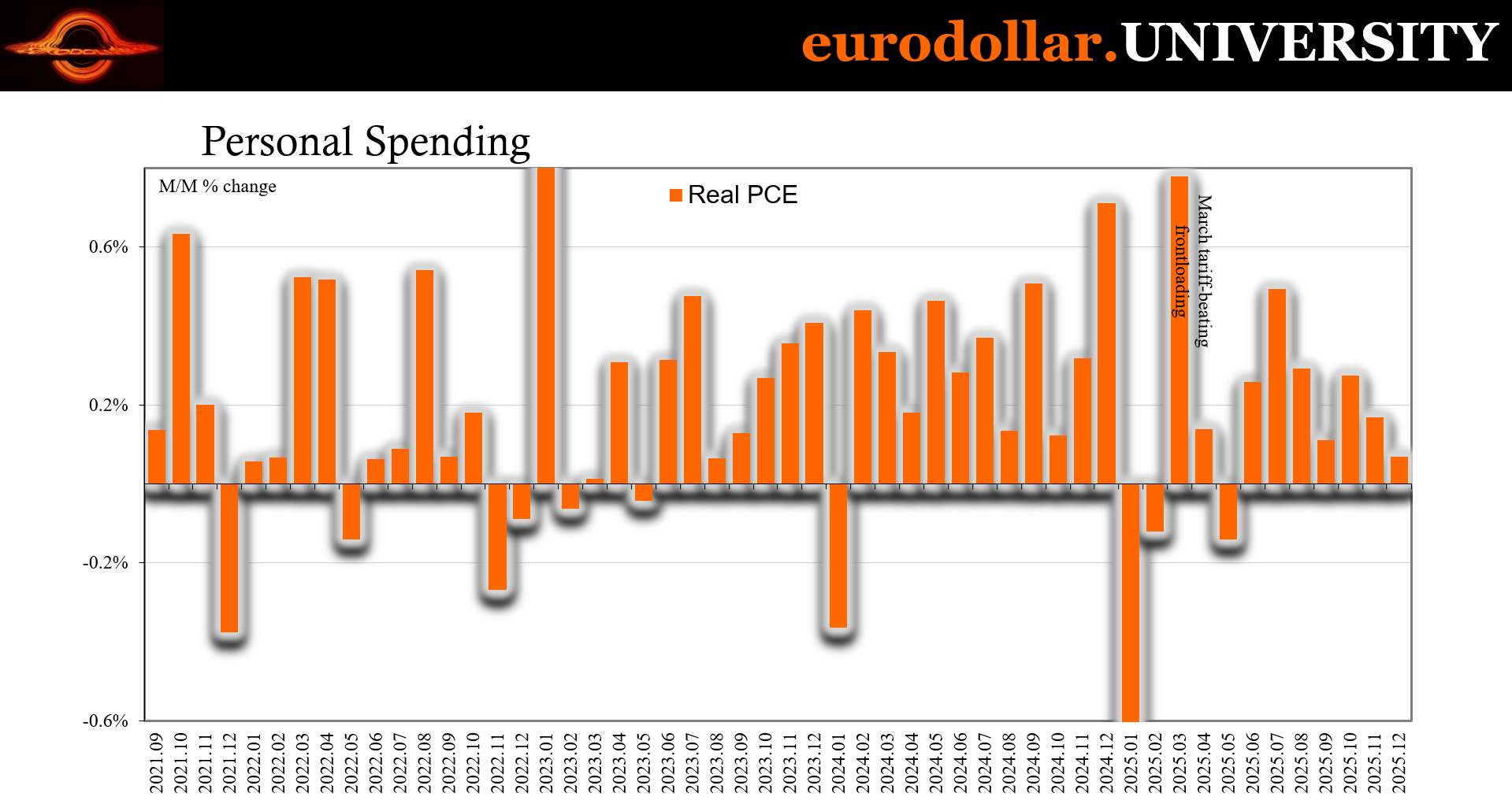

GDP growth slowed to just 1.4% q/q (annual rate) largely as the government shutdown subtracted 0.9 pts from the headline rate. The far more pressing and lasting issue was the slowing consumer environment which saw the goods economy in recession during Q4; PCE for goods fell one-tenth mainly as payback in the auto sector depressed activity.

That means the jump in purchases during the second and third quarters was not the big rebound everyone had been clamoring for, a reality auto manufacturers knew only too well which is why vehicle production slid sharply to end last year (see: IP, MVAS).

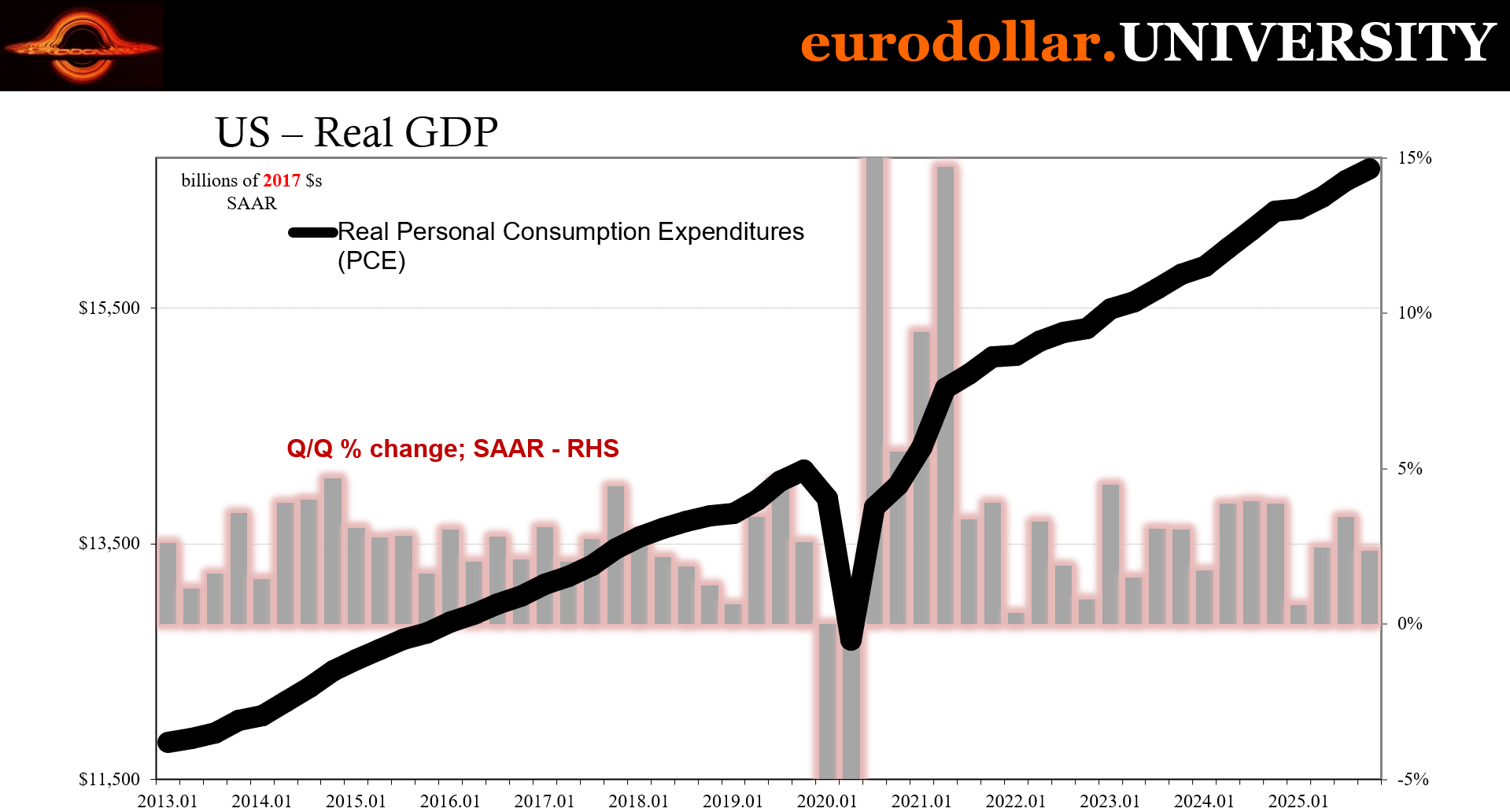

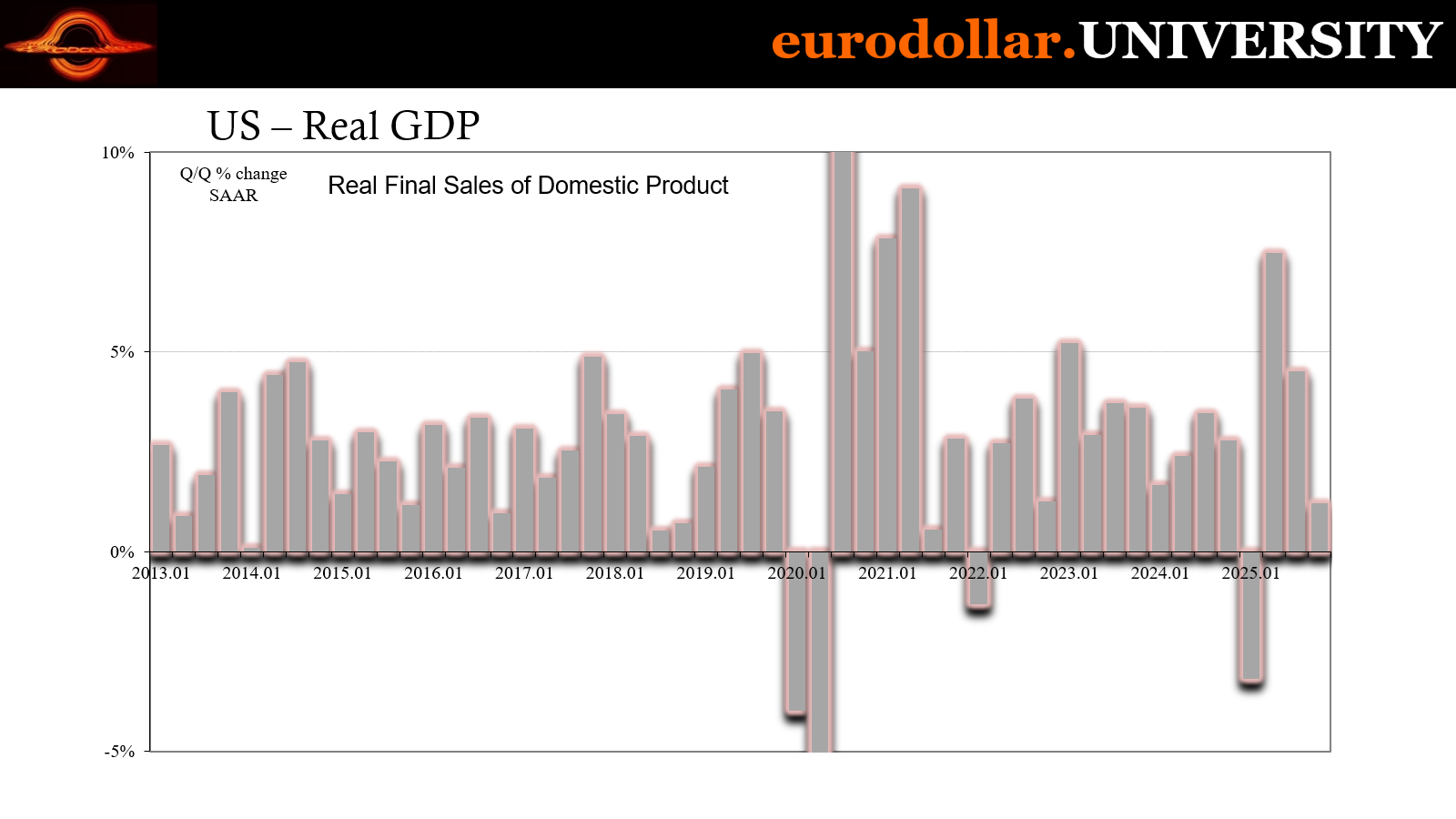

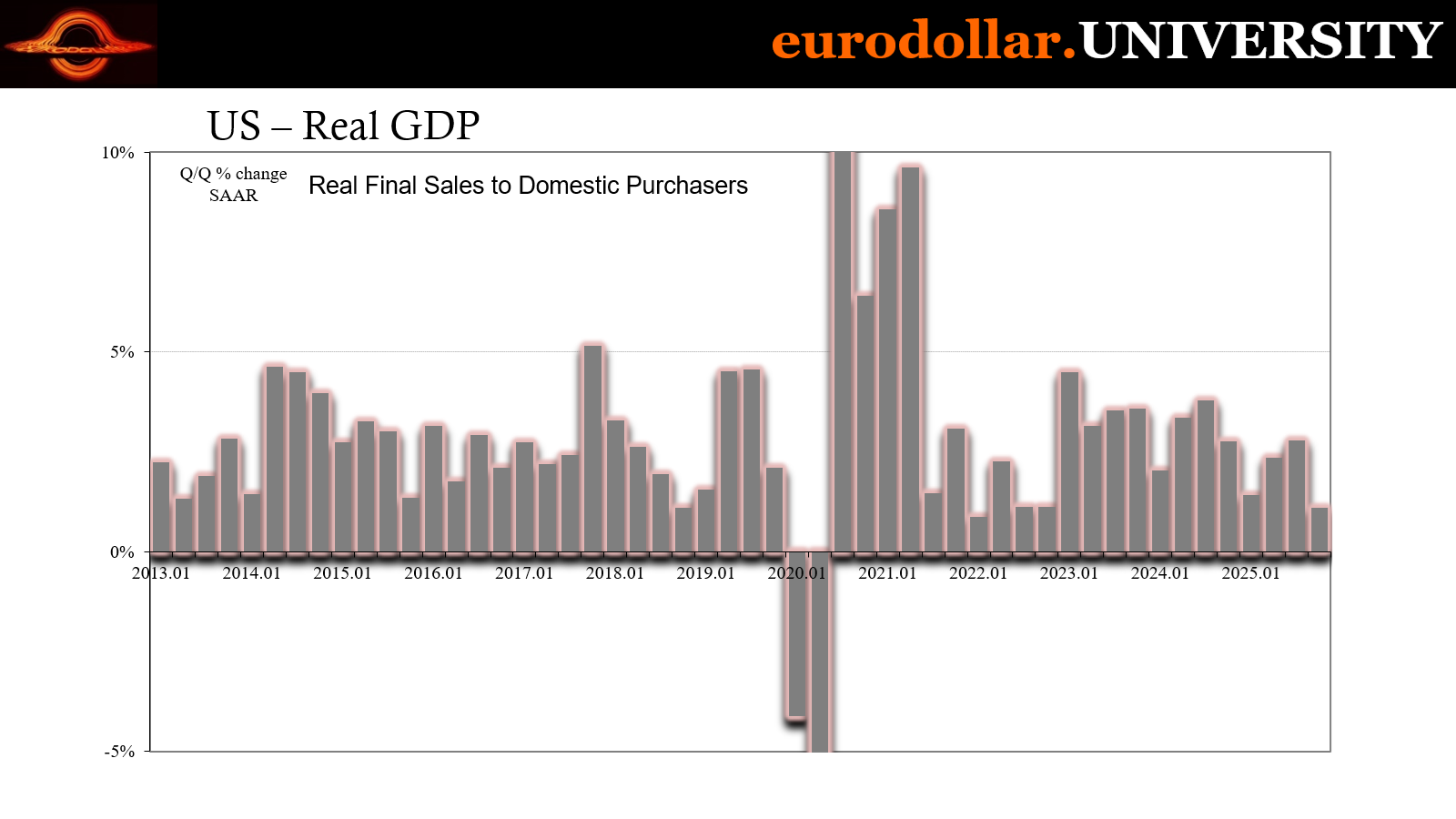

Services spending was steady, yet slowed, too. As a result, real final sales to domestic purchasers came in at barely 1%, the lowest quarterly change going back to the first quarter of 2022. Final sales of domestic product were similarly low given the downside in exports. The AI bubble’s impact on investment wasn’t nearly enough to fully offset the widespread weakness even before the October/November holiday in DC.

While most will focus on the government shutdown and its impact, the consumer side of the economy is the real story – as the CFO of Walmart was attempting to explain.

And that feeds directly from incomes which come from the lack of jobs, the hiring recession threatening to further negatively impact everything from spending to more risky portfolios than those run by Blue Owl. Quite simply, real incomes are still contracting. Falling further behind.

This is not some shocking surprise, except to those who believe in the Boom-cession; the latest media spin on how the economy can look so good via stats like GDP (oops) and at the same time so bad from particularly the perspective of job counts. Except, it isn’t just whatever tally of the number of employed positions, the income data shows the downturn is having further effects while refusing to turn around.

What spending there has been largely comes from the stock market, lingering wealth effects concentrated very narrowly from past soaring shares held to a small wealthy minority. That compares to the vast majority with little if any financial assets who are subjected to those shrinking real incomes.

The dangers Walmart’s management describe are therefore twofold.

MAYBE IT’S BECAUSE THEY DON’T ‘FEEL’ IT SINCE THERE IS NO BOOM

First, the wealthy who have been shopping might stop doing so if the NASDAQ can’t manage to shake off its current funk. Second, much more concerning, the “hiring recession” only deepens which would mean even if higher-income Americans keep spending lower-income consumers pull back even more than they have and far outweigh them.

The income data doesn’t just show the contraction of some prior hiring recession. Like the jobs data, too, the contraction kept right on going through the end of last year with no pivot in sight. On the contrary, December was yet another bad month.

The income numbers aren’t catastrophic, there is no plummet off a 2008-style cliff. Yet, contrary to most impressions, this is a contraction nonetheless with only growing danger the longer it continues – what specifically upset WMT.

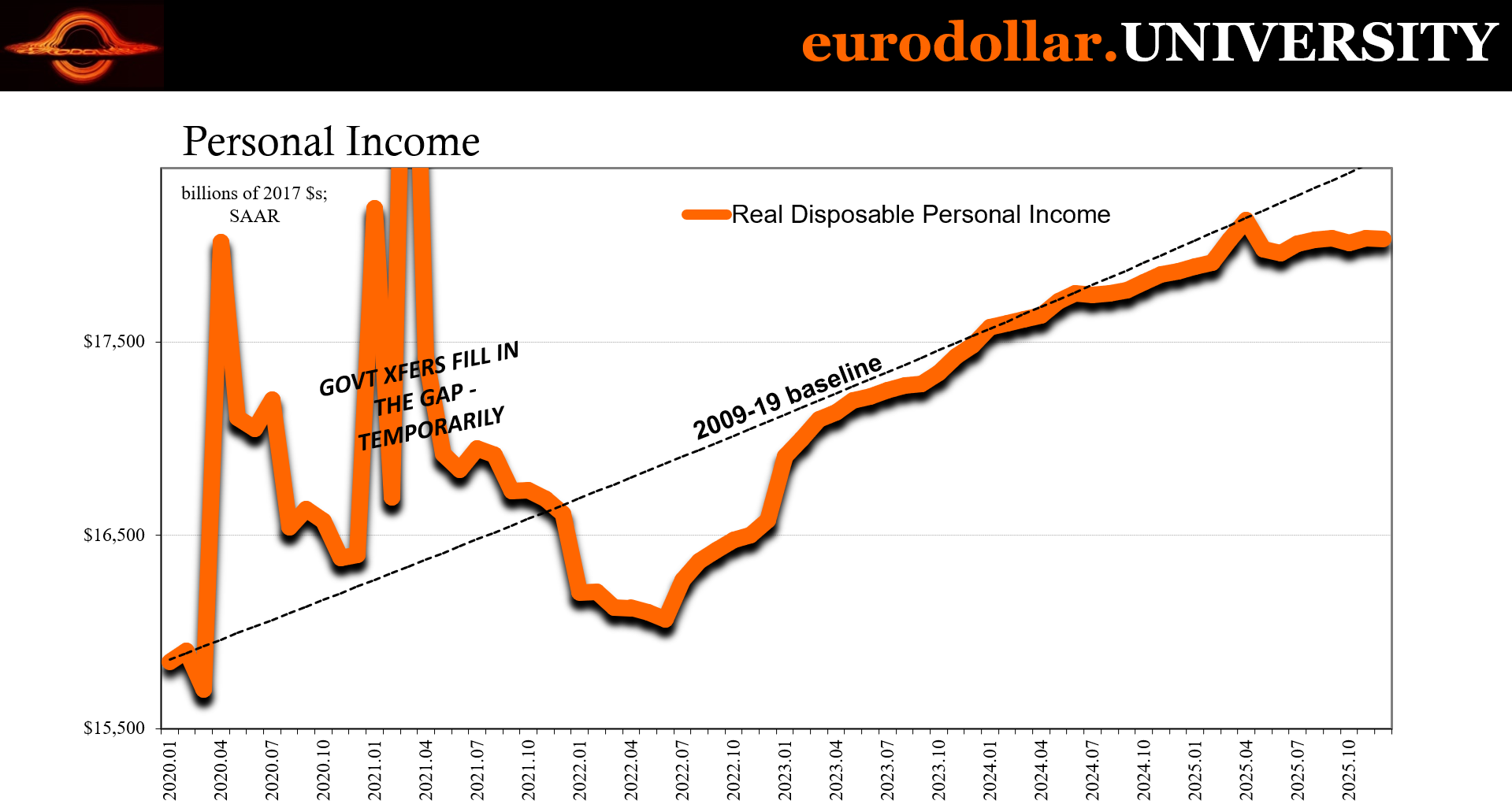

For December, real disposable income was slightly lower, falling 0.03% on the month. Excluding transfer receipts, private income was down 0.13% m/m. It was the second negative just in the fourth quarter, with November’s small 0.18% increase not enough to offset the other two leaving real income down for all of Q4.

It was also the fifth negative for the series over the final eight months of 2025. Since the deflationary chaos of April, real private income is down 0.3% and barely changed compared to a year ago. Maybe not catastrophic, still grim and alarming anyway.

Even spending itself was thin. PCE appeared better in the GDP data mainly due to October’s 0.27% m/m gain. Consumption slowed from there, only 0.17% in November and then almost zero, just 0.07% for December. That matches the retail sales figures, to an extent, pointing to not just a Christmas bust, more importantly last year ending with a thud rather than a determined bounce on the spending side.

Yet, despite the slowdown in outlays, because incomes have been so consistently poor and falling behind, the savings rate slipped even more, reaching just 3.6% in December. Once again, you can see why Walmart and other consumer-related business (General Mills!) are being prudently cautious on this year.

And also why money dealers are doing what they’re doing despite everything else which supposedly went right.

In the background

We know all about the repo mess which began to make itself more visible around mid-September when the first real draw on the Fed’s facility was taken. SOFR rates started to rise around then, too, but more importantly they grew more volatile which is what this is all really about. It isn’t necessarily rising rates, primarily the growing possibility for disruptions, disorderly liquidity, overall unpredictability in key funding.

It only got worse October to November before December displayed very clear dysfunction. We covered them at the time: on the cash side, more borrowing from the Fed and greater volatility in SOFR and other repo rates; on the collateral side, the explosion in repo fails plus the burst of additional demand for bills, including those in Japan (telltale collateral signal).

Such clear disarray convinced the FOMC to go beyond merely ending QT and go ahead with a restart to not-QE before mid-December.

After some more fireworks to close out 2025, everything seemed to calm down in January. SOFR was tame, no one bothered the Fed’s repo window for weeks on end, repo fails slid back to normal levels. It appeared as though Jay Powell was right about the whole thing; it really had been bank reserves and therefore not-QE creating a few more of them did the trick.

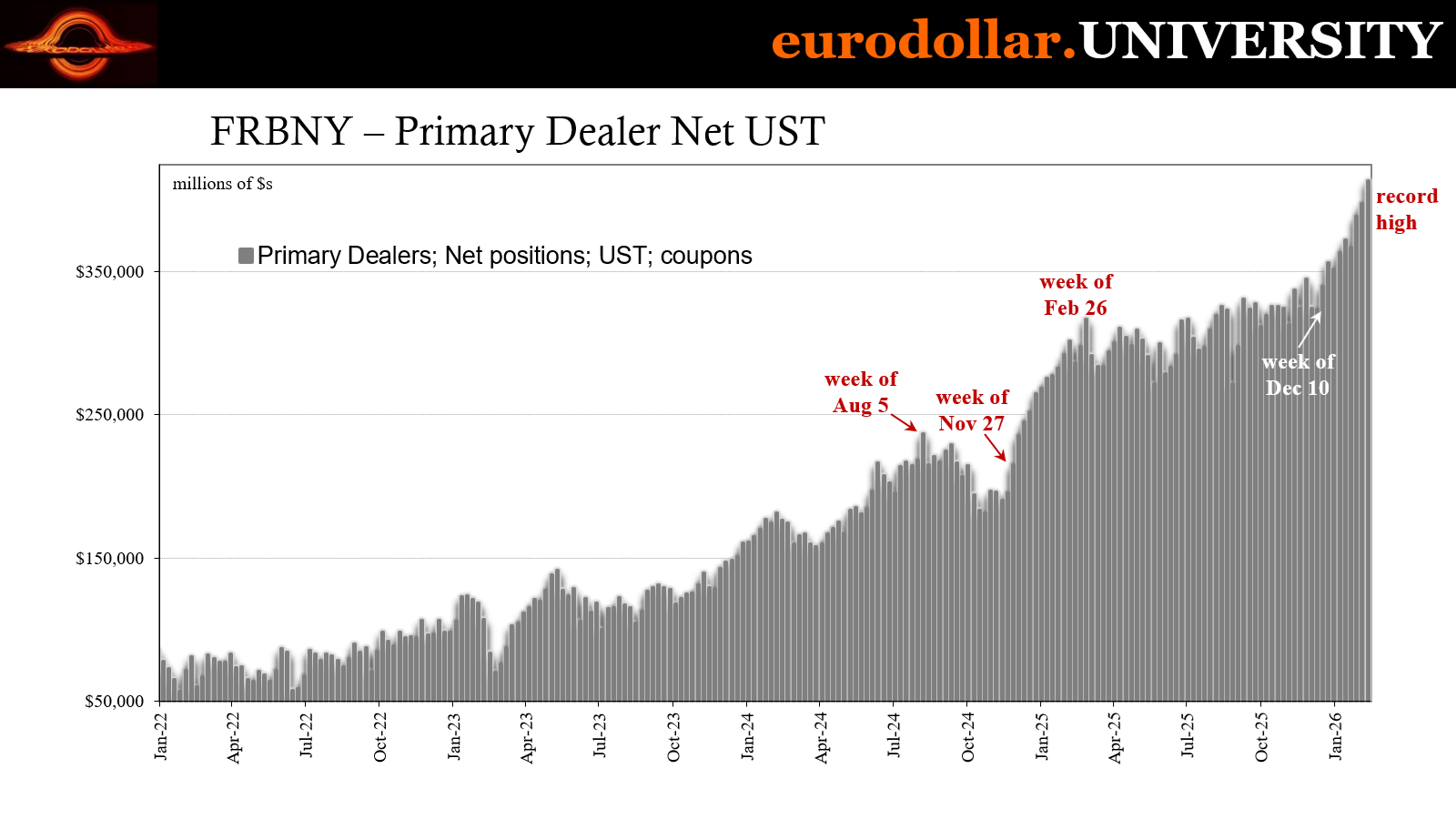

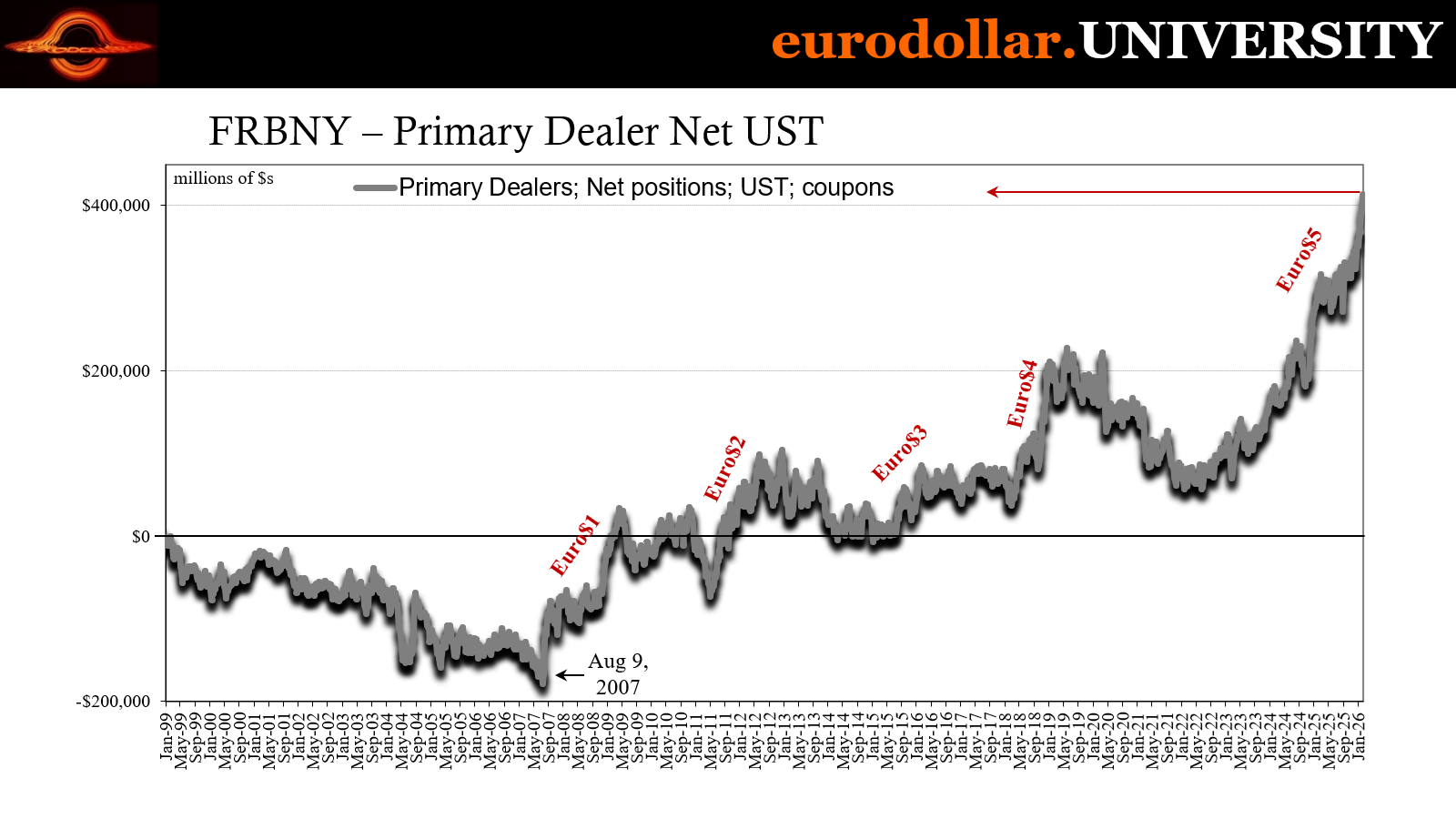

Except, behind the scenes, in the repo market itself, primary dealers (and presumably more eurodollar money dealers) weren’t seeing it that way. Not at all. These banks had already built up a record surplus of Treasury holdings before last fall, especially from late in 2024 anticipating the chaos of March and April 2025.

While the rest of the world thought the system had shaken off “tariff uncertainty” by last summer, dealers sure didn’t see it that way, still holding near-record Treasury inventories. As the cockroaches began appearing alongside flat Beveridge confirmation, they started to pile on even more government bonds.

But it really went crazy in early December. The first week, the total of coupons (notes and bonds, we’ll get to bills in the next section) was $324 billion. By the end of the year, it had climbed to $351 billion and a new all-time high. As repo and money appeared to calm down by other metrics in January, and maybe the market did, dealers weren’t seeing it as a real movement, or at best thinking the peace wouldn’t last long.

By the end of January, inventories had soared to $388 billion. As of the latest figures for the week of February 11, the week before this one with the updated owl, holdings soared again, reaching an astounding $413 billion. So, no, as far as the base of the repo market was concerned, these dealers weren’t seeing much if anything different from December. Negative potential never went anywhere even if the Fed “printed” a few more bank reserves along the way.

That means when Blue Owl broke this week, it was just all part of the anticipated consequences. As the company is forced to sell assets and close off investor withdrawals, the monetary system building up collateral holdings the entire time was just thinking ahead to more than this one fund entering Stage 2 behavior.

You could say this level of a Treasury stockpile was created for total Stage 2 (if not more, though we don’t want to get ahead of ourselves). It sure as hell isn’t the booming recovery everyone outside the monetary system has apparently convinced themselves must be taking place. Neither the data nor dealer behavior sees it that way.

In the case of dealer holdings, it isn’t just thinking.

Did bill know?

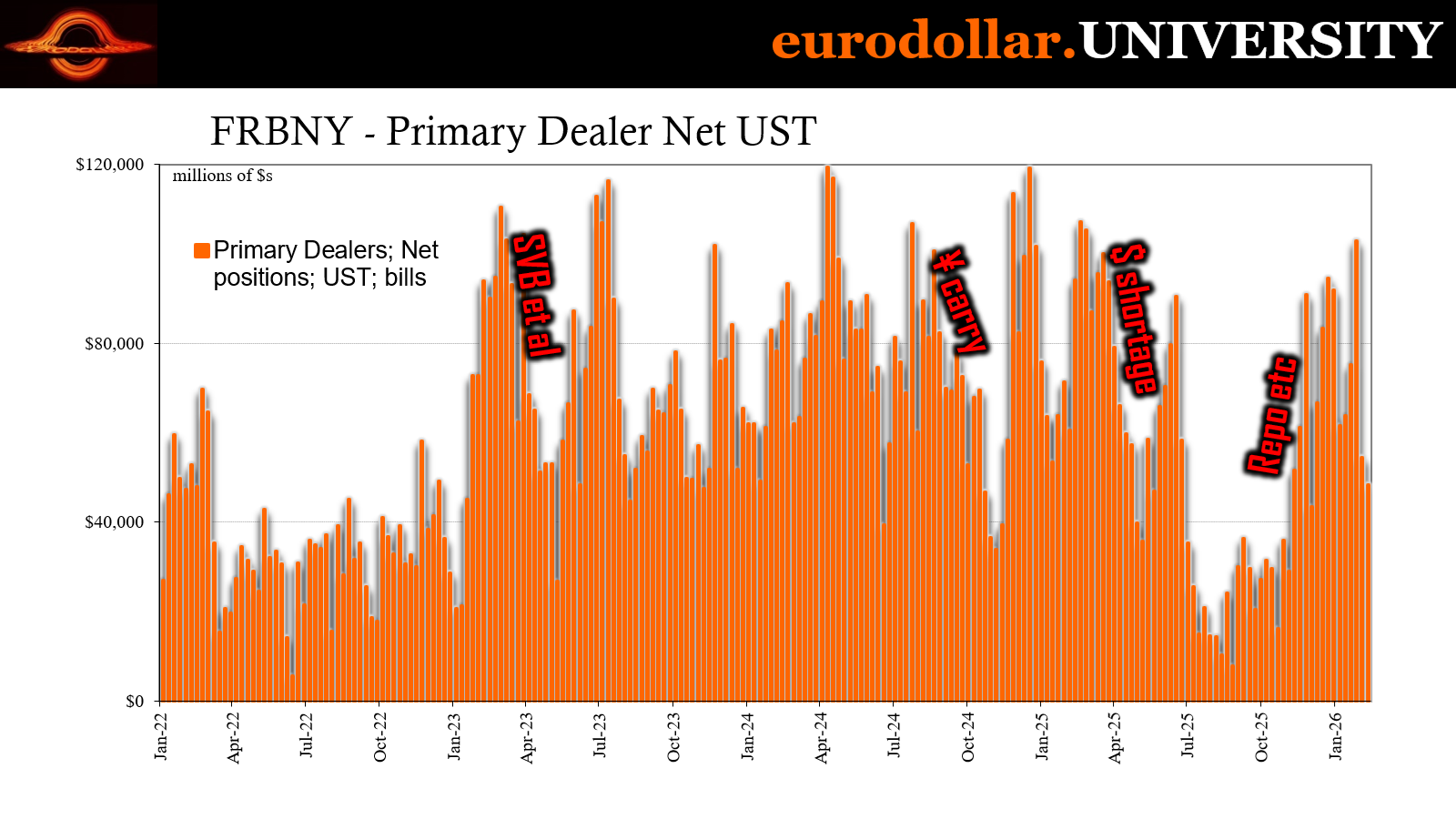

Primary dealer positions in bills add another layer to collateral considerations and more. It’s less about their baseline holdings and more about when those in bills jump to around $90 or even $100 billion. When that happens, quite often (not always) difficult monetary conditions follow and for mostly the same reasons as with coupon inventories. It was that way just before the bank crisis in 2023 or the carry trade blowup in 2024.

Cumulative bill holdings jumped to $94 billion the week of last Christmas, seemingly consistent with everything else at the time, having previously reached $90 billion the final week in November ahead of the outbreak. But like a lot of those other indications, repo rates, fails, etc., dealers let some bills out starting early January.

With the Treasury department flooding the system again with 4w and 8w instruments, no need to hold as many bills to take advantage of scarcity that Uncle Sam and Secretary Scott were taking care of. However, despite steady weekly issuance back above $100 billion moving onward, dealers began to pile on bills all over again in the back half of January leading up to the volatility at the start of February (the private credit problems and the initial selloff up to February 5).

In other words, even in the bill section of Treasury inventories there was reason to suspect January’s calm wasn’t widely shared or that it would prove temporary.

Taking those positions into account, it wasn’t so much out of the blue (pun intended) when on Tuesday more than $30 billion in activity visited the Fed’s repo window. We’ll never know if or how much that might have been related to worries about private credit. In some ways we’re talking about two separate matters, the micro focus on private credit liquidity surrounding certain funds and fund companies versus the systemic condition of money circulation in repo and beyond.

Yet, we also know these are connected, even if tangentially; connected by dealers. It isn’t implausible to think dealers knew what was going on at the owl and started to connect their own dots about where that could lead to already being on high alert for it.

With that degree of illiquidity, SOFR of course jumped, reaching 3.73% as of Wednesday, only two bps below the fed funds upper bound. Again, it’s not the rate itself, the volatility and the seeming unpredictability of it. You think you can easily, cheaply, dependably get repo funding only to see, seemingly out of nowhere, the marketplace goes awry.

Knowing that Stage 2 was about to be unleashed this week, perhaps that is what led to the $30.5 billion at the New York Fed. I highly doubt it was pure coincidence.

Mr. Powell at least had January. For a few weeks, he looked like a competent central banker as it looked like not-QE and its bank reserves had provided the answer. Just a little technical fine-tuning of the Fed’s balance sheet that got everything in money markets back to normal.

If only that was true.

If it was anywhere close to the case, primary dealers wouldn’t be sitting on that massive $413 billion Treasury pile. Yes, there are those even today who will say dealers are getting stuck holding the bag as the government gets broke-r by the day selling more bonds no one wants. We, however, know that’s demonstrably false.

The yield curve is bull steepening. Yields are tilting lower again while it does. If dealers didn’t really want all those bonds and notes, they’d have little problem selling them to a secondary market which clearly does. They’re choosing to hang on to what just so happens to be the best collateral.

No, dealer holdings proved nothing much had changed from December. If anything did, it was the monetary system looking forward to not just more of the same, but escalation in both main areas: money and macro.

Blue Owl’s very bad week is just the latest reminder on the one side about how especially Stage 2 is a very real threat; because it’s no longer a threat, it happened. Then the macro data, including GDP, further proves the same from the macroeconomy.

The FOMC’s mention of private credit, like Walmart’s hiring recession reference, those were not nothing. That $413 billion pile, though, it is definitely something.