THE PARADE OF TRICHET WAS ON FULL DISPLAY TODAY

EDU DDA Mar. 19, 2026

Summary: So much for being reasonable. The parade of Trichet was on full display today. Meanwhile, while central bankers fret fantasy inflation we got another real example of deflation. Oil soared and spreads widened, leading to liquidations across metals. Rates round-tripped. Nothing seems to be what it is supposed to be. That includes the private credit bubble and how much rate HIKES contributed to it. Therefore, low rates and deflation are to be expected during the bust. The oil shock just adds more deflation on top.

IF YOU DON’T LOOK CLOSELY, YOU END UP MISSING IT

If central bankers in North America were (relatively) reasonable in their views about the oil shock yesterday, their counterparts in much of Europe today went full-blown unreasonable. Policymakers in London were practically in a panic, suggesting there could be a rate hike from the Bank of England possibly next month.

They’re all in a rush to become the next Jean-Claude Trichet, the clueless ECB leader who hiked rates in the middle of 2008 - and then did it again (twice) in 2011. Both of those examples came just prior to Europe and the rest of the world falling into re-recession and more deflation, not inflation no matter how high oil had gone beforehand.

If anything, higher energy costs only contributed more to the downside. At least that correlation holds throughout history.

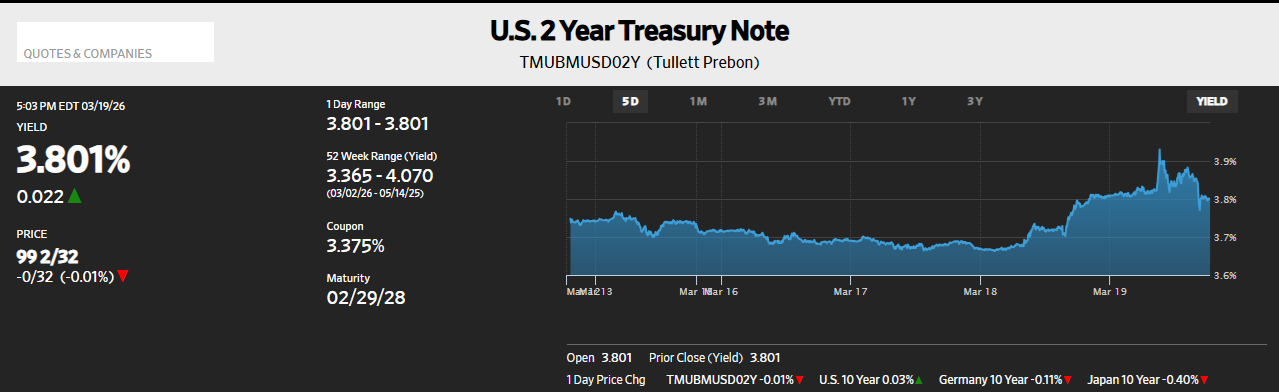

Despite the outburst of hawkishness and the global implications for the near-term path of ST interest rates, by the end of the day there was little left of them at least in the Treasury market. The 2-year UST rate soared as high as 3.92% in the English aftermath. By the end of the day, however, it was right back down to almost where it had started.

The Treasury Department calculates a closing value of 3.79% vs. 3.76% yesterday. Trichet’s ghost is modestly but noticeably lifting the front end.

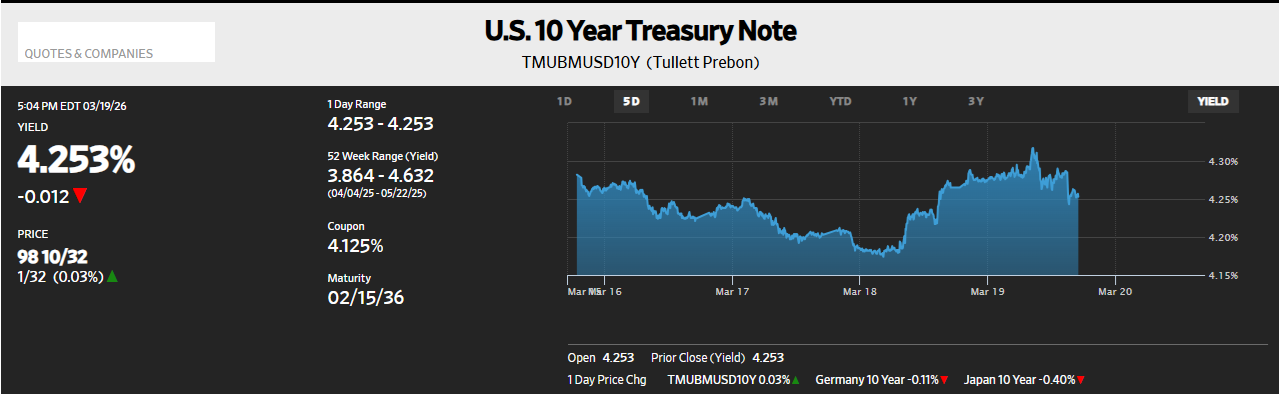

It’s not more because of the back end. While yields on that part of the curve initially moved higher, the 10s reaching 4.32% at one point, that benchmark maturity ended the day lower compared to the previous close. There’s hawkishness and then there’s crazytown in the face of what an oil shock would legitimately do.

The BoE just may raise rates soon, and a few others could join the Old Lady, the only outcome is Trichet.

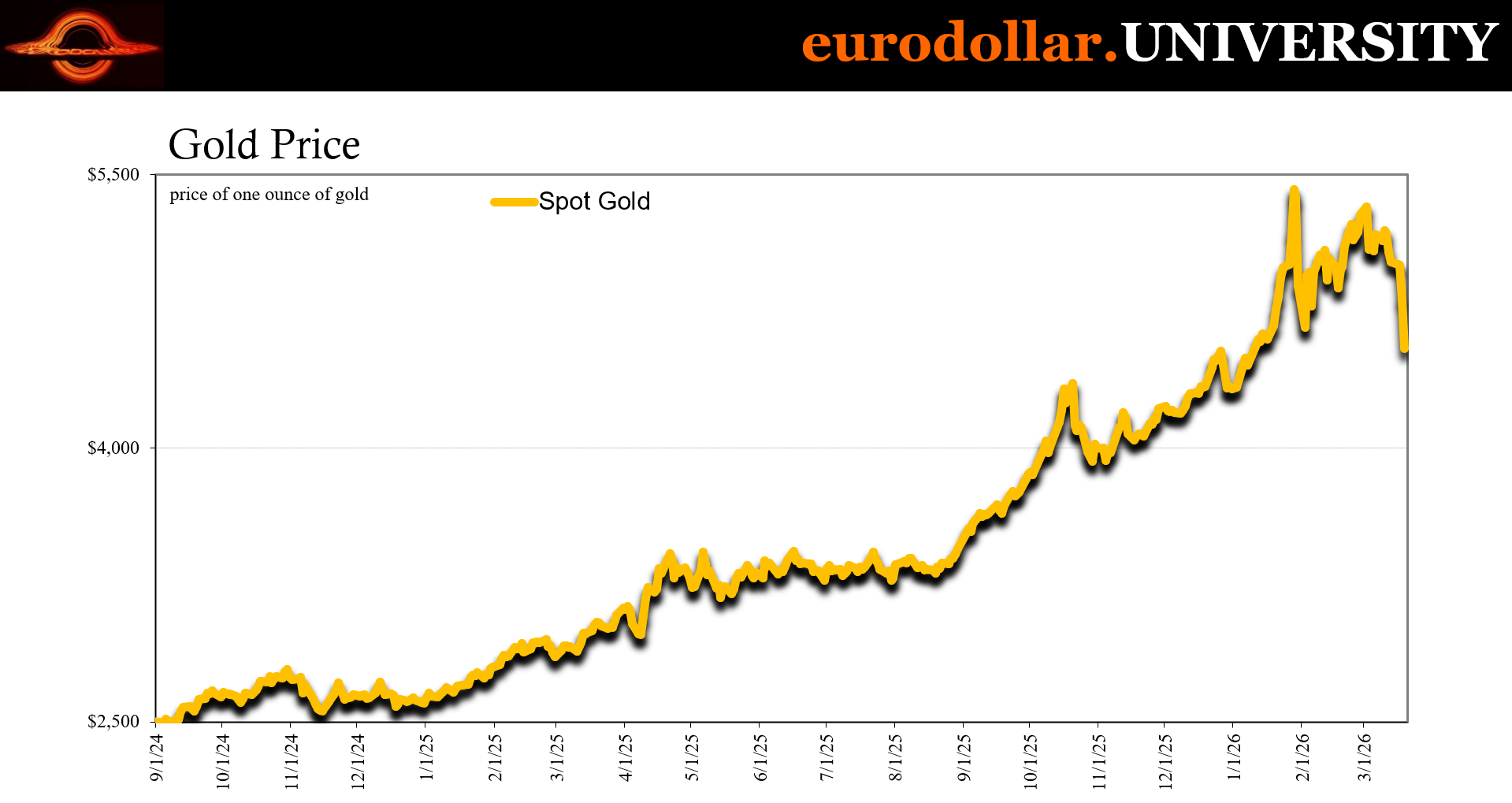

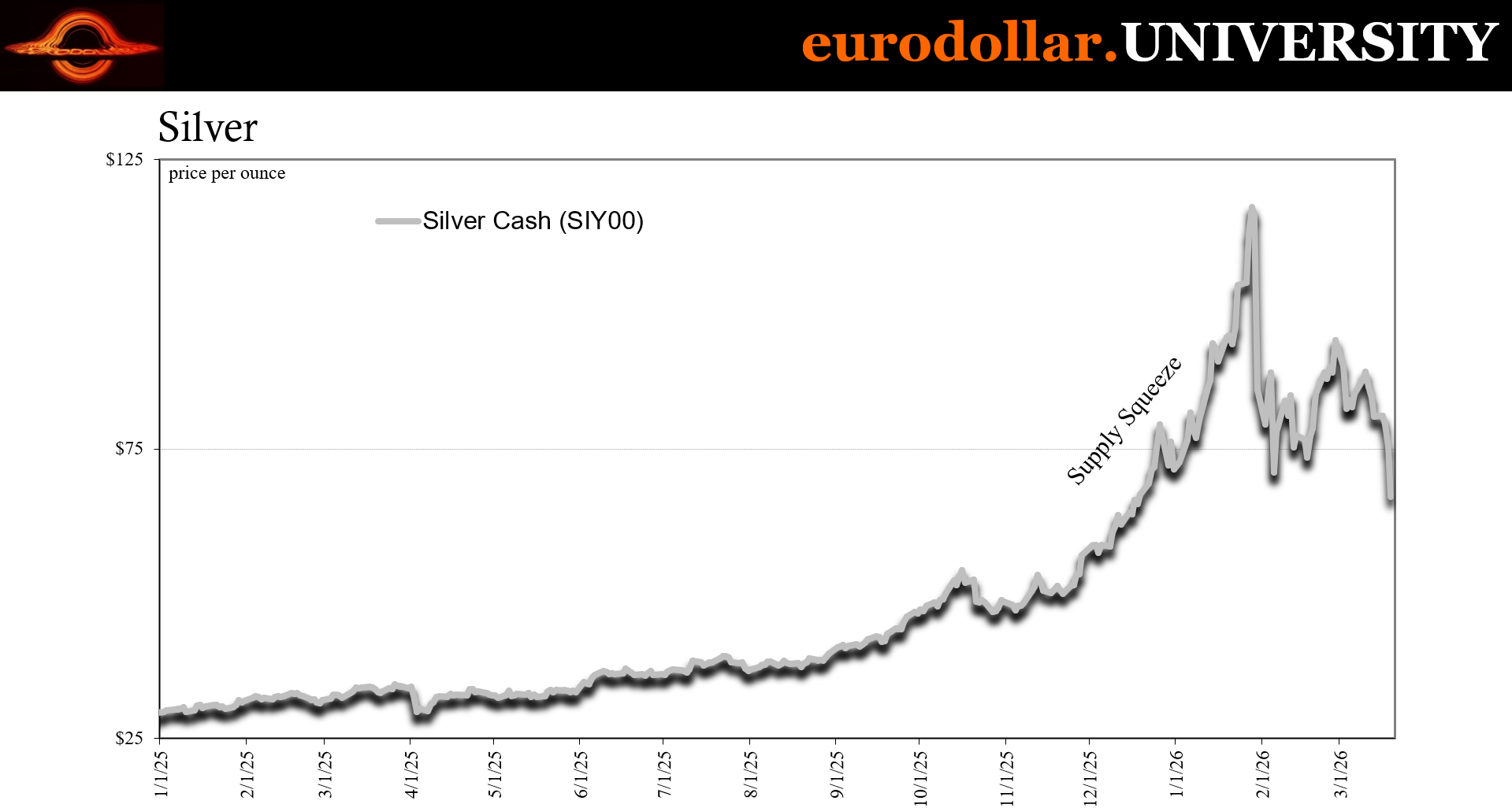

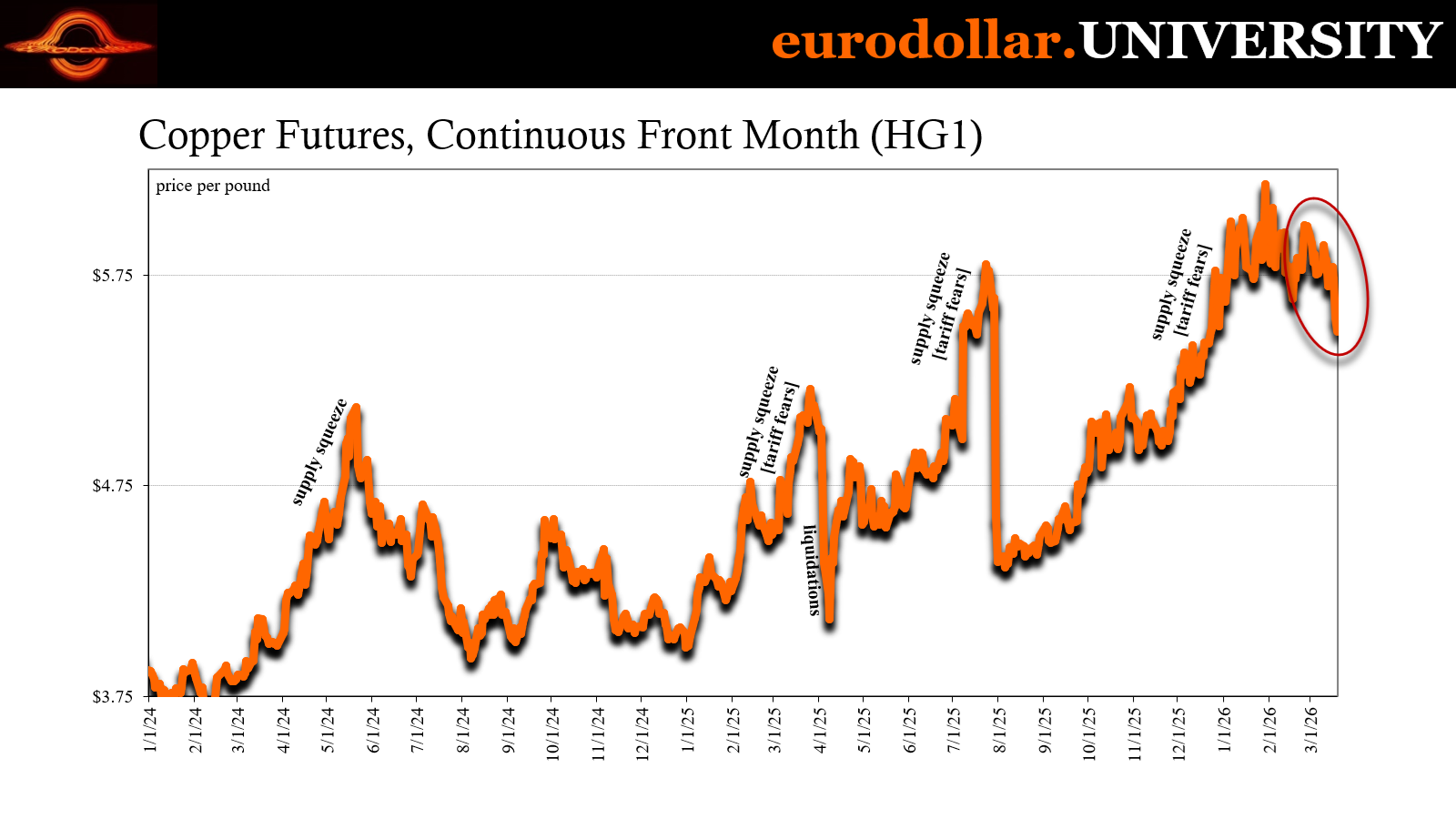

We were definitely reminded of that point in what turned out to have been a massive liquidation across metals. Not just gold and silver, copper and even aluminum were dumped right alongside. Each of them recovered, but the correlation with oil and oil spreads across the global market left the telltale signs for the other part of the oil shock.

There is a dollar liquidity problem which comes along with it, one that was on full display throughout the early morning and not for the first time.

It’s this constant tension between officials who get interest rates entirely backward and the increasingly negative consequences from the real economy they don’t understand. The same is true of private credit, the still-simmering background underlying any liquidity difficulties generated by the oil shock.

The Fed’s rate hikes contributed much to blowing that bubble in the same way further rate cuts will be in reaction to its bust. Yes, you read that right, as I’ll explain.

Now we have the possible collision of all these factors at the same time as central bankers predictably perform to their inner type. They’re all Jean-Claudes.

Oil spreads into heavy metal

WTI burst back above the century mark early today after another wave of panic petroleum buying registered across the system, originating as usual in Asia. The region is heavily reliant on Middle Eastern product currently stuck in and near the Persian Gulf. London insurers keep saying they aren’t denying policies in the same way home insurance firms in Florida say they’re active in the state after a hurricane.

Technically true, functionally irrelevant.

Coverage is available, true, but only at such exorbitant premiums it becomes so uneconomical to even think about taking out a policy. Right now, there are reports shipowners who are thinking of having their vessels transit Hormuz being quoted at around 5% of the boat’s value. For a single sailing. No one is going to do it even if when it might not also risk the life and limb of the crew.

In short, there is no effective coverage today which is why, among other dangers, there is no traffic flow. Without it, there are going to be physical shortages. There have already been reports in places like India, where small businesses and individuals have had to resort to burning wood in lieu of the usual petroleum-based supply.

The panic-buying of crude is understandable. Only, more recently, the intense bidding has become more localized. During the initial wave, oil spreads among the various global benchmarks started to diverge, though they remained relatively close enough. These days, differentials are becoming enormous.

Brent got as high as $115 today whereas WTI maxed out around $100. Both backed down after the panic had subsided yet remain far apart. Murban soared to very nearly $130. Abu Dabhi’s chief benchmark is currently about $30 higher than the spot price being charged in America.

From the North American perspective, it may seem as though the energy shock has settled down. Oil pricing around $95 isn’t good, obviously, but it’s also nowhere near $130. The widening of global spreads leaves the wrong impression. The panic hasn’t subsided at all and that is a very bad sign. For one, it means there is a very high chance the shortage lingers even if the Hormuz bottleneck does get resolved fairly quickly.

The longer it remains bottled up, the more time it will take to normalize afterward therefore the greater the chance more economic damage gets done in the meantime.

Not just macro, there will be more financial problems to go along with it. We’ve already seen several instances of liquidations and today we got another one. Commodities, particularly the metals, were utterly slammed straight away from Asia. The connection to oil is via dollars.

Dollar shortage

Indonesia had already announced greater capital controls which hinted the dollar pressure was already building there. Southeast Asia’s largest economy is also its biggest oil importer. The oil price shock, even before getting to the physical shortage, is a margin call.

Importers were only expecting to pay the previous market price for crude. Even if deliveries are under contract, many of those will have to be replaced in the very short term given how any which were supposed to have originated within the Gulf region just aren’t going to happen. Not soon, anyway.

To replace those cargoes, it is going to require a boat load (pun intended) of capital, meaning dollar funding. Global traders are already getting pinched for the same reasons, having to go hat in hand to global banks arranging for billions in credit they didn’t plan for (or, if they did, they didn’t expect to draw on it right now).

Import firms across Asia are facing the same crunch. Where are they going to go to get funds? The eurodollar system, already on edge and risk averse, it’s not going to be an easy sell therefore local sources are the most likely alternative (thus, Indonesia). Even going to the government or some central authority, whomever has the ability to raise dollars quickly that can then be made available quickly to buy whatever oil or LNG might become available in a pinch.

Thus, when oil prices skyrocket as they did earlier today, the panic buying behind it would also create a short run spike in dollar demand. And so metals had to be sold down.

Gold, for example, started getting liquidated at around 12:10am ET, meaning morning in Asia. The dumping continued throughout the remainder of the regional session, not subsiding until 8:05am ET, lasting right through the European morning. It wasn’t central bank hawkishness, as some have said, rather, again, understandable demand for the kind of money you can buy oil with.

There were surely other factors which piled on the selling, too, including margin calls as prices smashed through certain levels on the way down, skittish lenders who didn’t want to extend more credit into what appears to be a deteriorating situation in every respect. Not just in the microscale of metal and commodity trading, but also in the bigger picture sense of how the expanding oil shock will lead to increasingly negative and more likely consequences.

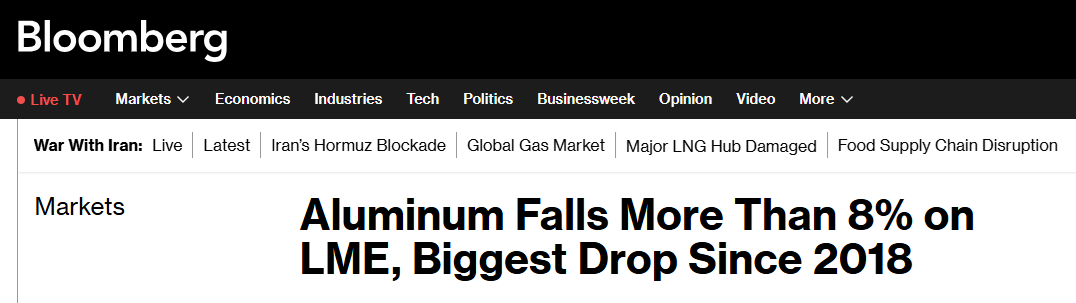

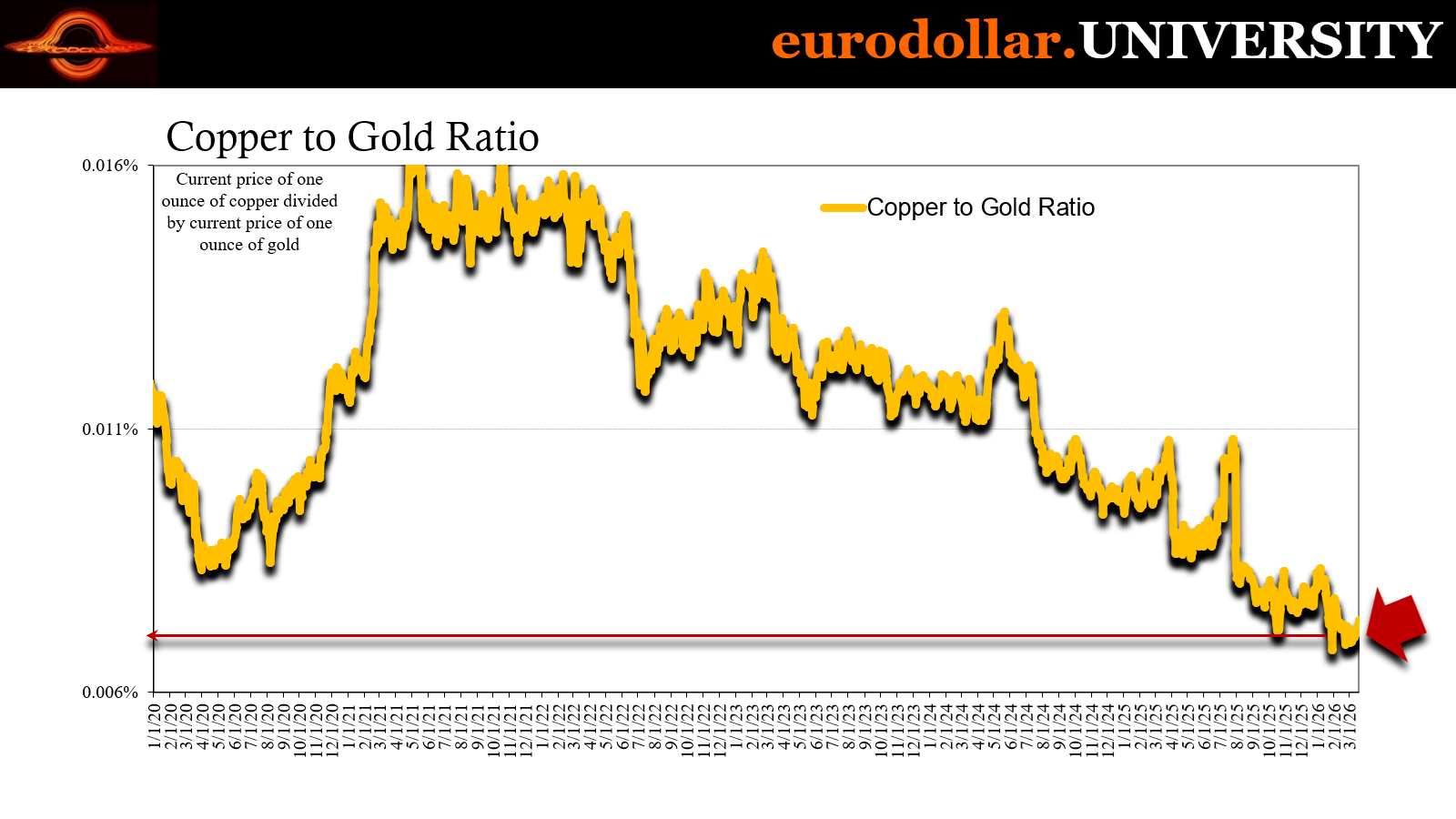

The casualty list was impressive. Gold was slammed to a low of $4500 from yesterday’s $4800 close which was already down from the prior $5000 intraday high. Silver fared much worse, nosediving under $66 before rebounding to make it back to $72.80. Copper dropped into the $5.30s. Even aluminum got caught up in the vortex, with the largest daily drop since 2018.

Oil shocks become deflation in money as if the system needed one more way to refute the idea it will lead to inflation.

INFLATION, WHAT INFLATION? IT WAS NEVER GOING TO BE INFLATION

What good were the hikes?

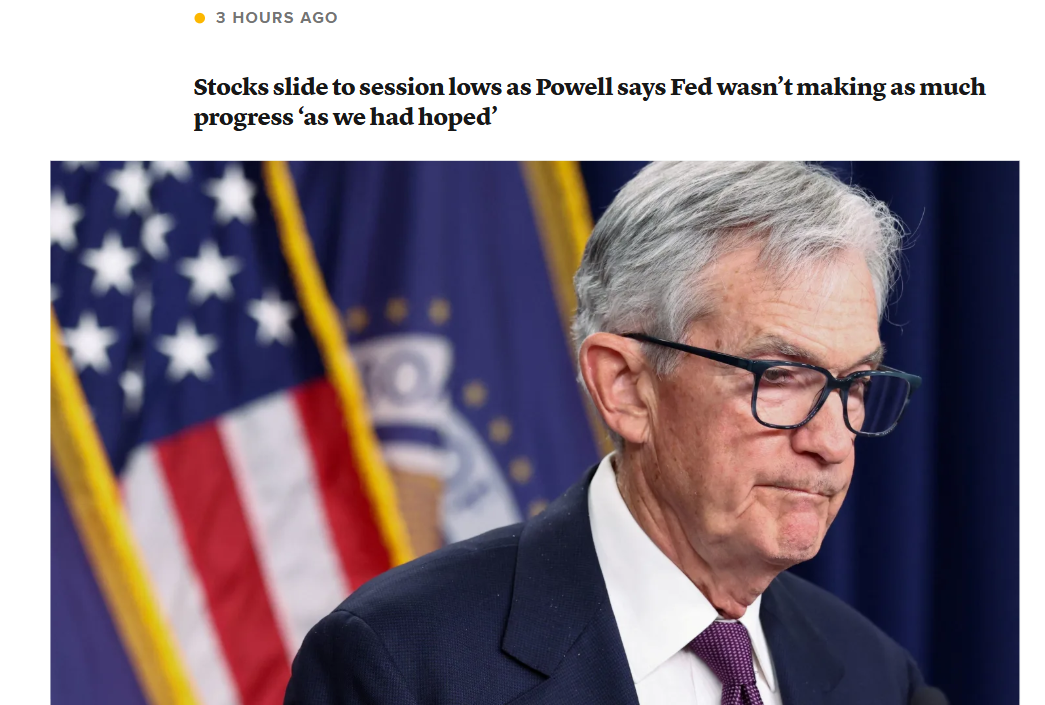

Government officials are among the least self-aware individuals to begin with, yet you have to wonder if ever Jay Powell gets that uneasy feeling every time he complains about inflation being “sticky” he does realize what that has to mean about the Fed and everything it stands for. As I covered yesterday, the FOMC was - overall - reasonable in its reaction to the current energy circumstances. The Chair, not so much.

He complained policymakers don’t believe they’re seeing as much progress on inflation as they had been hoping. Of course, they are going to throw up a litany of excuses for this. Prior oil spikes. Trump’s tariffs. There are a million separate reasons to blame this and that.

Even so, Jay Powell in 2022 presided over what the Fed constantly characterized as the most aggressive (read: powerful) monetary (not money) response to inflation (supply shock) ever conceived in the Eccles Building (the very facility that has Powell under DoJ investigation). It was or was supposed to be this awe-inspiring display of central bank might.

The Fed’s finest hour, as Powell himself implied.

So, how in the world can he sit here four years later and complain the biggest rate hikes in history didn’t make as much progress on inflation as they said it would?

FOUR YEARS.

The rate hikes began with an FOMC vote on March 16, 2022, a 25-bps start and the first rise to policy rates since the embarrassing finish to the prior cycle at the end of 2018. If you are being honest, you’re left with the impression interest rate (not monetary) policies don’t seem to do what they’re supposed to.

We know all about “stimulus” which never stimulates; we got another reminder of it today when new home sales crashed by the most since 2013, falling to the fewest sold since 2022 even though mortgage rates during the month in question were the lowest in years.

Not only do rate cuts reflect weakness instead of curing it, rate hikes are very much to blame for the private credit bubble. Sure, bubble behavior stupidity and greed are there, too, but rate hiking is a key ingredient. In fact, that’s exactly what Japanese carry traders admitted in the summer of 2024 when it blew up.

Most people have the impression low interest rates create bubbles. After all, anything which artificially cheapens the cost of borrowing must lead to the worst cases. But that’s just wrong. The far more relevant factors are all on the supply side, how lenders respond rather than what borrowers might consider.

They call it “reach for yield” and we can pick from a number of examples, not just private credit in the twenties. Mortgages in the middle 2000s are good place to start. To this day, people associate the housing bubble with Alan Greenspan’s rate cuts after the dot-com bust and recession. Worse, they think it was the rate hikes which popped the thing!

No. Credit growth was intense long before the Fed once again failed to stimulate 2001-04 with lower policy rates. After all, two years of jobless recovery were the reasons why the Fed went to 1% in the first place.

Moreover, mortgage rates follow the Treasury market, not the misguided policies of clueless, backwards bureaucrats. Greenspan may have pushed ST rates down to their lowest levels since the thirties (before ZIRP), but mortgage rates didn’t come anywhere close to that after moving in tandem with bond yields.

By the time the “maestro” began raising rates, money and debt growth was out of control. Rather than putting the brakes on it, increasing ST interest had the opposite effect, turbocharging all the worst behaviors. The worst “vintages” of mortgages were those issued in 2005 and 2006, during and after the rate hikes (which began in June 2004).

How is that possible? We’re taught that higher rates mean it’s more expensive to borrow which then chokes off borrowers. But you have to consider what that did to lenders.

They have to “reach for yield.” As ST borrowing gets more expensive, they don’t do less of it, they find other ways to maintain positive, profitable spreads. Lenders get even more creative. When were NINJAs and no-down payment loans at their worst? When ST rates were going up.

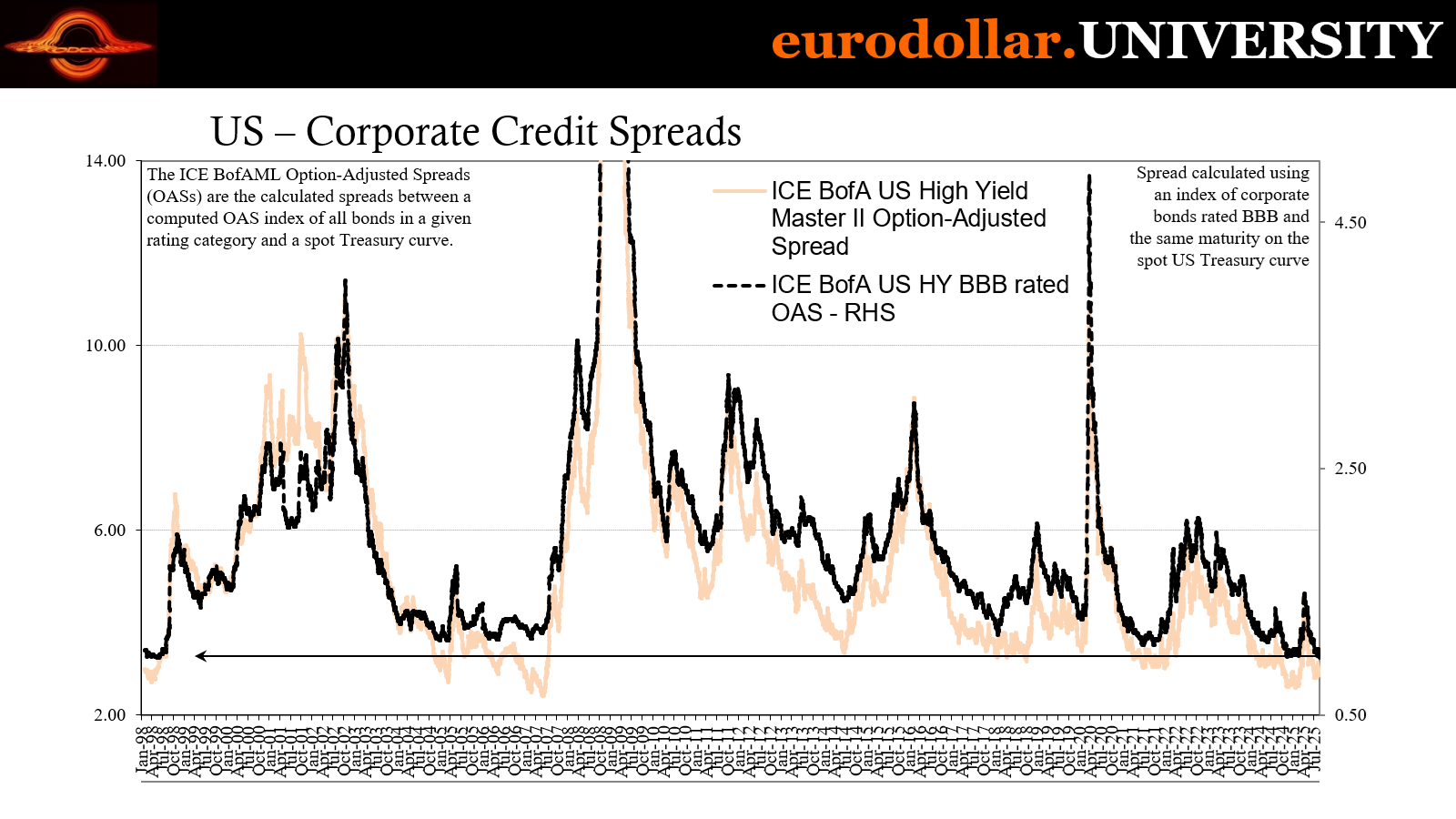

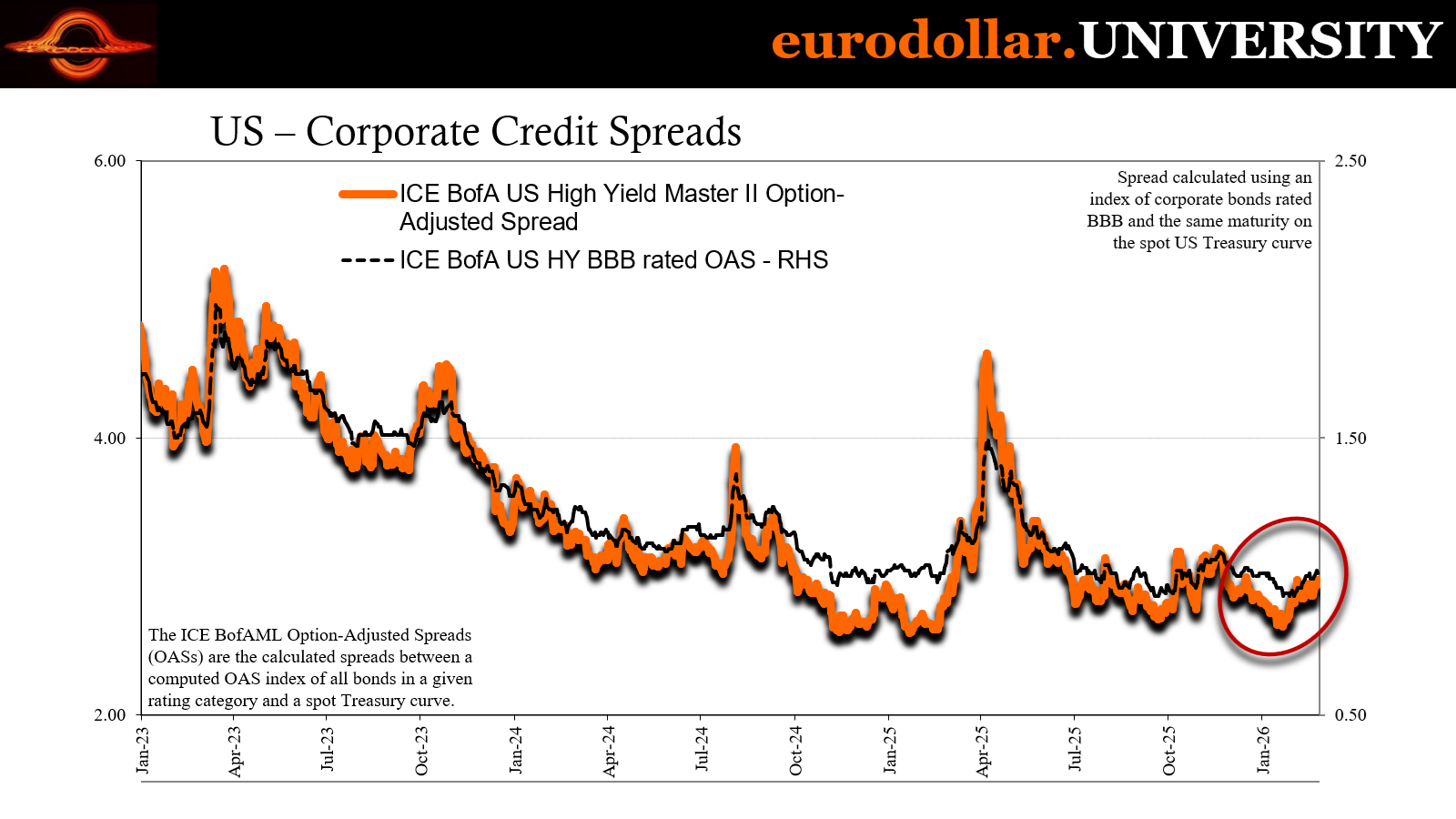

Risky spreads collapsed between 2005 and 2007 as demand for risk soared (below).

The key to it all, aside from the hubris behind financial engineering, it’s the positivity provided by the Fed or whatever other central bank. They hike rates but also claim the economy is boomingly fine. In fact, oftentimes the two are put together; officials say they have to restrain the economy because it’s so good. Higher borrowing costs but then no economic risk.

Reach for all the additional (risky) yield you can possibly conjure from the dumbest ideas.

Alan Greenspan was trying to pull back on the bubble (he didn’t see that way) but instead blew even more air into the damn thing and had no clue while it was happening. Instead of monitoring reality, officials stuck to simplistic, stupid econometric models which didn’t even incorporate financial inputs. This goes beyond flying blind; they don’t even know what it is that’s supposed to happen.

They say rates become restrictive. And there is still no proof that’s the case. The only evidence they have is their regressions. It’s the same circular reasoning behind expectations theory; Economists put it in their models because they needed to in order to make the math work, and because they did everyone now thinks that’s how inflation works.

Same goes for rate hikes which in the real economy don’t work that way.

Private credit

What did the Japanese say back in that critical summer in 2024? They said the rate hikes from 2022 raised their borrowing costs which propelled the buying of less-than-AAA CLOs and a whole bunch more, so already this should sound familiar. Just like the mid-2000s, the Fed tried to restrain them with higher financing rates but then also gave the Japanese along with the bluest of owls the go ahead to reach for yield by simultaneously declaring the economy strong and resilient.

Seriously, the more likely outcome would be worsening bubble behavior not putting a stop to it. The rate policy story is children’s fiction.

If there is “no additional risk” to seek out riskier and riskier borrowers, of course lenders are not just going to go looking for them, they’re going to get creative once more in what they do once they find subprimes. This is just what happened in private credit and shadow banking during the 2020s, propelled in large part by the rate hikes.

Yes, greed. Stupidity. People doing dumb things. But they started to because the rate hikes created the need for more return while the ever-optimistic forecasts provided the cover and the justification for going all the way on it. The more higher-for-longer got to be the accepted view, along with the strong economy, the bigger the bubble got.

Rate hikes didn’t constrain credit; they helped expand the worst of it.

Should it be surprising everything begins to unwind when going in reverse? Only, in the opposite case, the rate cutting does not pop the bubble, merely becomes the predictable response to its downside. Where money only flowed in while reaching for yield, money will have to flow out and rates get to reflect the reversal whether policymakers realize it or not.

It certainly doesn’t matter – either way – what the policies are intended to accomplish.

And that is how Jean-Claude Trichet hikes policy rates in July 2008. It’s the same reason why Jay Powell complains there isn’t enough progress on inflation a full four years after having started the most aggressive “tightening” the Fed has ever engaged in.

I used to write all the time they really have no idea what they are doing. I even created a macro once-upon-a-time so that I could just type the shortcut TRHNIWTAD and have it appear in full text. But this is difficult for most people to accept.

How could it possibly be that way? After all, everyone says the Fed prints money and higher rates restrict the economy and bring inflation down.

Well, not even Jay Powell can say that today, can he? The guy is either so

The truth is it has always been like this. Read the quotes below from Friedman in 1963 talking about the Fed in the 1920s. This is just what central banks do. Officials create policies from whacky ideas, have no clue how or why they should work, and if things do somehow go well they can say they did because of the policies. The only real policy is to turn correlation into causation, the true skill of Mr. Ben Bernanke.

This is precisely what superstition is.

During periods of turmoil, central bankers appear lost, helpless, prone to fits of what in hindsight is shown to have been very obvious stupidity. They end up

Meanwhile, oil shock and liquidity go unappreciated everywhere else but where it matters most. Yet, all the media can talk about is the line out the door to become the next Jean-Claude Trichet. And won’t they all be stunned when one or more of them do.