Daily Briefing 6/16/25

Big Three/Unemployment Rate (NBS)

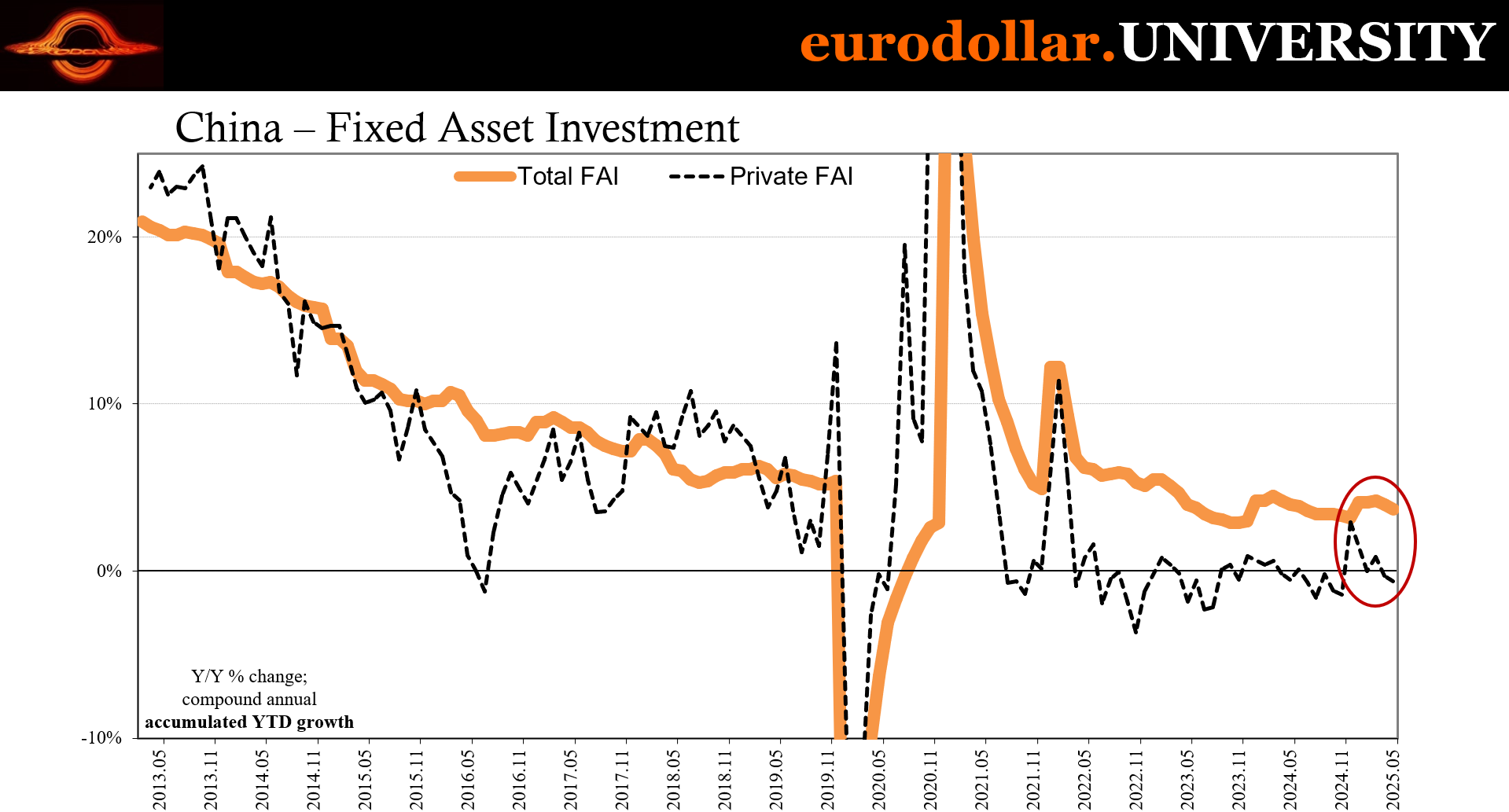

China’s economic data for May 2025 shows a mixed picture. Industrial production rose 5.8% year-over-year, slowing from April’s 6.1% and missing expectations, marking the weakest expansion since November 2024. Manufacturing lost momentum under the weight of US tariff pressures and tariff activity payback. Retail sales, however, surprised to the upside, accelerating to 6.4% due to holiday spending and especially government subsidies. Fixed-asset investment slowed to 3.7% year-to-date, dragged down by a deepening real estate slump, while private and foreign investment remained lackluster. Meanwhile, the surveyed unemployment rate edged down to 5% (zombies; see: DDA).

Interpretation

May’s macroeconomic releases from China reveal very little other than an economy struggling to gain momentum amid external headwinds and internal imbalances. The slowdown in industrial production growth to 5.8% - the weakest since November 2024 - reflects rising pressure on the country’s export-oriented manufacturing sector, as renewed US tariffs erode overseas demand on top of however much had already been pulled forward (payback is likely to remain ongoing ahead). While mining and utility sectors held steady, the backbone of China’s industrial economy - manufacturing - lost pace, growing at 6.2%, down from 6.6% in April.

In contrast, retail sales delivered a rare upside surprise, rising 6.4% year-over-year, the strongest clip since late 2023. Seasonal tailwinds from the Labor Day and Dragon Boat holidays, along with targeted subsidies for electronic goods, helped boost consumer spending across a range of categories. Household appliances, sports goods, and alcohol led the surge, pointing to resilient discretionary spending. For consumer electronics, thanks to subsidies the growth rate of 53% above last May was the most on record; smartphone and similar sales soared 33%.

Excluding Beijing-supported categories, the rest of retail sales would have seen zero growth.

Fixed-asset investment remains the economy’s soft underbelly. Growth of 3.7% missed expectations and remains heavily reliant on public infrastructure and selected high-tech manufacturing. The continued plunge in real estate investment (-10.7%) casts a long shadow, as the sector drags on related industries and undermines broader confidence regardless of any “stimulus” or targeted aid. Private sector investment was flat, and foreign investment fell by over 13%, highlighting persistent skepticism from both domestic and international firms. Month-over-month, fixed investment barely budged, up just 0.05%.

In short, China’s May data shows an economy increasingly held together by policy support and seasonal boosts, not by organic strength. The ongoing property bust, faltering industrial momentum, and fragile private investment suggest the recovery remains precariously balanced and with its dependable downside, slowing bias. If it hasn’t been completely proven by now, there is very little Beijing can offer which will reverse the tide – or even arrest the slide, however slow and incremental it might remain.