THE WRONG FOOT IN THE HOUSE

EDU DDA Jun. 30, 2026

Summary: JOLTS turnover came up short in May relative to payrolls. While we wait for the next set of pure guesses from the BLS, the same agency backtracks via turnover and once again discovers the same familiar shortcomings. These are very vivid in the housing market. According to the two big sources on home prices, those declined yet again back in April. Rates weren’t the reason nor was selling. It’s the same reason why Economists is Europe were stunned by today’s big CPI numbers.

WE’RE TAUGHT RATES ARE THE KEY TO REAL ESTATE WHEN WE SEE YET AGAIN ‘SOMETHING’ ELSE IS

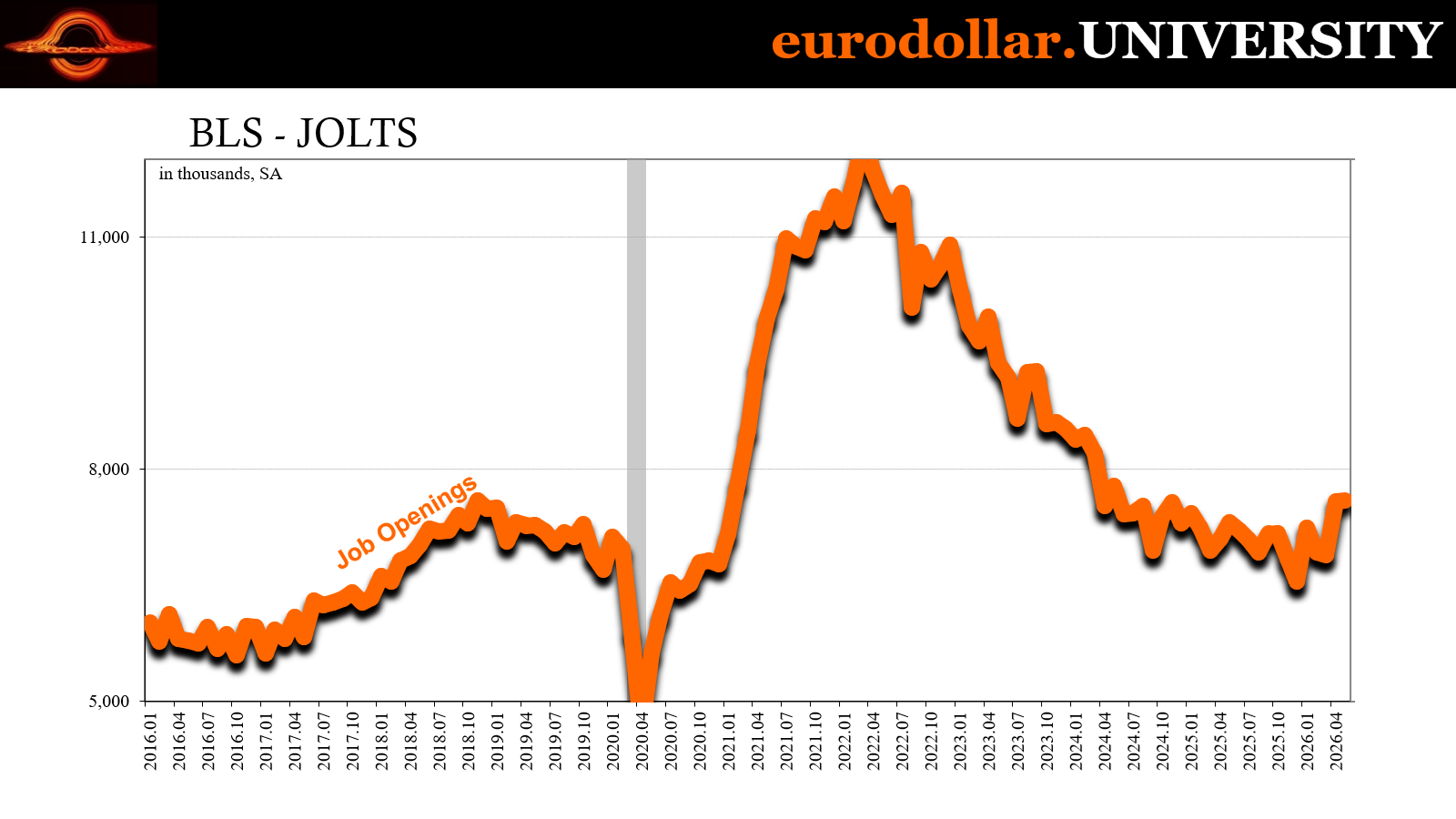

Three days from now, the BLS will deliver another headline to the media and public which won’t amount to much beyond the computer digits it takes to create all that noise out of so much nothing. Today, the same BLS reported on labor turnover, the real focus of its JOLTS data. Unfortunately, the same mainstream spotlights the wrong part of this one, too.

They go for the “JO.”

Looking through it to the important figures, hiring was dismal, quits were minimal and net turnover says payrolls were probably close to zero in May, not robustly confirming the benign view from Wall Street. Main Street continues to have few options, fearing those are becoming fewer all the time.

They said so, again, in another confidence survey. For the Conference Board, the percentage of respondents reporting jobs were hard to get in June jumped to the highest since early 2021. Everyone is alert to layoffs looking for mass doses of them when they keep coming in dribs and drabs. Thus, we’re purposefully left with a false binary choice: either jobs are disappearing by the millions or everything must be just fine.

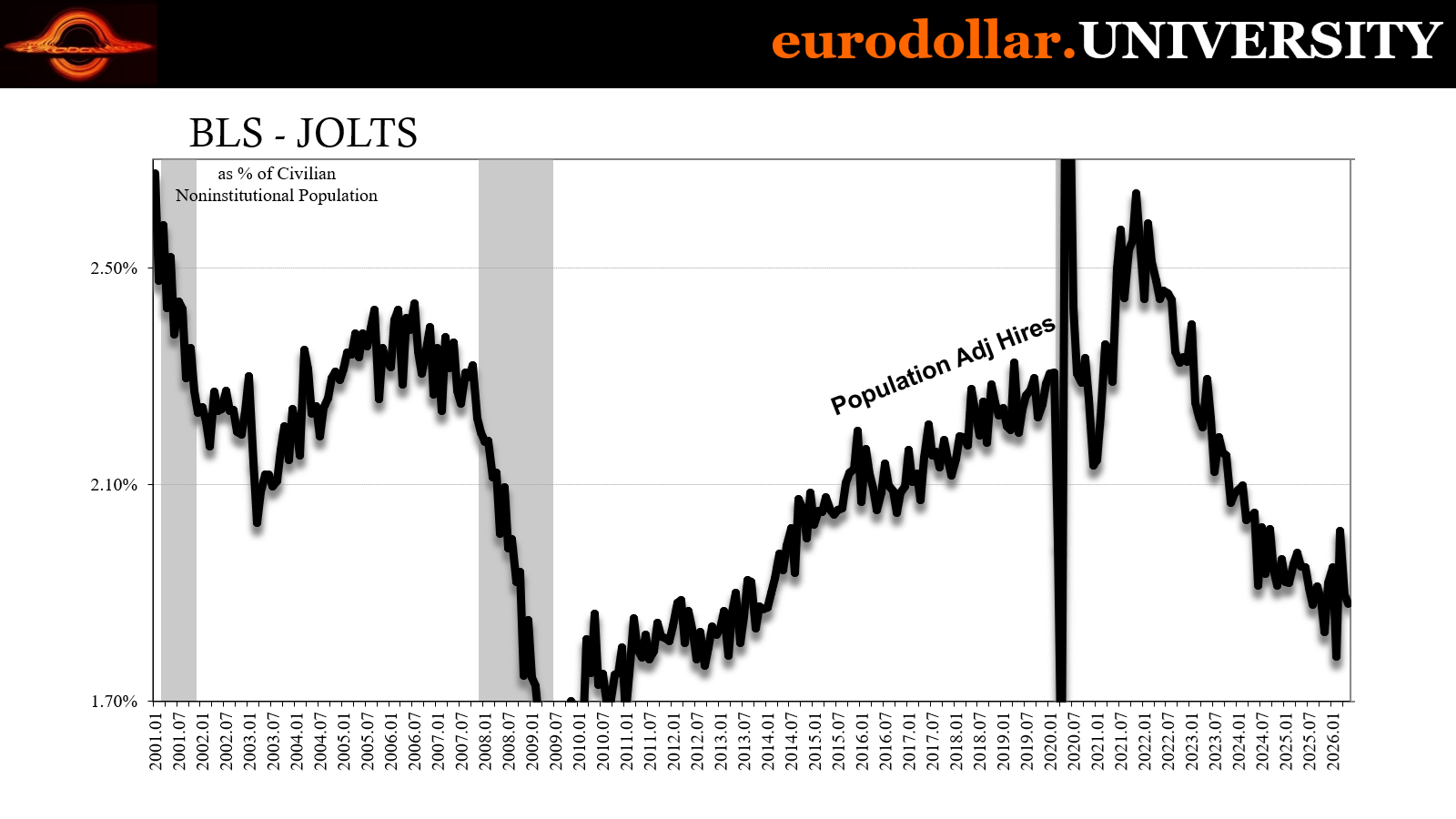

In reality, flat Beveridge is the ongoing hiring freeze.

One that at least will chill “inflation.” Picking up on yesterday’s theme scouring Europe as a leading indicator, the European rate hawks were thoroughly flustered by a cluster of inflation numbers coming from the biggest economies on the continent. Germany, France, Italy, all “unexpected” dips in CPI rates.

While oil is responsible, what’s missing is what those hawks thought there’d be when, once again, we keep seeing more evidence inflation was never a risk. And why.

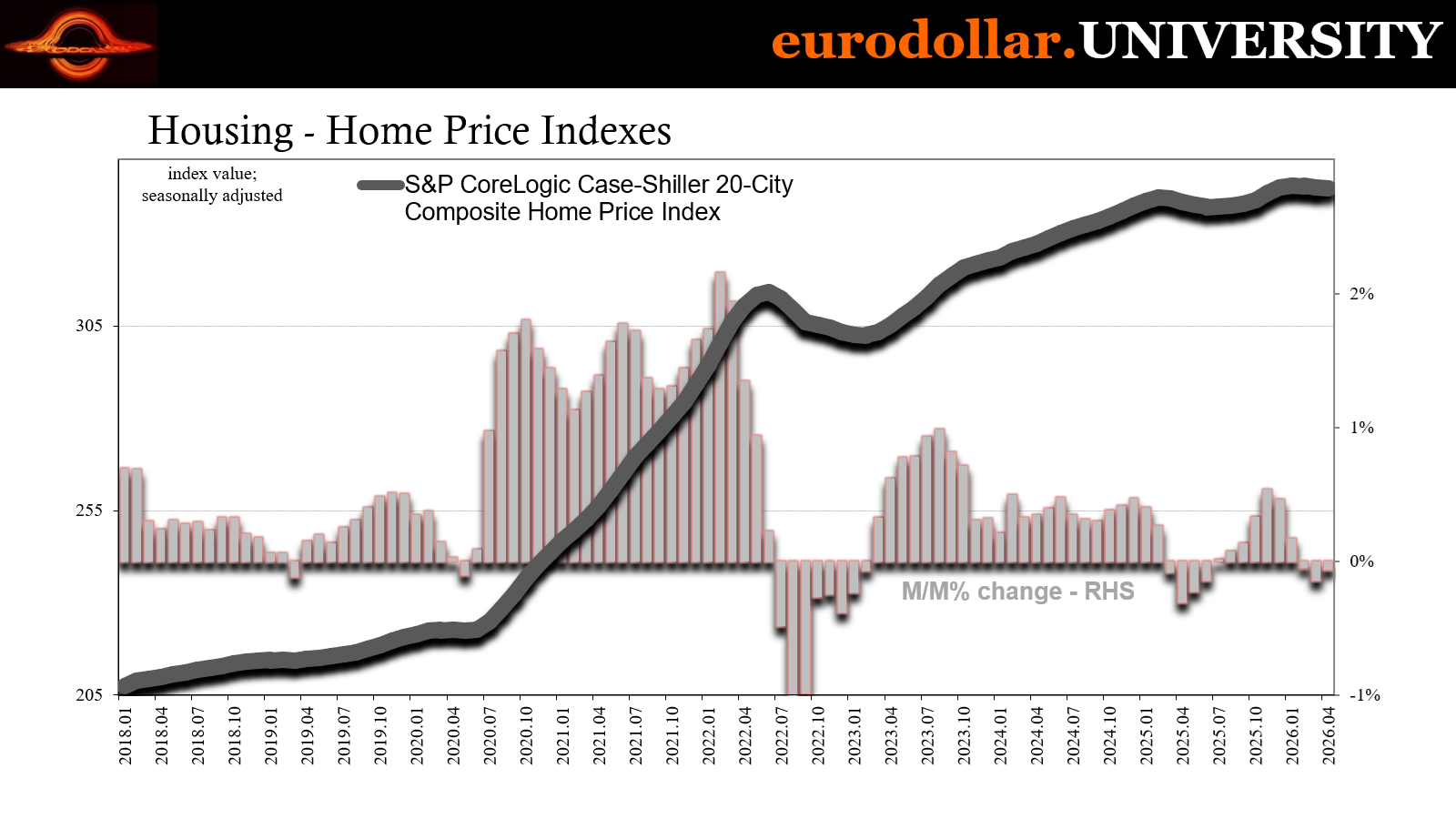

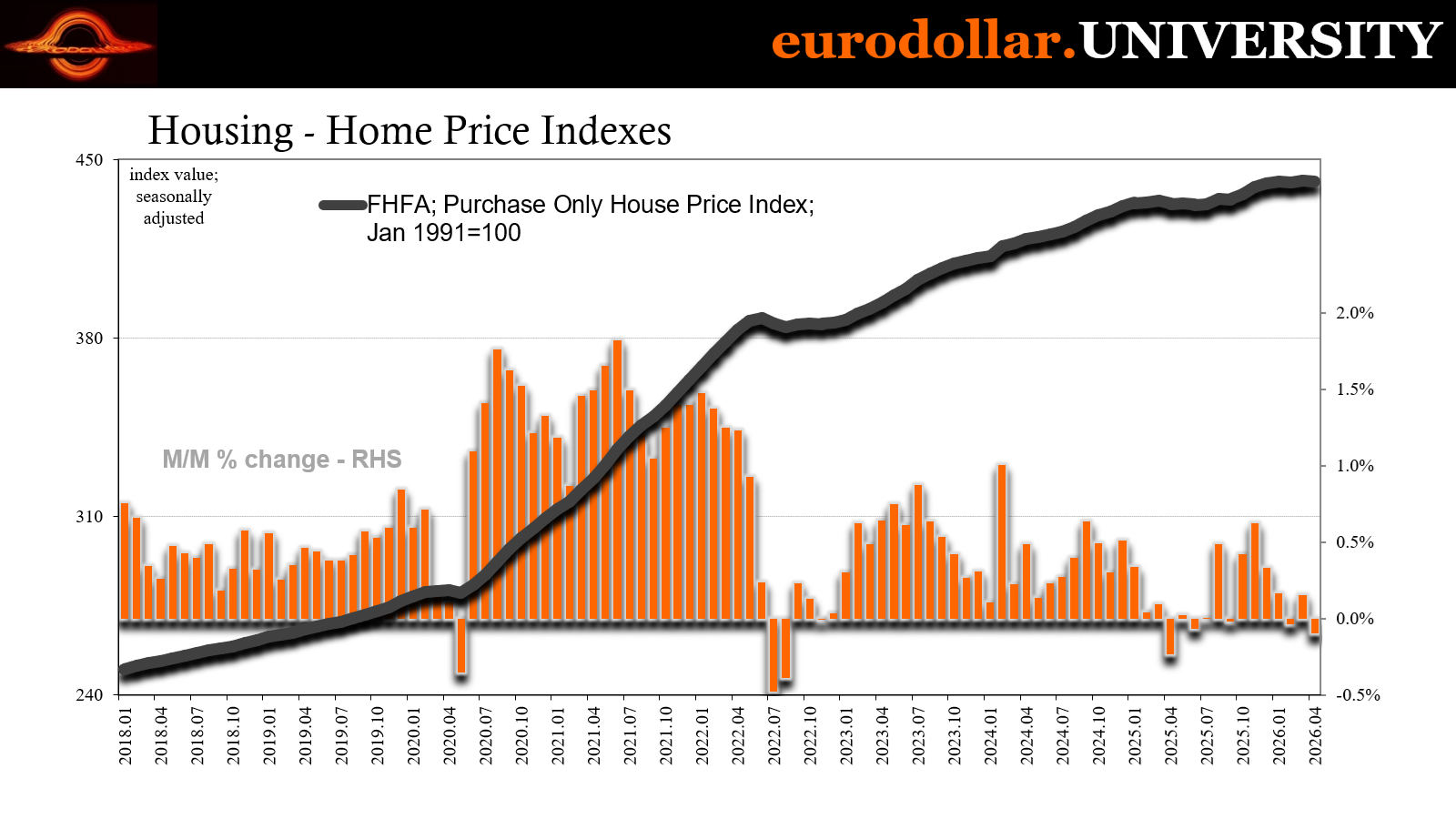

What continues to be a threat is that no-hire/some-fire dynamic. US home prices slid again in April and that was according to both major home price averages, S&P’s (Case-Shiller) and FHFA’s. Lower mortgage rates have done little to nothing because rates aren’t a primary factor these days. The LTS from the BLS is and falling home prices are more proof to that effect.

Wrongfooted

Oil prices are down, as everyone knows. Even Economists are vaguely aware. So, you’d think those statisticians would have been more optimistic about June CPIs and HICPs. Without crude, rates of price increases would have to come down.

But this is where practical experience messes up the theory. As discussed, European Economists more than most believe oil is no longer the full story. Yes, petroleum is dropping but according to their models something else should already be pushing other prices up: those second round or second order effects they keep obsessing over.

So, despite softening in energy for June, the mainstream herd all figured other costs were going to make up some or all the difference. Surprising to no one at EDU, across Europe, in economy after economy, they didn’t. Take away the oil, consumer price rates already appear far less menacing.

Not that it will make any difference to the irredeemable hawks. Just like last year and the “tariff inflation” that never was, policymakers will be dedicated to keeping the story alive for years to come. I half joked that would be the case last spring, knowing full well those like KC Jeff over here at the Fed or Isabel Schnabel in Frankfurt don’t go on evidence. They were still screaming about tariffs right up until Iran even as there continued to be no reason to believe anything was changing.

Thus, while markets have discounted the chances for inflation this entire time, it will be some time yet before the Volcker impulse is diminished enough a sufficient number of central bankers fall back away from the hawk nonsense. Even as the reasons for doing so are clear as day:

German inflation cooled more than expected in June, part of a slowdown across most of the region brought on by the drop in global oil prices.

The reading for Europe’s biggest economy fell to 2.4% from 2.7% in May, the statistics office said Tuesday.

Data earlier in the day also showed a surprisingly sharp decline in France’s inflation rate, back to the 2% level targeted by the European Central Bank. Italy’s headline number moderated too, to 3.1%, wrong-footing economists who’d expected it to hold steady. [emphasis added]

Again, they believed German, French and Italian rates would hold steady or slightly accelerate because of second order effects, other parts of the consumer experience that would have been experiencing high enough prices to offset the sudden drag from the energy segment. They were wrong therefore wrongfooted because basic economics always escapes Economists.

Businesses know – as was pointed out yesterday – they cannot pass energy or any costs including tariffs to their customers, at least not without provoking a sizable backlash sacrificing volume. The only real pathway for either tariffs or energy shock prices is through the labor market.

Europe, as a leading indicator, is leading on where the next stage is heading – right where the curves have been pointing. Frown more, Euribor.

Sell this America

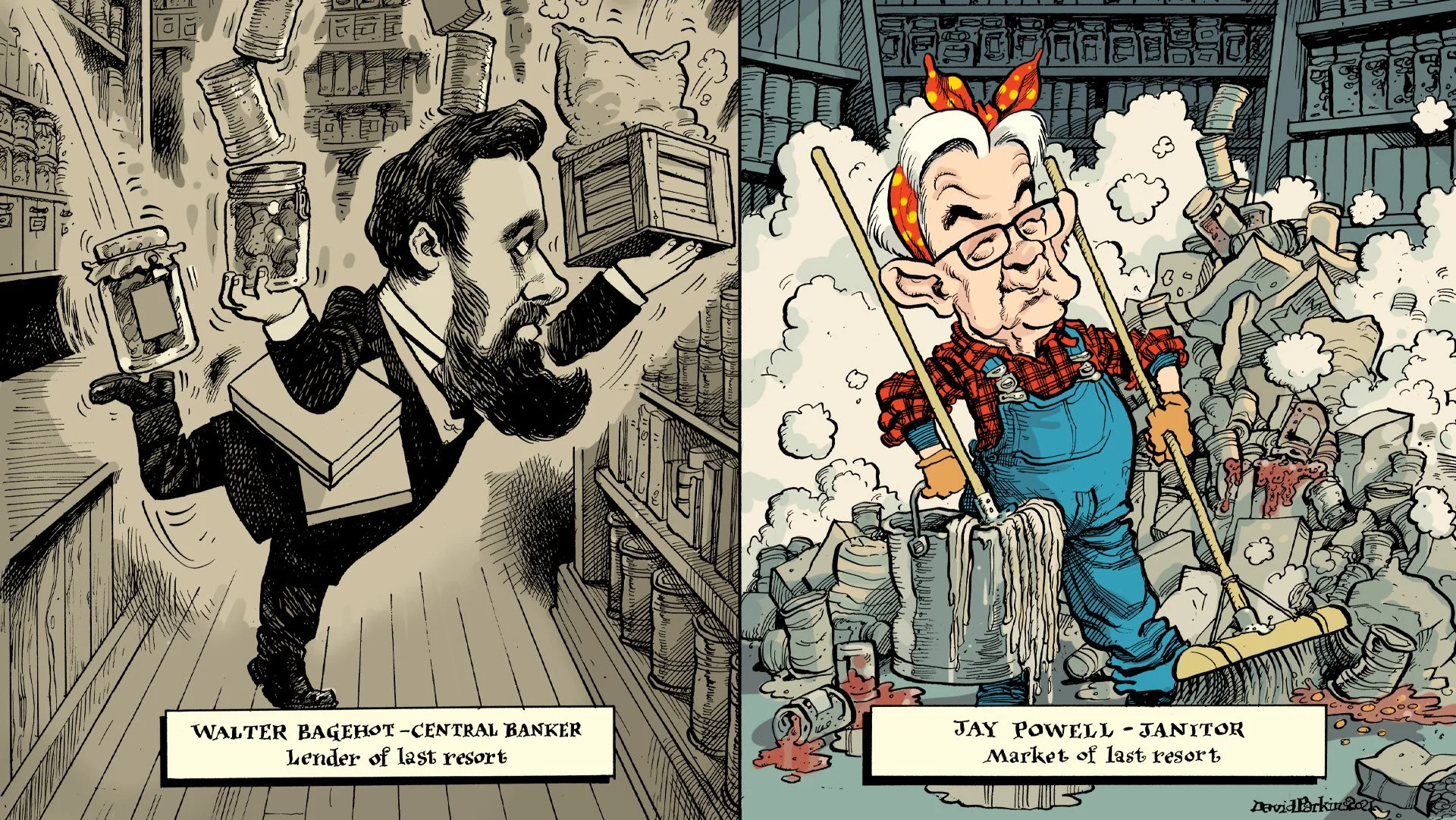

Last week, I wrote about how critical selling was in determining when a financial problem becomes a full monetary crisis. Forced and indiscriminate selling is always the key, which is why the Federal Reserve is now a janitor rather than central bank. They have to catch the falling knives hoping they can spot them coming down before they do too much damage.

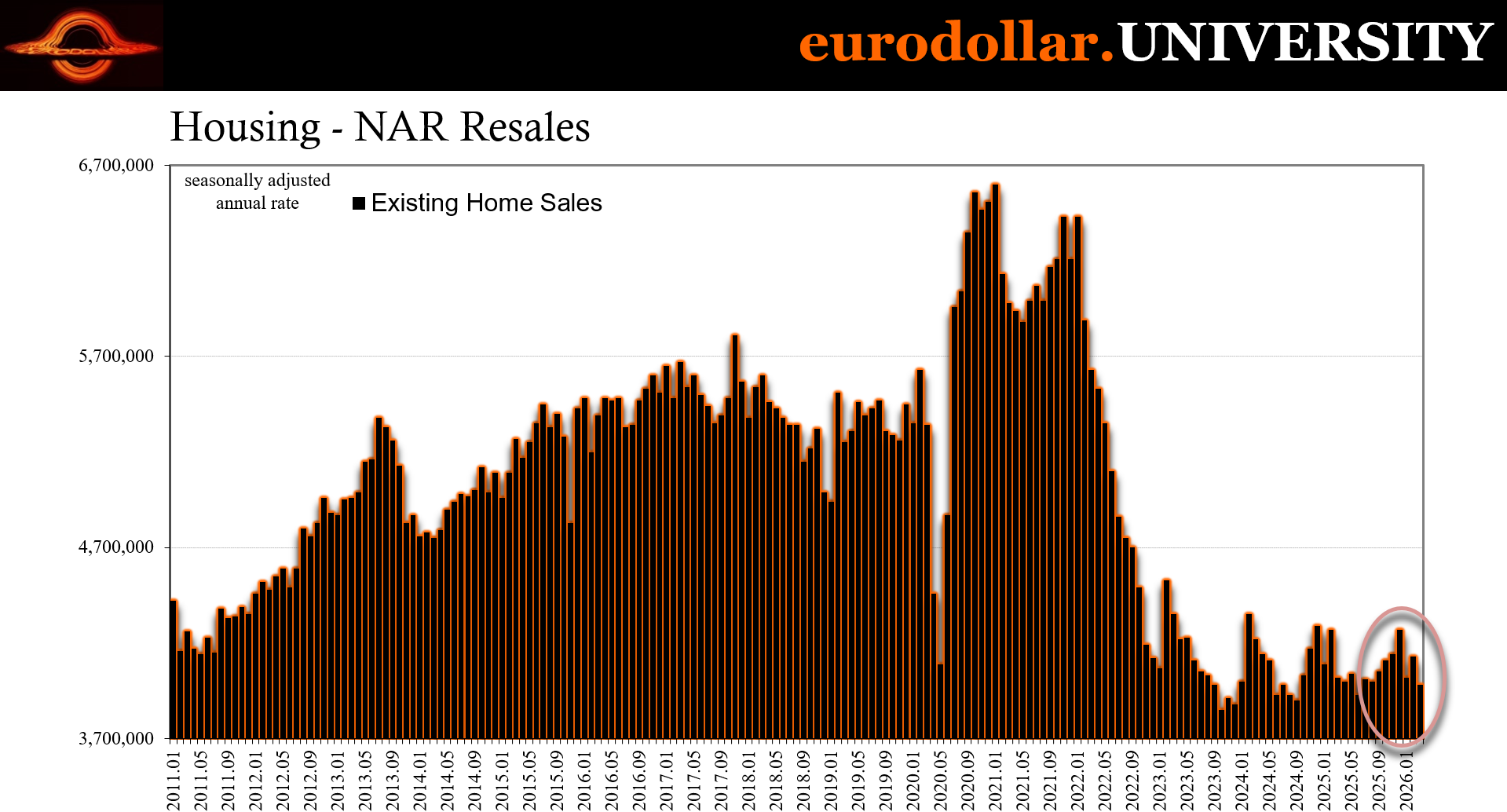

Regular selling is a natural part of everyday experience in financial markets, but what we saw in the housing crisis of the 2000s was something very different and that experience offers a perfect case study. Right now, resale volumes, for example, are as low as they had been during the worst of the Great Housing Bust. According to the NAR, the level has been scraping along at roughly 4 million, give or take, for years already.

There were as few existing homes sold in May 2026 as there had been in April 2011. Think about how wild that is, because in early 2011 real estate was in the absolute doldrums. After years of relentless bust, it was still just getting to the worst of it.

No one would consider the current housing market comparable, yet the data says otherwise at least where it comes to activity; which means the current one is about buyers and the lack of them, rather than sellers.

What drove the property sector into the dirt back then went way beyond a backlash against loose lending standards. The critical difference can be seen – and felt – in prices. Twenty years ago, they were crashing compared to these days just some negative numbers; not that the latter is good, not catastrophic.

Lenders were forced to foreclose on properties which they simply dumped on a market which had no money behind it. SIVs were hardly able to cope with becoming landlords. In fact, they couldn’t. So, forced selling, rampant liquidations, foreclosure auctions ended up not just depressing prices but pushing them down and keeping the spread of systemic collapse going.

The menacing-not-threatening housing bust of the middle 2020s features none of that. There aren’t many foreclosures and even what there are these days financial types know the last thing they want to do is dump a property, at least without reasonable assurance there’s a close price for it. So, the housing bust this time doesn’t necessarily feel like one even though the depression in activity is just as bad.

What’s holding down real estate is therefore the lack of buyers rather than an imbalance of rushed sellers. The problem in seeing this is always Jay Powell, soon to be Kevin Warsh. If you believe, because you’re told to, that the labor market is solid or at least resilient, the lack of homebuyers makes little sense or, as they would have you think, it’s solely because interest rates are too “restrictive.” This appears to validate the mainstream theories on rates.

It doesn’t; look no further than the booming housing market of the 1990s when mortgage rates were at levels today would be considered totally out of reach. An economy that is truly strong and resilient can handle more historically normal financing costs. No one complained about Alan Greenspan’s painful rate targets; quite the contrary, many blamed his “loose” policies for the dot-com bubble.

The point is – emphatically – rates aren’t it, and they didn’t do it. Housing today is entirely about demand, which is jobs and incomes. Full stop. Lower mortgage rates since 2022 didn’t make a dent in the market. The recovery promised by Larry Yun, the NAR’s chief propagandist, was based on the idea Jay Powell had been right when the lack of turnaround proved he hadn’t been (as the Japanese carry traders said).

The latest data on home prices for April shows declines in the main indexes. Not a surprise, not a product of slightly higher mortgages which follow USTs not FOMCs, just flat Beveridge encountering the energy shock and convincing even more possible homebuyers to sit on the sidelines. While the selling wasn’t overwhelming, it has still been there consistently and for over a year, “oddly” timed to right around the time when those Japanese were warning about the dangers of having reached for yield when the job market goes flat.

Both main measures, S&P and FHFA, have themselves gone flat, turned sideways since the start of 2025 (the first negative payroll report is now last January after revisions). The housing market is confirming rates aren’t the story, lack of labor turnover is and continues to be.

Another jolt

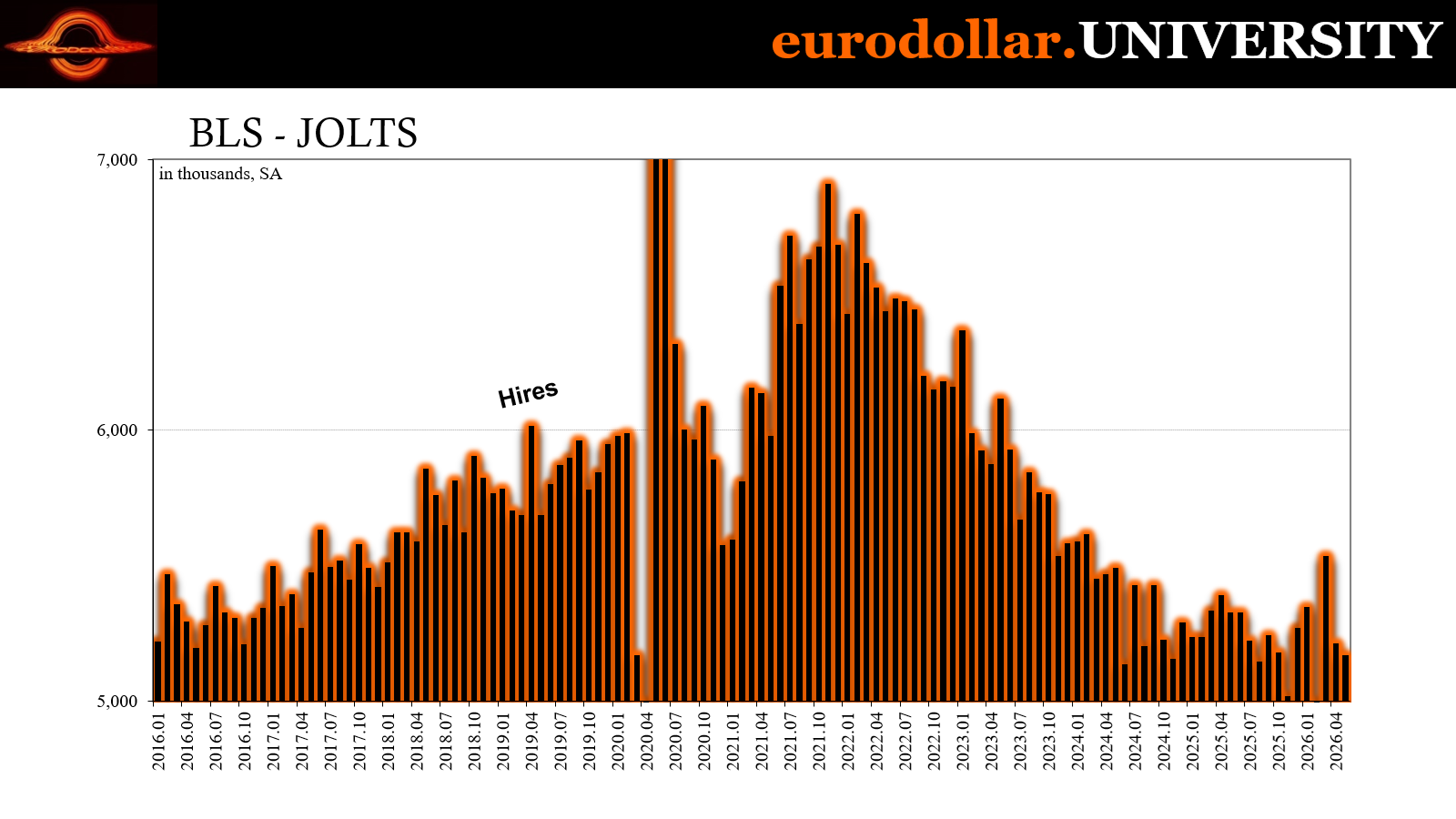

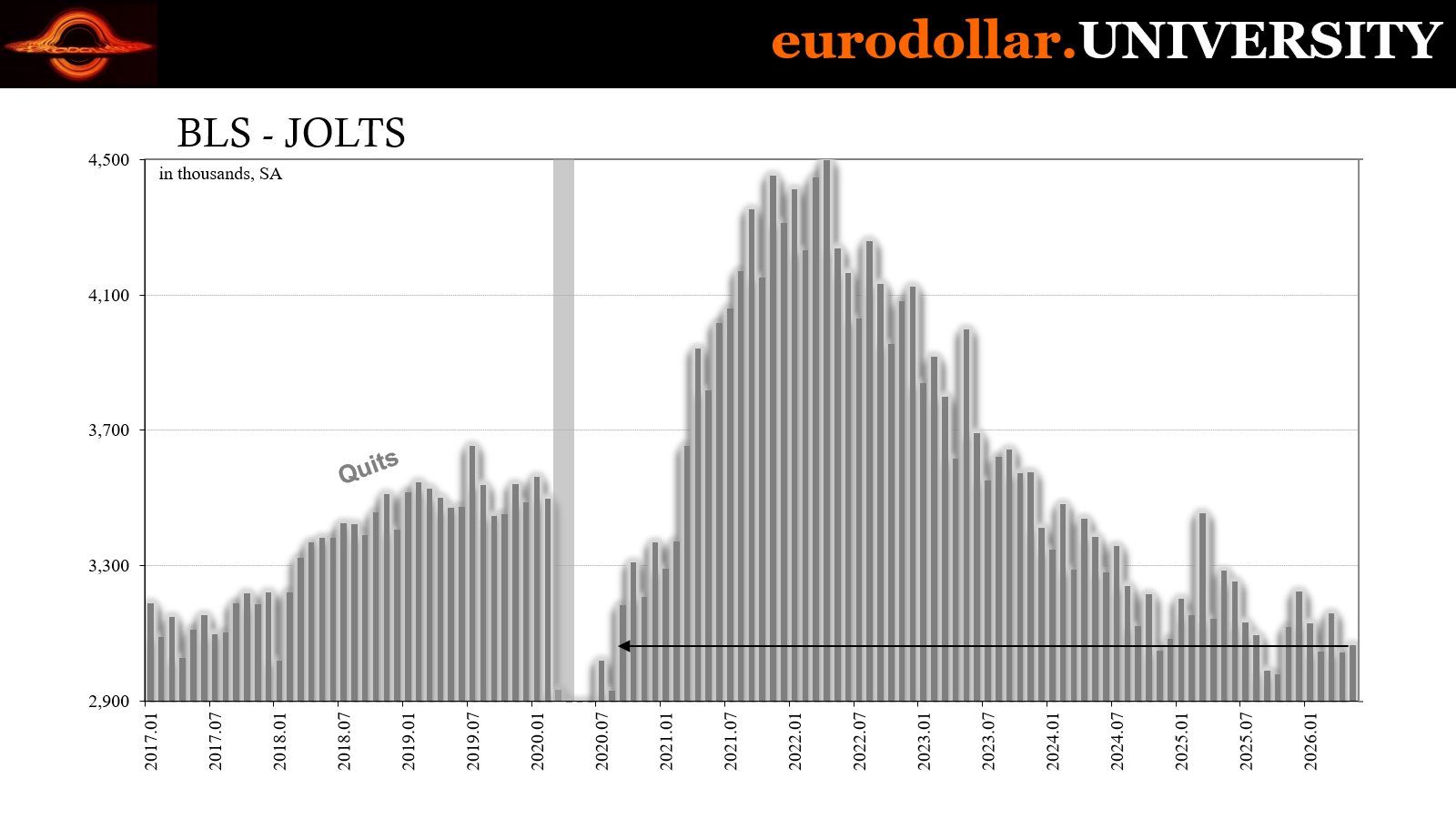

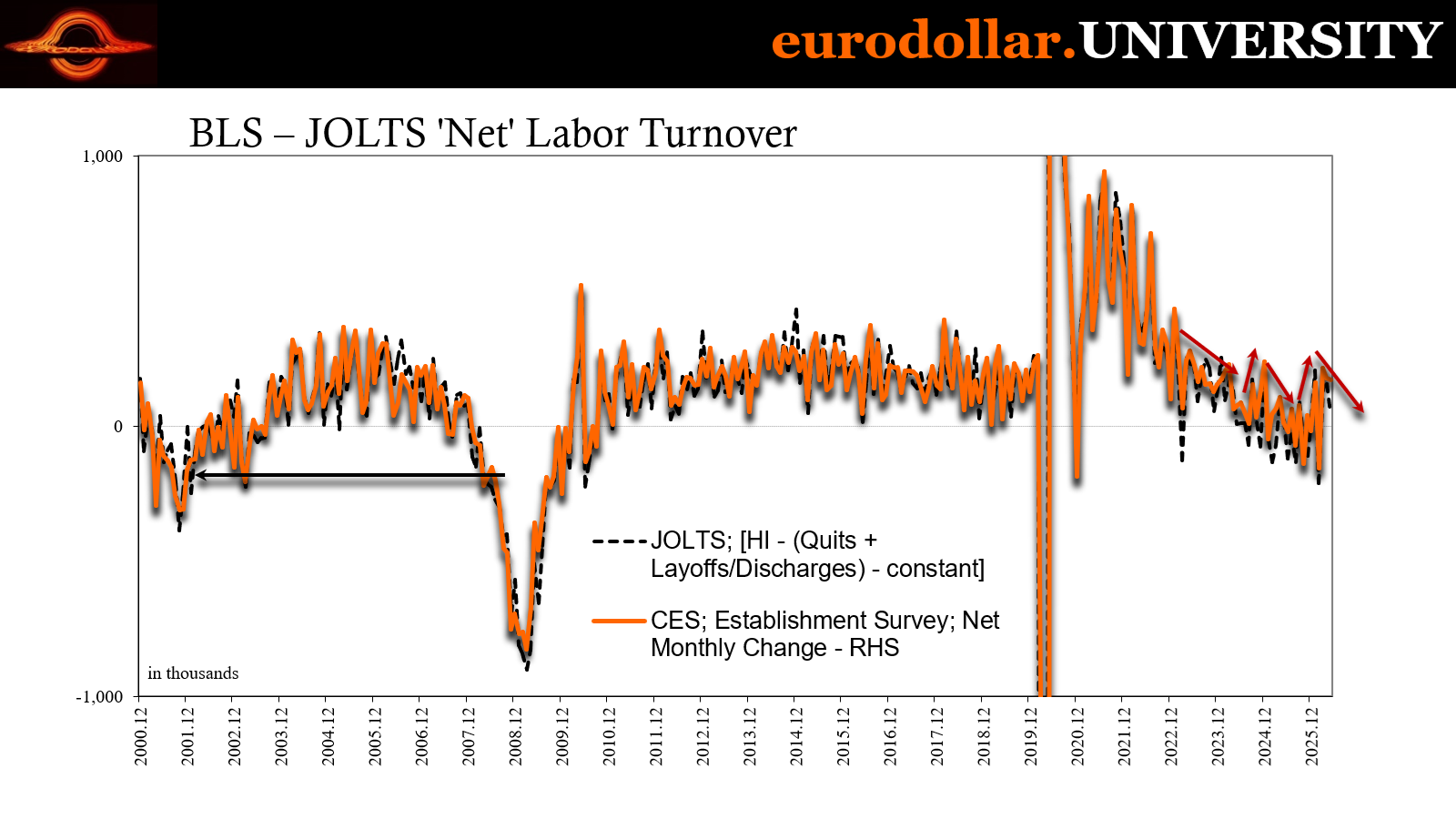

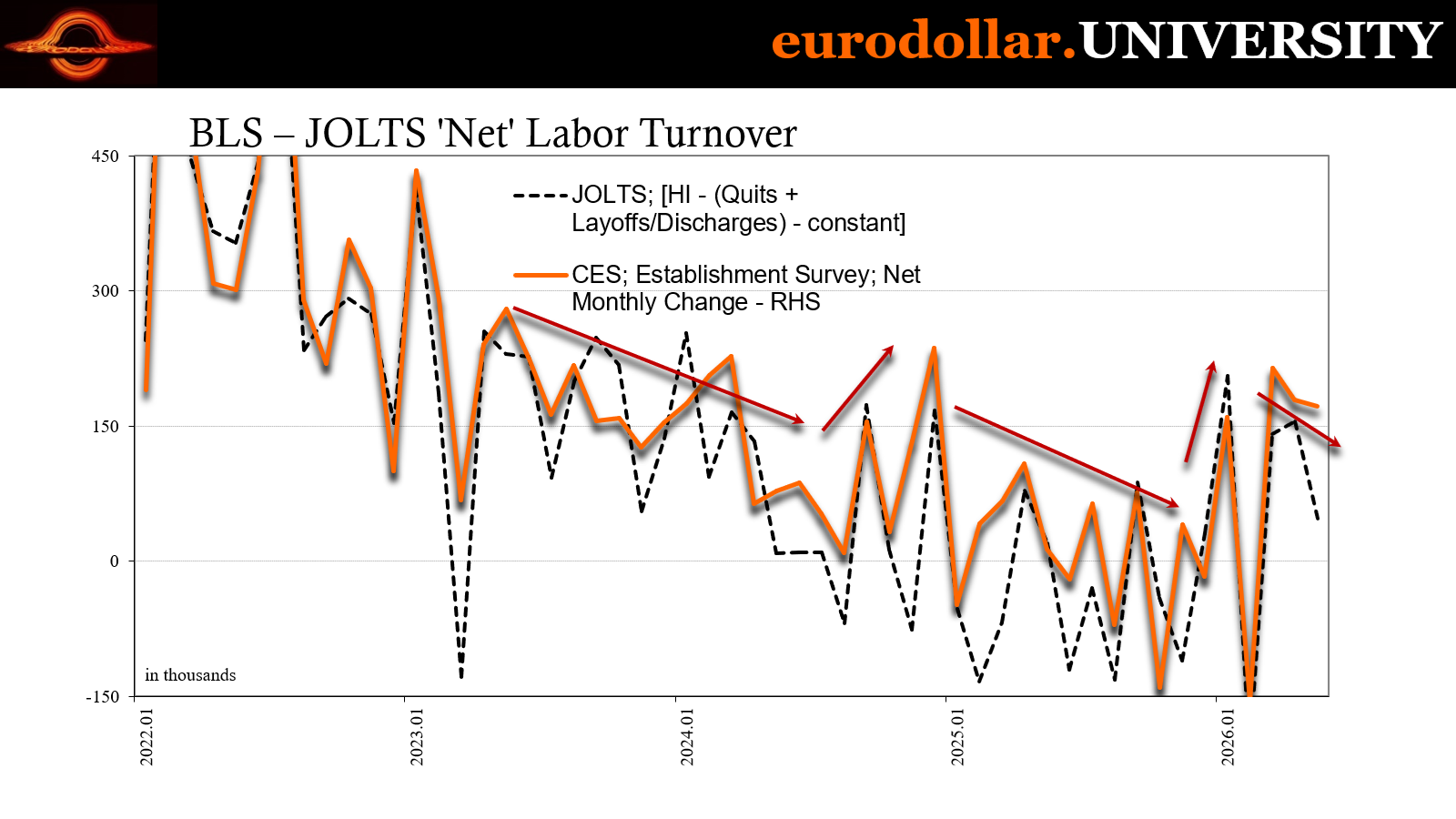

JOLTS was designed to end up where payrolls are but from a different perspective, thinking through a different methodology. The Establishment Survey (CES) looks at employment from the count of, well, payrolls; how many of them establishments report. JOLTS looks at labor through churn, not the number of employees on the books the 12th of each month, instead how many workers were hired versus the number fired or who quit voluntarily.

If you sum all those up, the net turnover should end up close to the monthly change in the payroll level. And the truth is, that’s typically the case. However, the Establishment Survey for years had diverged somewhat, overstating the payroll levels therefore monthly changes (this time is no different). JOLTS turnover was somewhat closer to reality, though it is designed to be similar to CES and is even benchmarked to it.

That difference between the series was put up again for May. Payrolls, as you know, came in well above expectations, making a three-month run of good numbers the series hasn’t produced in a long time. While many were willing to take those numbers as they are, for no good reason, the net turnover in JOLTS suggests employment activity has been getting weaker since March rather than being sustained.

March was…something. Whether it was a sudden burst of work available due to the Iran conflict, the flood of front-loading activity, possibly the US getting ready for the World Cup, most of the data does indicate a bounce of some sort around March. CES kept it up through April and then May.

JOLTS hiring went from deep recession level below 4.9 million in February to over 5.5 million the following month as oil surged – pointing to front-loading not a recovery.

This had happened similarly if to a lesser extent in late 2024’s artificial high preceding trade wars.

Since March, however, while CES shows consistent payroll growth, seemingly indicating a possible sustained pivot in jobs and boosting the margins at the NYSE, turnover points to a comedown from March following numbers that weren’t nearly as positive to begin with. Payrolls went: 214k, 179k, and 172k. Net turnover turns to: 141k, 155k, and then just 47k for May.

That’s more like a temporary artificial high returning to trend, just like what happened early in 2025 and confirmed in the housing market.

Surveys point to the same, not just recently but also since that arrival of flat Beveridge. Consumer sentiment tanked to start last year which today is more obvious in that these data figures now display what Americans were warning about the entire time. As consumers as workers grew more pessimistic throughout last year, Powell and his ilk dismissed it as an overreaction to tariffs; only for his dismissal to blow up in his face with last summer’s fiasco (the same ones the Japanese were warning about the year before).

Today’s report from the Conference Board on consumer sentiment showed a small rise in the overall index, not surprising given the ceasefire with Iran turned to possible peace deal and the retreat in oil and gas (if not quite the same dip for RBOB, which might explain why sentiment wasn’t much changed). But in the details of the report was this not-so-insignificant result:

…perceptions of the current labor market softened measurably as the percentage of consumers saying jobs were ‘hard to get’ rose to 22.5%, the highest level since January 2021 (22.8%). Moreover, consumers anticipate little change in the labor market six months from now.

Does that sound like three “strong” payroll months? Or does it better match labor turnover after a temporary artificial bump and then further aligned with moderately falling home prices for a real estate market which can’t generate buyers no matter what mortgage rates do?

It is, of course, a set of rhetorical questions. Besides, the answers were already given to us in the TIPS market, for one.

One final connection: in that kind of economic climate, the chances of businesses being able to easily pass along higher input costs go right out the window. Consumers don’t have the incomes and far too many fear they’ll end up with even less. Raise the cost of anything and watch buyers disappear. Companies know it, the CPIs are already reporting it, and after some time enough hawks will end up realizing it.

That’s as true in Europe as it has been here. We are talking about the flat part of the Beveridge curve being confirmed in various ways that all lead back to that one place. A lot of economics is ambiguous, thanks in some part to Economics which sows so much confusion. But that is why I urge you to never fall in love with a single series, let alone a single monthly datapoint.

In our current case, there is no shortage of consistent all speaking the same language and saying the same thing. It’s not inflation. After a temporary bump, flat Beveridge is again calling.